Oracle Cloud makes progress - but key work remains in the cellar

Oracle CEO Mark Hurd made an appearance and talked about Oracle’s progress in his unique, numbers-driven style, stressing the value of cloud. It was good to see his view and to get some insights into Oracle’s cloud strategy straight from the top. His example of e.g. IBM shrinking revenue by $10B and how much of that revenue is going to be Oracle’s resonated well.

Also interesting that Hurd sees HCM and Customer Service as the most important applications of the 21st century – as taking care of employees and customers is essential for enterprises to tapp into faster and sustainable growth. At the end of the day Hurd asks CxOs to accept the reality of the cloud that is simple(r), more innovative, enables disruption, creates speed and has the better economic operation advantage.

MyPOV – Hurd has a unique personality that is clearly data and numbers driven, and his pitch for cloud will resonate well with equally number driven CxOs. It is also well aligned with Oracle’s organizational DNA of TCO reduction – which manifested itself through the product demonstrations, too. How well that approach works in less rational buying decision environments will be interesting to observe in the next quarters.

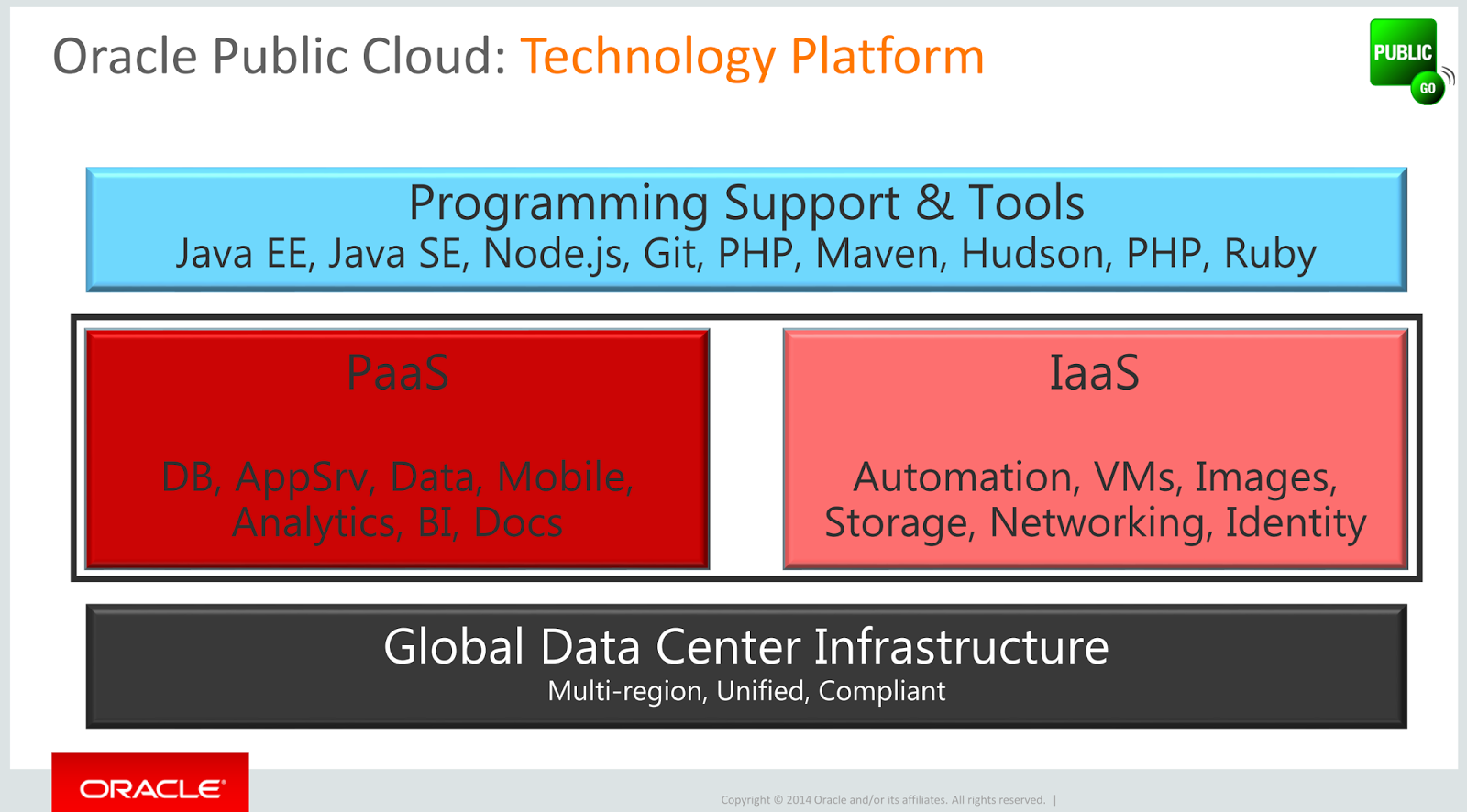

Earlier Oracle President Thomas Kurian kicked off the day – walking through the complete Oracle cloud portfolio in very short order. At a 30k feet level Oracle kept the format with its 4 ‘as a Service’ offerings – with IaaS, PaaS, SaaS and DaaS (Data as a Service).

