PC upgrade cycle to be driven by AI, but calling timing has been difficult

Editor in Chief of Constellation Insights

Constellation Research

Larry Dignan is Editor in Chief of Constellation Insights at Constellation Research, where he leads editorial coverage focused on enterprise technology, digital transformation, and emerging trends shaping the future of business. He oversees research-driven news, analysis, interviews, and event coverage designed to help technology buyers and vendors navigate complex markets with clarity and context. ...

Read more

Personal computers powered by artificial intelligence haven't surged ahead just yet, but demand appears to be strong enough to spur an upgrade cycle. That's a key takeaway from earnings results from Best Buy, Dell and Hewlett-Packard.

During Best Buy's second quarter earnings call, CEO Corie Barry said the company saw solid growth in tablets, computing and services, but those gains were offset by other categories.

"In Q2, we believe the growth in laptop sales continued to be largely driven by customers’ desire to replace and upgrade their products. The performance of Copilot+ in the quarter was in line with our expectations, but at this early point, a small part of the total revenue," said Barry. "We believe we are just at the beginning of the impact of AI on tech innovation and customer demand. For example, the June introduction of the Copilot+ laptops was one of the first launches with an important AI capability. In addition, Apple Intelligence has been announced with capabilities and features across devices. We believe AI inspired capabilities and innovation will continue to spread across categories and devices over the next few years."

"In Q2, we believe the growth in laptop sales continued to be largely driven by customers’ desire to replace and upgrade their products. The performance of Copilot+ in the quarter was in line with our expectations, but at this early point, a small part of the total revenue," said Barry. "We believe we are just at the beginning of the impact of AI on tech innovation and customer demand. For example, the June introduction of the Copilot+ laptops was one of the first launches with an important AI capability. In addition, Apple Intelligence has been announced with capabilities and features across devices. We believe AI inspired capabilities and innovation will continue to spread across categories and devices over the next few years."

PC industry's big dream: AI enabled PCs spur upgrade cycle

Barry added that Copilot+ PCs have higher price points but create a halo effect for PC upgrades overall. She added that PC upgrades will be driven more by evolution than revolution. "We've been really clear in saying we never expected everyone to be lined up at the door waiting for their AI devices. It's more that this continues to proliferate across screens," she said.

In other words, there is definitely an upgrade cycle looming for PCs bought during the COVID-19 pandemic. It remains to be seen how much AI drives those upgrades.

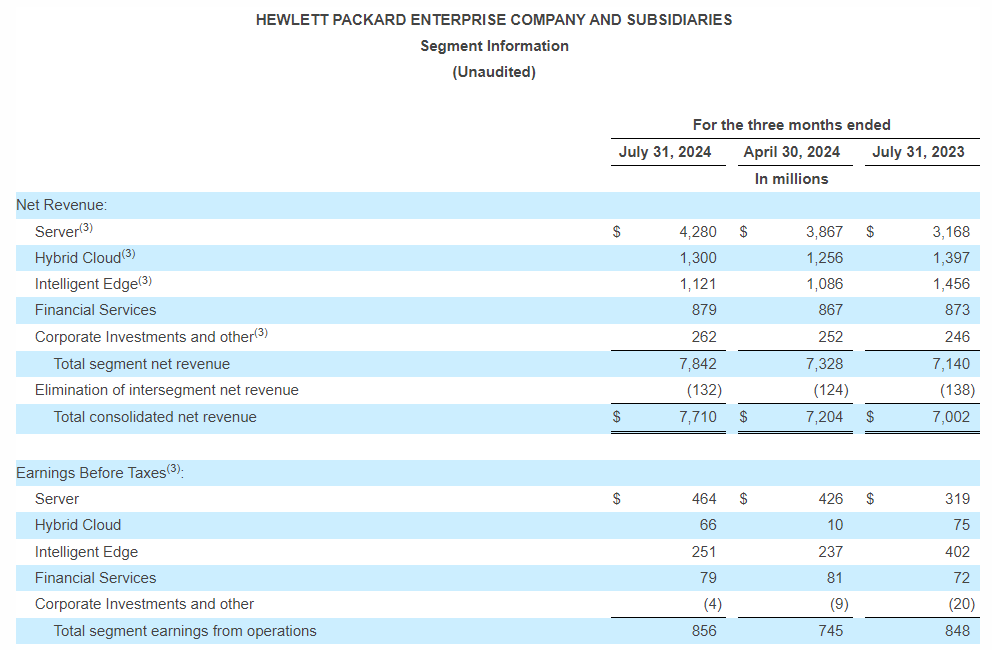

HP's fiscal third quarter results also featured a heavy dose of Copilot+ PC chatter. HP CEO Enrique Lores said the company saw good demand for its PC unit with a "strong recovery" in commercial PCs.

Lores said:

"In the AI PC category, we are charging ahead. Our next-gen AI PCs are empowering everyone from knowledge workers to data scientists to unlock the power of AI. In May, we launched our first generation using the latest Qualcomm processor. As the world's thinnest next-gen AI PCs with the longest battery life, they are made for mobility. And in July, we introduced a new premium model powered by the latest AMD processor. It is the most powerful AI PC in the industry with up to 55 TOPS of NPU performance. It delivers personalized experiences like real-time translation, personal communication coaching, and quick professional video creation and to help protect against AI-assisted cyber-attacks."

