Salesforce Dreamforce 2024: Takeaways on agentic AI, platform, end of copilot era

Salesforce Dreamforce 2024: Takeaways on agentic AI, platform, end of copilot era

Larry Dignan is Editor in Chief of Constellation Insights at Constellation Research, where he leads editorial coverage focused on enterprise technology, digital transformation, and emerging trends shaping the future of business. He oversees research-driven news, analysis, interviews, and event coverage designed to help technology buyers and vendors navigate complex markets with clarity and context. ...

Read moreSalesforce CEO Marc Benioff laid out the company’s AI vision, which revolves around autonomous agents working with humans and the end of the “hit or miss” copilot era. The mission for Benioff: Put the copilot era to bed and focus on agentic AI powered by one platform the Salesforce platforms. Benioff said he wanted his customers to use Agentforce to deploy AI agents at Dreamforce and put an end to do-it-yourself AI.

During his keynote at Dreamforce, Benioff and his executives laid out the case for depending on Salesforce as your AI platform. As telegraphed by Salesforce leading up to the keynote, the talk was heavy on Agentforce.

Benioff said:

“The copilot world has been kind of a hit and miss world. It's been a copilot world where you say, ‘I have these copilots, but they're not exactly performing as we want them to. We don't see how that copilot world is going to get us to the real vision of artificial intelligence, the augmentation of productivity, or better business results. In some ways, copilots are the new Microsoft Clippy. This is the third wave AI. It's agents.”

"Benioff made a pretty compelling case for Data Cloud and the Salesforce platform as the basis of building agents. The approach taps data, metadata and knowledge of app business logic that's all already in Salesforce. Data Cloud adds data federated from third-party data clouds and ingested from external apps. The pitch that everything is in one platform and not a DIY project has attendees here at Dreamforce nodding their heads," said Constellation Research analyst Doug Henschen.

Here are the key takeaways from Dreamforce 2024.

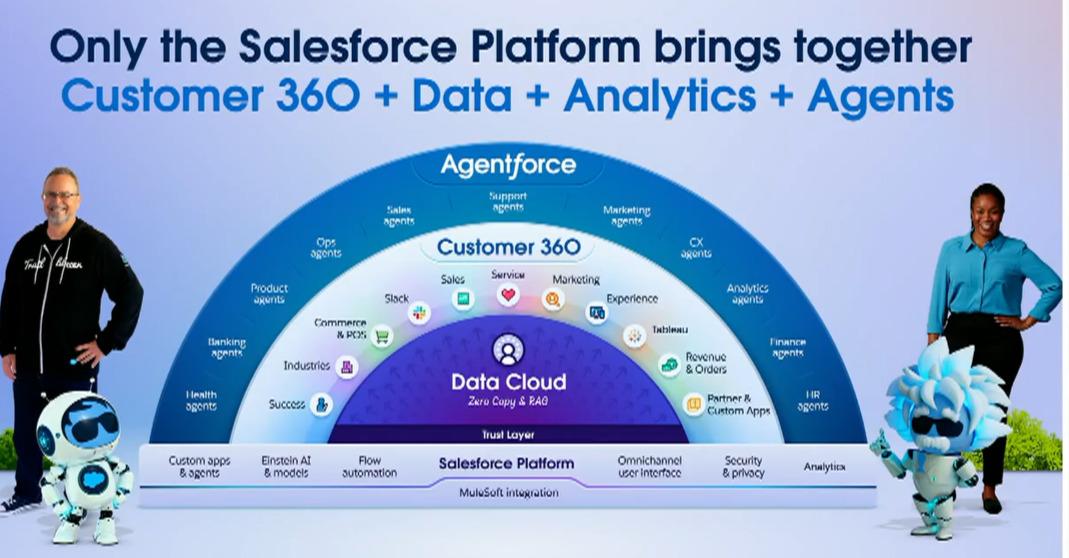

Salesforce is now a platform and less a series of clouds to cross sell. For the last few years, Salesforce has done the heavy lifting to create a series of clouds that run native together. This grunt work is enabling Salesforce to scale Agentforce across Marketing, Commerce, Sales, Revenue and Service Clouds as well as Tableau.

Agentforce wouldn't be possible as envisioned without a unified platform. Salesforce's move to one platform is what enabled it to build out Agentforce using Airkit.ai technology acquired a year ago. With a unified platform, Salesforce is betting it can fend off rivals like ServiceNow, which has the potential to relegate enterprise software to systems of record.