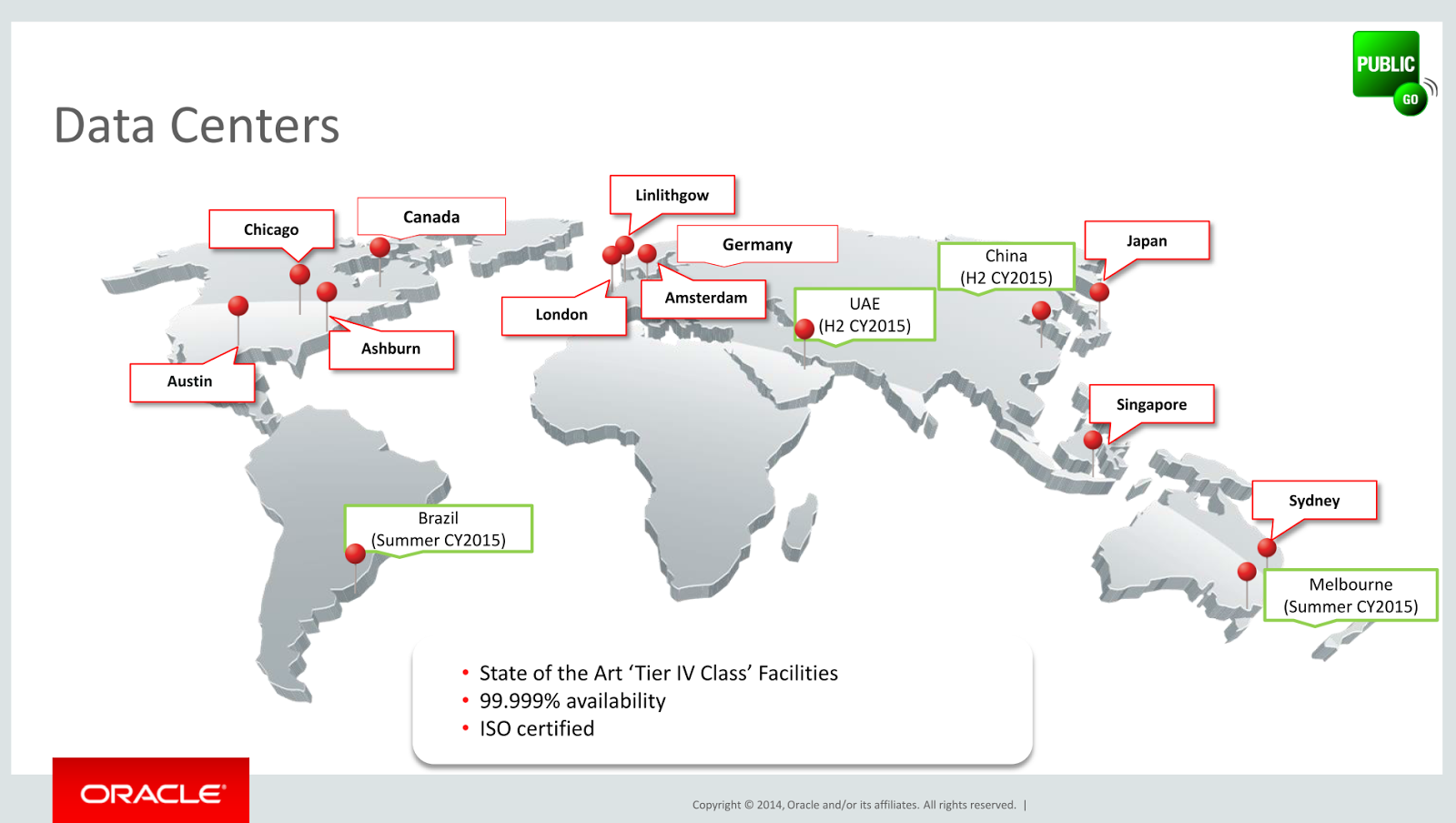

Oracle is the only cloud vendor prominently featuring DaaS, which plays well to Oracle’s database heritage but is equally forward looking, as enterprises become software companies and data being the key equity for next generation business processes. We will break this down next, but let’s note that Oracle has made progress in its datacenter infrastructure, too – with 19 (soon to be 21) Tier 4 data centers operating the Oracle Cloud, the newest additions being Toronto, Frankfurt, Calgary and Munich. This makes Oracle one of the few cloud providers with multiple data center locations in Canada and to our knowledge the only provider with two data centers in Germany. Data center locations matters for cloud, not only from a data sovereignty but also from a performance perspective.

For comparison and consistency reasons I will keep this blog in the same format as last year’s Progress Report (you can find it here).

The State of IaaS

The Oracle IaaS offering comprises Storage (Elastic Object & Elastic Block Storage), Compute – and new – Software Defined Networking (SDN). A year ago queues, notifications and Identity ran under IaaS, but have now been promoted to PaaS. Oracle now supports a single global namespace across Storage – a huge simplification and value over some competitors, geographic replication and a shared file cloud service (in beta). Oracle will (and has to) expand these services in the next 18 months substantially. On the Compute side, Oracle now offers a general purpose, high performance, dedicated and engineered compute service, giving customers a wide range of compute offers to choose from. Major functionality for Compute is being delivered this year – but the roadmap was only shared under NDA. New compared to last year was the Software Defined Network product offering, where Oracle offers Software VPN Layer 2 and 3, Hardware VPN IPSec Tunneling, a Direct Connect offering to its Public Cloud and Network Bonding. Effectively Oracle offers to connect through the Equinix Cloud Exchange, AT&T Netbond and hardware VPN based InterConnect.

MyPOV – Good progress by Oracle on the IaaS side. 2015 is the key year for Oracle to deliver some critical IaaS features that will make the offering competitive to other offerings in the marketplace. Regardless there is good customer traction for Oracle IaaS today as customer panel and reference slides showed.