Lores also noted that HP's AI Studio workstation is designed for data scientists and AI developers. Going forward, HP said it expects commercial PC strength with consumer market weakness. "We had said that we expected sales to be around 10% during the second half and we think we're going to be slightly above that number. So, they are performing well. Where we really are also focused on what we call next-generation AI PCs that we have just started to launch," said Lores. "We expect next-generation AI PCs to represent around 50% of shipments in 2027, three years after launch, and they drive an average selling price increase between 5% and 10%."

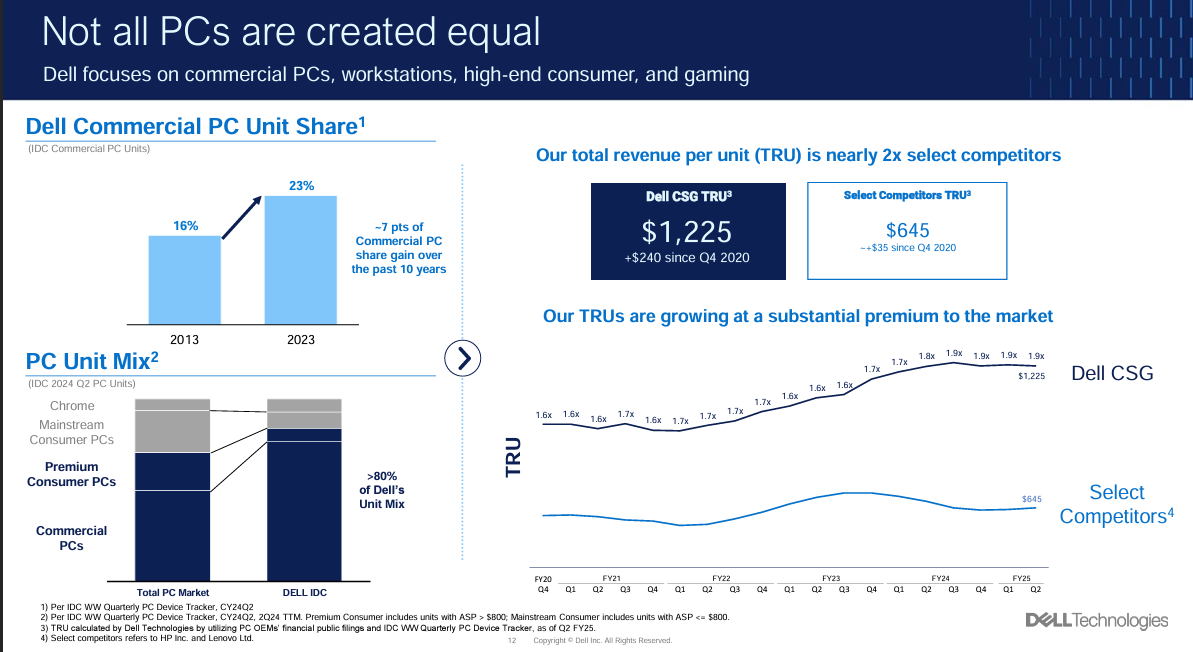

As for Dell Technologies, the company said its PC unit saw "modest commercial PC demand growth in the quarter with healthy operating profitability."

Dell Technologies said that it expects PC revenue growth in the second half in the year, led by the fourth quarter. Over time, PC upgrades will be driven by the long-term impacts of AI.

Jeff Clarke, Chief Operating Officer of Dell Technologies, said:

"We remain optimistic about the refresh. I think it's reflected in our guidance that we think the refresh is shifting more towards the end of the year than we thought, maybe at the middle of the year. The refresh is heading towards end of '24 into '25. What's important about that is, as the refresh takes longer it snaps back faster because the Windows 10 end of life date. We have an aging install base of machine bought during the Covid era all mounting to be refreshed with exciting new products built around AI. More AI applications are coming. Calling the timing has been difficult.

Applications to help productivity with end users is around the corner. And if you think about the extension of AI up to the edge, and what inferencing will be done on the edge on PCs that opportunity is immense as well. When you think about running these small language models with larger memory footprints on the edge your PC will do amazing things."

My take: For the next 12 months, AI PCs will get folks interested in upgrading. I can't necessarily figure out the value proposition for Copilot+ PCs yet, but if you have to upgrade (and many of us do) there is something to be said for future proofing.

Data to Decisions

Future of Work

Innovation & Product-led Growth

New C-Suite

Tech Optimization

Next-Generation Customer Experience

Digital Safety, Privacy & Cybersecurity

dell

HP

AI

GenerativeAI

ML

Machine Learning

LLMs

Agentic AI

Analytics

Automation

Disruptive Technology

Chief Information Officer

Chief Experience Officer

Chief Executive Officer

Chief Technology Officer

Chief AI Officer

Chief Data Officer

Chief Analytics Officer

Chief Information Security Officer

Chief Product Officer