“We are all going to be using agents, but we're going to do it all within our Salesforce platform,” said Benioff. “This platform is the key strategic motion of Salesforce, and now this platform has the best AI in the world.”

Showing Agentforce will sell AI agents to the enterprise, upend the copilot craze and convince companies that new business models like pay per conversation are warranted. Let's face it: Dreamforce 2024 is really one big demo. Agentforce was outlined ahead of Dreamforce with a steady cadence of news. It remains to be seen how this Dreamforce (Agentforce) demo fiesta affects Salesforce's growth.

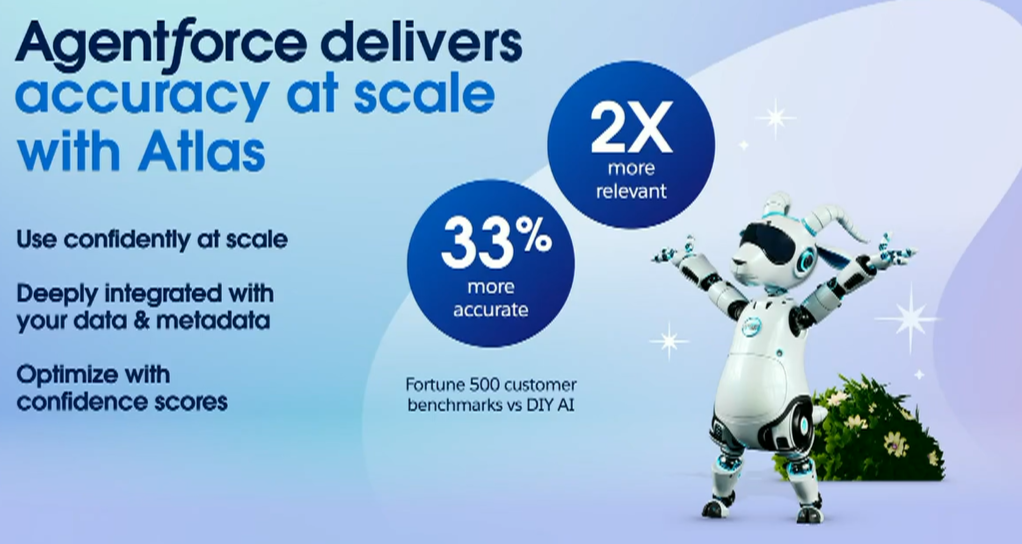

Accuracy will be the big selling point for Agentforce. Benioff said:

“These agents are going to be some of the lowest hallucination agents who've ever experienced. Why is that? Why would our agents be so low hallucinogenic and so accurate? Well, it has to do with the platform. It's because we have the data and the metadata and the workflow and the business process and the security model and the sharing model.”

Benioff’s goal is to light up Agentforce as fast as possible for customers and highlight it as a way enterprises can scale labor during peak times.

Everything you need to know about Dreamforce 2024:

- Salesforce adds AI agents to Marketing, Commerce Clouds, Slack at Dreamforce 2024

- With Salesforce push, AI Agents, agentic AI overload looms

- Salesforce debuts Agentforce: Will enterprises pay $2 per AI agent conversation?

- Salesforce Q2 revenue growth 8%, touts Agentforce

- Salesforce's Benioff ponders consumption-based model enabled by Agentforce

- Salesforce Furthers Autonomous AI Agent Development with xGen Concept & Tenyx Buy (see release on new genAI models)

- Salesforce's New AI Agents Mark Foray into Autonomous AI

- Salesforce's acquisition of Own highlights small ball approach to M&A

DIY genAI isn’t worth it. Benioff’s big pitch to enterprises is that the power of platform can drive more value than do-it-yourself efforts. He said:

“DIY means I'm just putting it all together on my own. But I don't think you can DIY this. You want a single, professionally managed, secure, reliable, available platform. You want the ability to deploy this Agentforce capability across all of these people that are so important for your company. We all have struggled in the last two years with this vision of copilots and LLMs. Why are we doing that? We can move from chatbots to copilots to this new Agentforce world, and it's going to know your business, plan, reason and take action on your behalf.

It's about the Salesforce platform, and it's about our core mantra at Salesforce, which is, you don't want to DIY it. This is why we started this company."