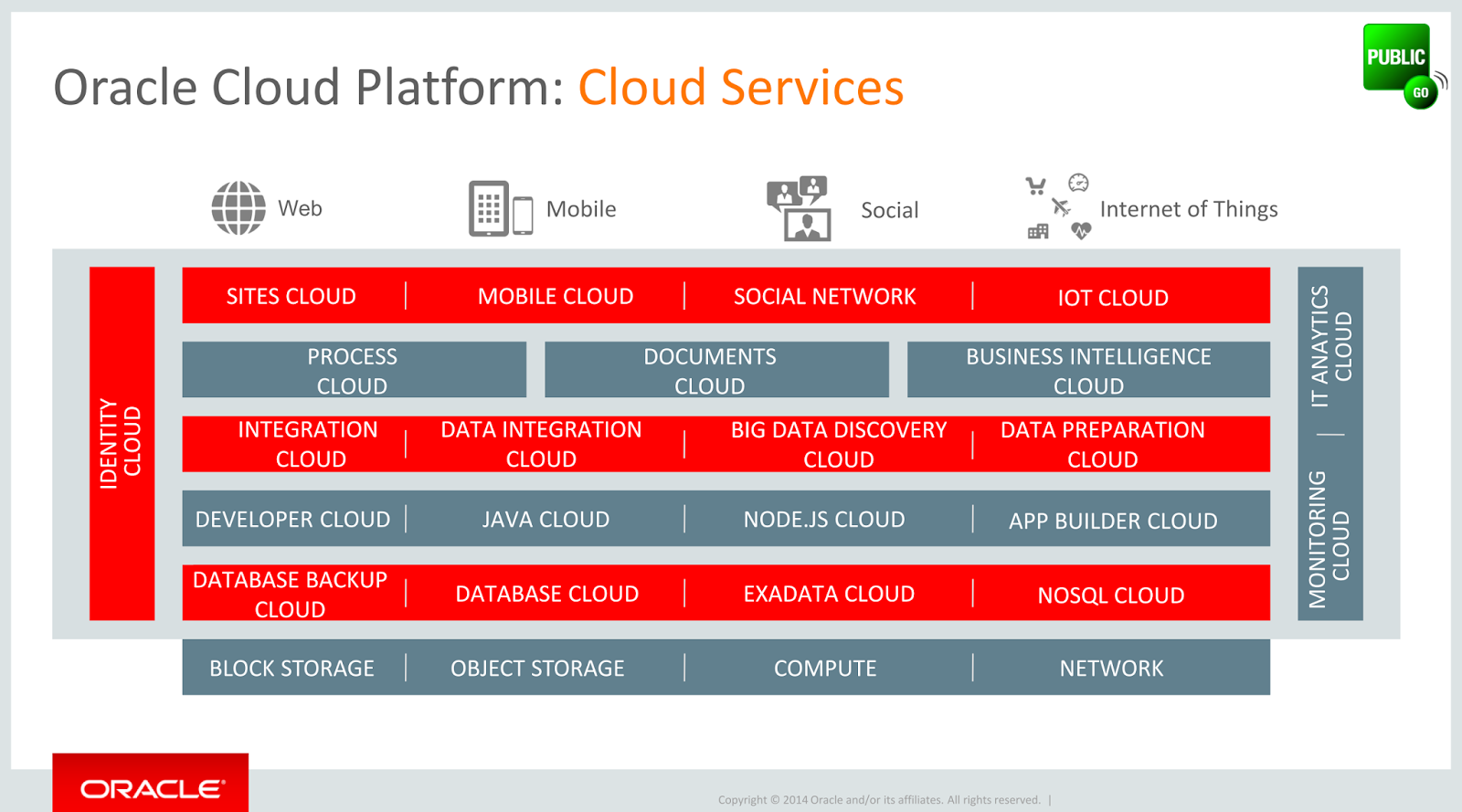

The State of PaaS

Oracle PaaS is taking a persona centric view on using the Oracle middleware and database stack: Oracle has always courted developers, and the middleware DNA goes back to integration, so these personas stay, what’s new (debut was at OpenWorld) is the departmental user and analytics user. For developers the rapid deployment and the polyglot language capabilities of Oracle PaaS stick out as differentiators. On the integration (aka iPaaS) side Oracle has done progress on click integration / 0 coding options, which are actually an enabler for the departmental user area. Oracle here delivers on the PaaS side a comprehensive integration platform for different styles of integration (applications, data, process, events and identity) designed with each persona in mind (developer, architect and departmental User). With PaaS Oracle is delivering on the extension and integration promise from OpenWorld for its SaaS products, but also complements it with LOB capabilities like document, storage, mobile, collaboration and social options. For the analytics user Oracle PaaS offers all discovery and analysis options for data residing in (Oracle) RDBMS, OLAP and BigData. The visual analysis of complex data for the departmental user is one of the differentiators.

MyPOV – Good move by Orcle to more roles beyond the the common 2014 PaaS roles of developers, IT users and LOB users.. Defining more specific and interesting forward looking roles as for analytics is the right move, especially because Oracle can offer some very valuable functionalities in this space and can draw on a large (BI) user community that is thirsty for the next step. But the most impressive move is the focus on the departmental user. Empowering business users to do their job with no / little IT involvement is what business user want and need in the fast paced 21st century. Whichever vendor will get to the business user first will create a new ‘higher ground’ that is key for long time market leadership in enterprise software.