To drive the point home, Salesforce is upgrading all customers from Einstein Copilot to Agentforce. Constellation Research analyst Martin Schneider said:

“The upgrade of Copilot to Agentforce might surprise some more casual users who might still be trying to get a foothold in terms of deploying AI into production. In short, Salesforce might be moving too fast here. But the company is doing a solid job of telling an “easy button to Agentforce” story. The emphasis on both security and “trust” as well as a low/no code message in most of the messaging should help even single-cloud users take the plunge.”

"The "Don't DIY your AI... it's too much" message is a pretty effective take down of the prevailing AI proposition. Nonetheless, it's healthy to be skeptical. I think customers will want to experiment for themselves and know more about costs before proceeding at scale," said Henschen.

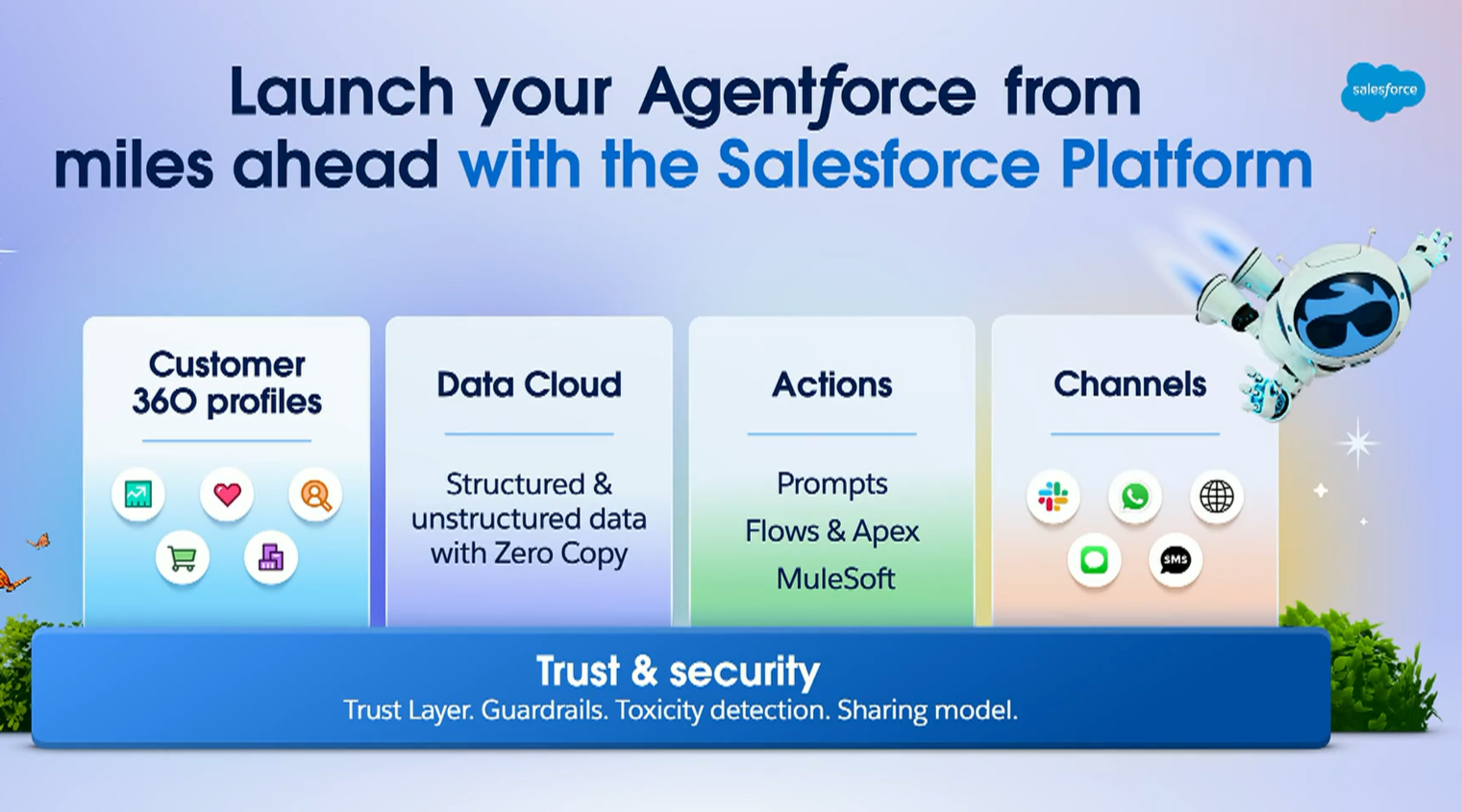

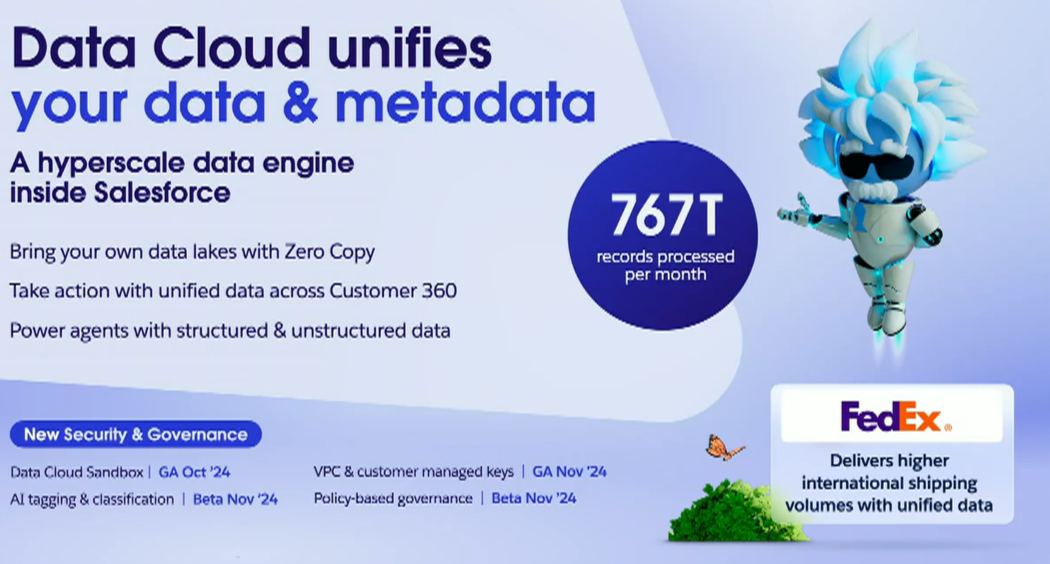

Data Cloud is the glue of the Salesforce Platform. Data Cloud is seeing 130% growth year over year in paid customers. The company touted customers including FedEx and Wyndham Hotel & Resorts. With Data Cloud, Salesforce is looking to couple Data Cloud, Customer 360 and Agentforce across its platform with the ability to automate actions and workflows.

With its built-in vector database, Salesforce is arguing that Data Cloud is the platform to ingest unstructured and structured data, data lakes and warehouses. Data Cloud is also the conduit to leverage metadata across multiple enterprise functions. At Dreamforce, Salesforce said it is adding support for unstructured audio and video to Data Cloud as well as connectors to multiple partners and more governance features.

The message is clear: Without a data strategy, you don't have an AI strategy. Data Cloud is the core of your data strategy because it grounds Agentforce. Data Cloud One is seen as the glue that can connect silos of Salesforce instances across large enterprises.

Constellation Research's Henschen lays out the Data Cloud evolution.

"Salesforce is extending, maturing and advancing the performance of Data Cloud on multiple fronts. It starts with zero-copy, federated connections now being available for the top five analytical data platforms -- Snowflake, Amazon RedShift, Google BigQuery, Databricks and Microsoft Synapse/Fabric. Prebuilt connectors for data ingestion now extend to more than 200 leading apps. Semi-structured and unstructured data are now supported with the addition of vector embedding/search and retrieval augmented generation (RAG). Finally, both structured and unstructured data can now power agents developed in Agentforce with low-latency, millisecond-speed performance through streaming data pipelines. All leading data platform providers are also pushing on all these fronts, but for Salesforce customers that want to build AI and personalization around customer data, Data Cloud is an option they have to consider.”

Agentforce and AI agents are an ecosystem play. Salesforce realizes that it can't be an AI agent silo so it's creating an ecosystem. Part of that ecosystem revolves around systems integrators (naturally), but the vision also includes a bevy of partners that will build AI agents for the Salesforce platform. Salesforce is also looking to make its agents portable to other applications including Google Workspace and Google Cloud, Amazon Web Services, Box, DocuSign, Workday, IBM, Zoom and other established vendors in the enterprise stack.