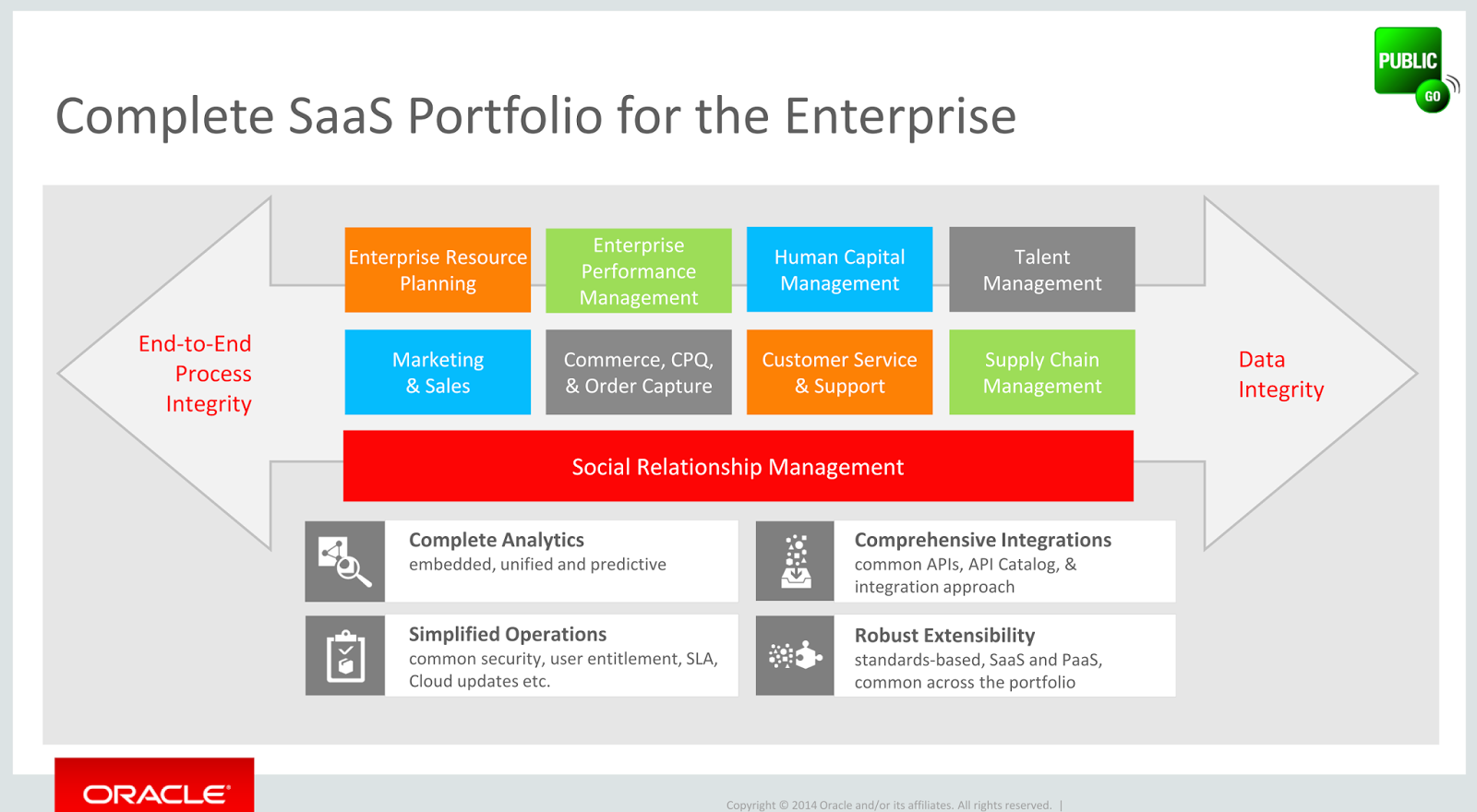

The State of SaaS

As a year ago it was back to Chris Leone to give the overall SaaS overview as it was this year– and it makes sense as Oracle HCM is the most advanced of the Oracle SaaS offerings in terms of customer adoption. The value proposition of Oracle’s SaaS offering has not changed – build an integrated suite of enterprise software with a common horizontal foundation, which enables technology offerings such as analytics and vital next generation application capabilities like social and collaboration. The main progress compared to 12 months ago has been made in Financial and ERP, where Oracle now has good customer momentum, and even the (at Oracle) traditionally lagging SCM area is catching up. Main focus going forward for the SaaS Suite will be in CX, EPM, ERP, HCM and SCM, with an overall focus and enablement of analytics.