The play for Salesforce will be to ensure its AppExchange is loaded with plug and play AI agents.

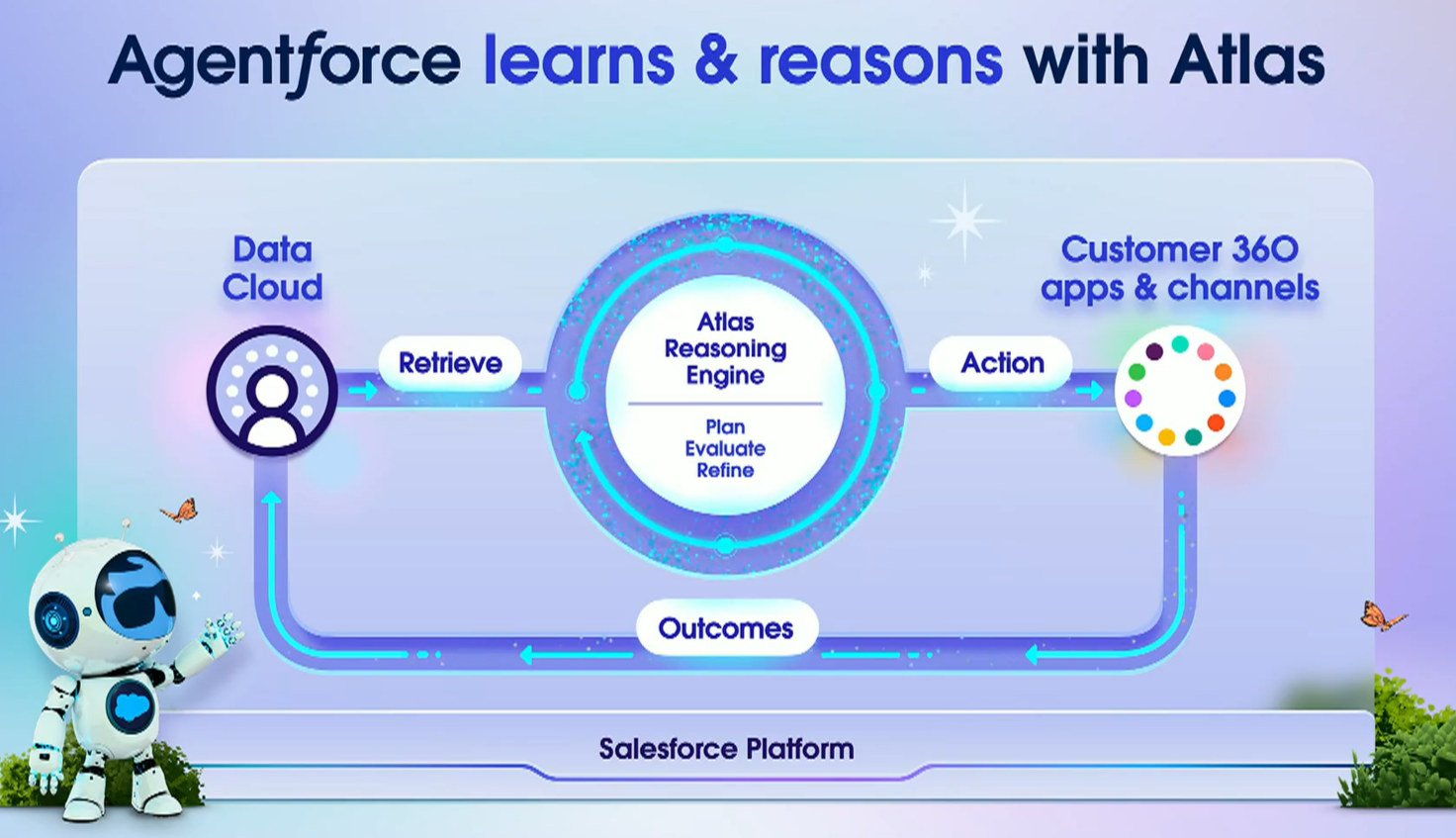

Atlas details still sparse. Agentforce is driven by the Atlas reasoning engine, but executives didn't divulge much.

During the keynote, Clara Shih, CEO of Salesforce AI, outlined the following about Atlas:

- Atlas is the brain of Agentforce. It takes goals, roles, data and creates a plan and then refines it as it executes. Using RAG and Data Cloud it leverages Customer 360 data.

- “Atlas knows to seamlessly escalate to one of your team members using Sales, Service, Marketing or Commerce Clouds. My favorite thing though about Atlas is that the more you use it, the smarter it gets.”

- “While everyone else in the industry is talking about reinforcement learning from human feedback, we have pioneered reinforcement learning from customer outcomes in Customer 360, whether it’s marketing conversion rates or sales, deal wins or service resolutions. All of that is used to continuously tune and improve your Agentforce. And because your data isn't in our product, all of your outcome data is proprietary to your company.”

The other argument for Agentforce with Atlas is it trumps DIY genAI efforts.

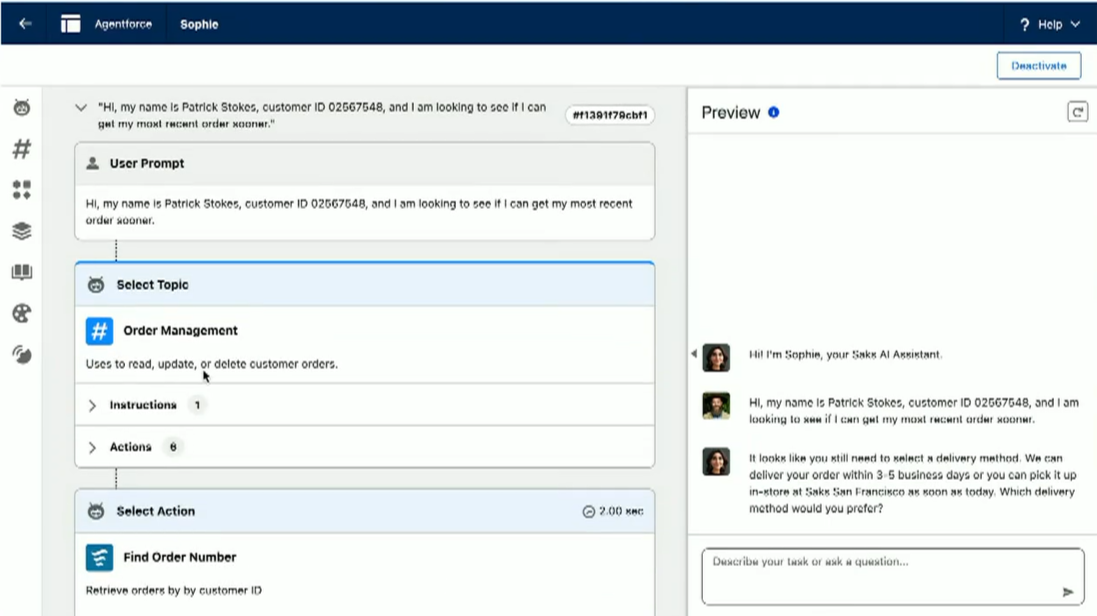

A demonstration did highlight how Atlas reasons within Agent Builder.

Salesforce will have to tell the Agentforce story through its customers. Benioff said that the aim of Dreamforce is to get enterprises up and running quickly with Agentforce. If successful, Salesforce can show business value, the power of the platform and land customer references. Salesforce has been highlighting customer references including Wiley, Disney and Saks.