MyPOV – For the longest time Oracle SaaS products have been lagging in functionality as Oracle took the long path to re-write these applications. 10+ years after the Fusion announcements almost all products (with the exception of SCM) are at par or more advanced than the previous suites that Oracle still sells (Oracle e-Business Suite, PeopleSoft, JD Edwards and Siebel). The strong platform capabilities and benefits show in e.g. mobile, BI, and PaaS. Along the way Oracle has also created a CX product family and is the only vendor to break out and focus stand alone on Social Relationship Management (SRM). So overall good progress – but for most business around the world orders are still the path to revenue and here Oracle needs to invest to make the overall SaaS suite fire on all cylinders and for all industries.

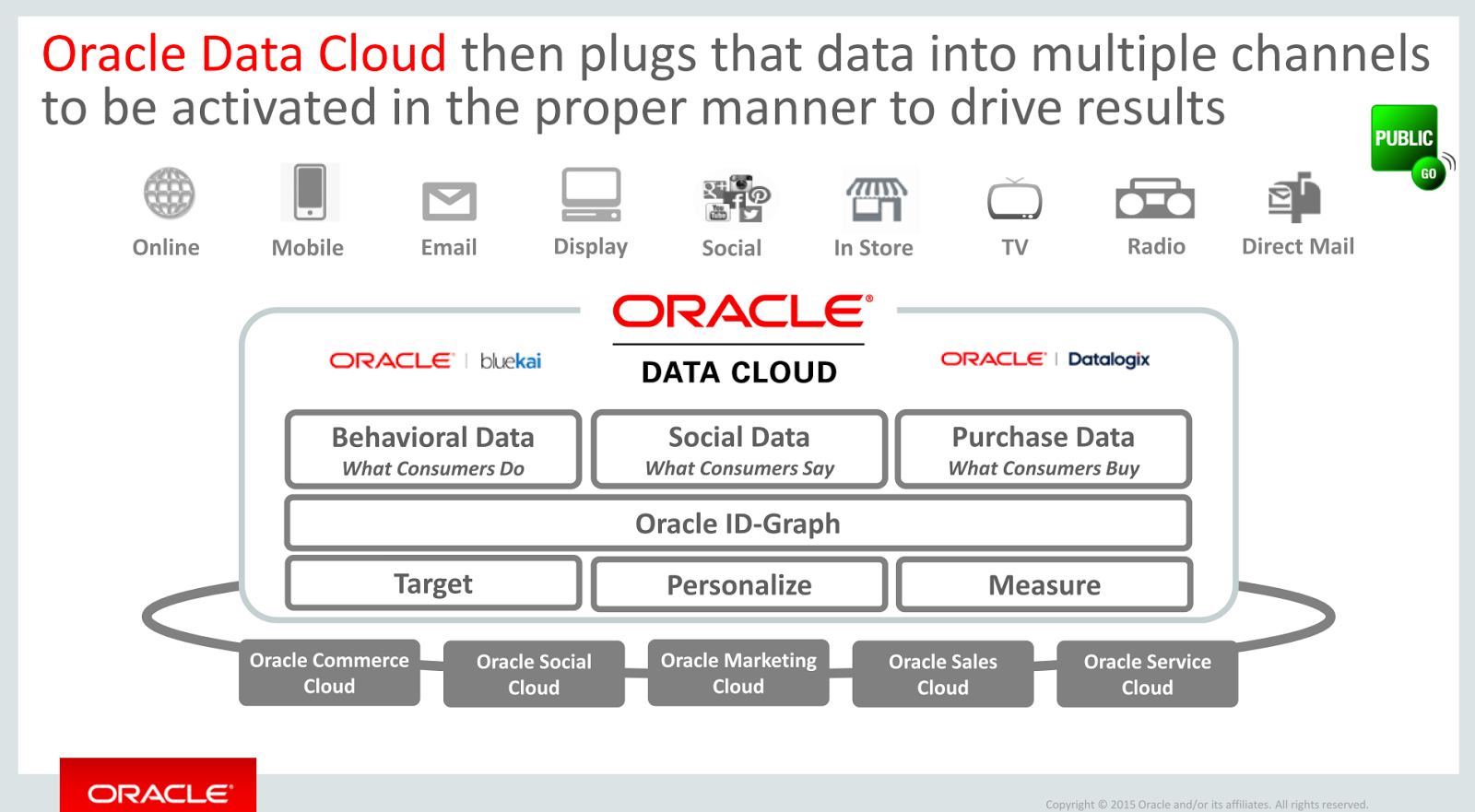

The State of DaaS

That Oracle is serious about DaaS is underlined by the fact that this is the only ‘aaS’ area that operates as its own independent GBU. The DaaS offering evolves around the Oracle ID graph, which describes individuals as completely as positively, collecting social and real world assets to compose an actionable set of data to execute value adding activities on the individual’s data. The DaaS offerings can be used standalone, but they also shore up capabilities for other Oracle SaaS properties, e.g. DaaS for Sales and DaaS for Customer Intelligence.

MyPOV – This is newest ‘aaS’ offering for Oracle, and it still sees acquisition activities (see my take on the Datalogix acquisition here). Oracle competitors don’t have similar offerings, so Oracle will do well to use DaaS as a further differentiator in other product areas – e.g. in HCM (Recruiting comes to mind), SCM (Transportation Management) etc. Oracle also needs to strike (or be more public about it) more content deals, taking e.g. a page from IBM’s playbook.

Analyst Tidbits

- One of the many new products was Oracle Process Cloud – and this one caught my attention. The product's goal is to automate business processes by enabling business users to design and implement them. It has all the characteristics of a next generation application (cloud, analytics, social, collaboration) and changing the Future of Work (no setup, fast iterations, no code). Definitely a product to watch.