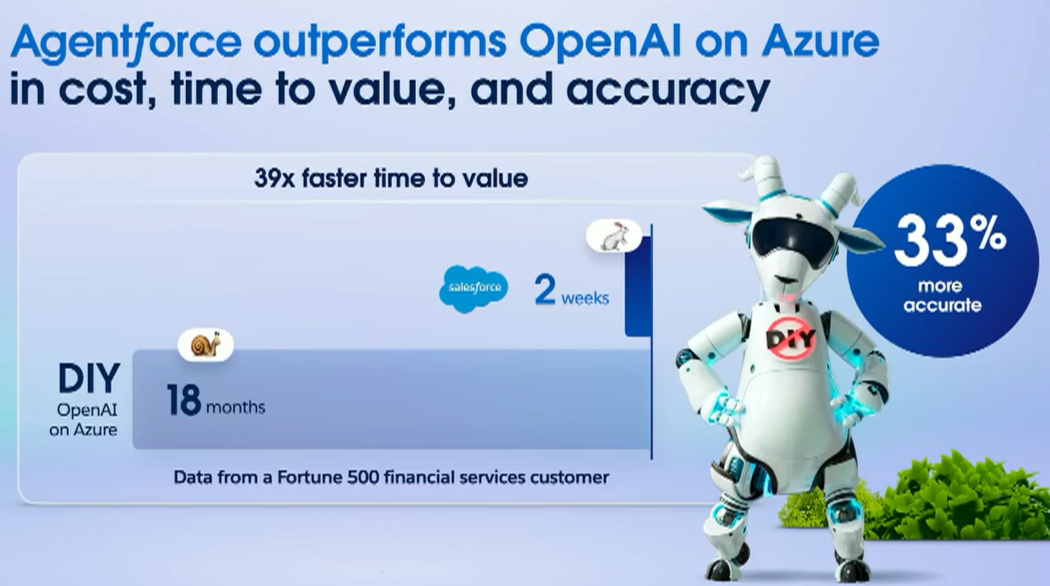

Benioff also encouraged enterprises and cusotmers to benchmark Agentforce vs. alternatives such as OpenAI on Microsoft Azure.

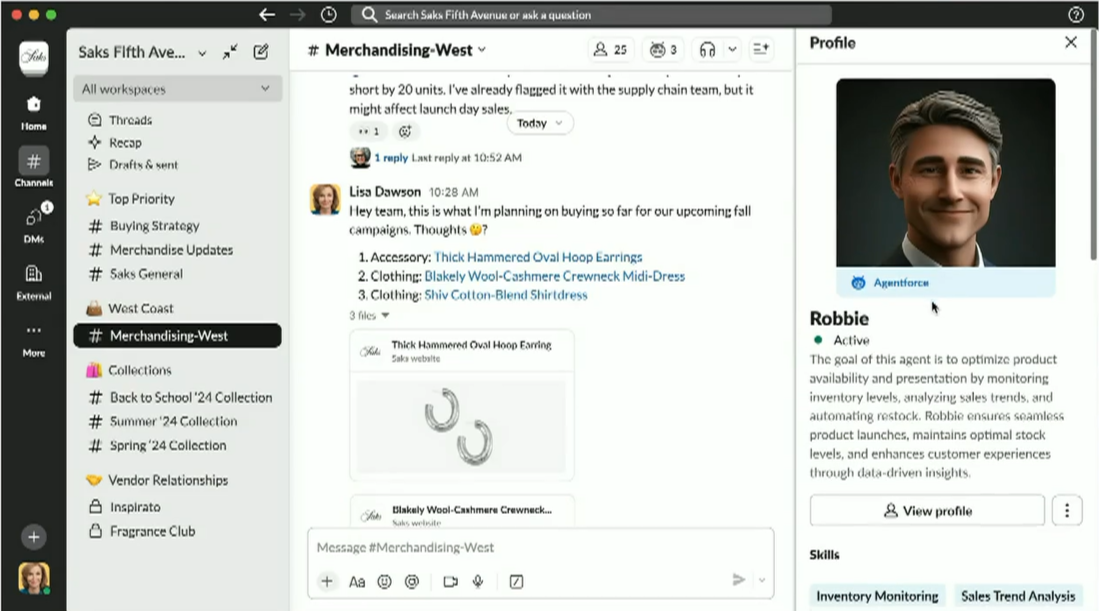

Slack is being positioned as a work operating system (again), but the agentic AI era may actually make the vision real. Slack from its inception was viewed as a work operating system. Slack has been more of a collaboration tool. For work OSes, think Smartsheet, Asana and Monday.

But AI agents may make Slack more valuable--perhaps not valuable enough to justify the $27.7 billion Salesforce paid for the company. That Slack acquisition is why Salesforce must think smaller about M&A today. Agentic AI has the potential to transform Slack and its mission.

Constellation Research analyst Liz Miller noted a few swipes at the contact center during the Salesforce keynote. "The contact center zingers were the backbone for all of this Agentforce conversation," said Miller. "The next question is how will Slack allow for real time and asynchronous communication and collaboration across human and AI agents. Slack takes on a very different role. Where and how are you including agents into a swarm? Where and how are agents adding to and improving conversations and actions that come after. This puts much more pressure on the Slack team to quickly innovate.”

Data to Decisions Future of Work Innovation & Product-led Growth Marketing Transformation Matrix Commerce Next-Generation Customer Experience salesforce Chief Information Officer