- On the more mature products Oracle Integration Platform Cloud Services are interesting. Leveraging the long history of Oracle middleware is a good starting point – but adding adapters to standard business applications as pre-integration offerings will be an interesting capability to watch.

Overall MyPOV

No questions Oracle is making a lot of progress with its cloud products. And Oracle is doing a great job at making them leverage each other (I would love to see the dependency diagrams) – while making sure they have a standalone business benefit as a singular product. Oracle is also more granular than other vendors with an enterprise software or hardware background moving to the cloud, but Oracle has to make sure the offerings don’t get too complex and remain easy to understand, market, sell, and later implement and operate. It is good to see that a number of the products are gaining good customer traction and have passed the critical path of being strong standalone offerings in the marketplace. But a few other (key) products need more work this year to come to the same level – and most of that should happen this year. Last year Kurian described the Oracle cloud strategy as a two step program – getting to the critical functionality level and then differentiate the offering. A year later Oracle has reached the critical line with a number of offerings, but a lot of more work remains. The differentiation and vision remains clear – one integrated suite of as a Service products that work and operate better together – as they were built by the same vendor. The pitch that Oracle can also operate their cloud operations better than anyone else (or customers can operate them on premise, too) will be an easy one. This year’s OpenWorld should be a big one, and we will be there to analyze.

- Event Report - Oracle HCM World - Full Steam ahead, a Learning surprise and potential growth challenges - read here

- First Take - Oracle HCM World Day #1 Keynote - off to a good start - read here

- Progress Report - Oracle HCM gathers momentum - now it needs to build on that - read here

- Oracle pushes modern HR - there is more than technology - read here. (Takeaways from the recent HCMWorld conference).

- Why Applications Unlimited is good a good strategy for Oracle customers and Oracle - read here.

- News Analysis - Oracle discovers the power of the two socket server - or: A pivot that wasn't one - TCO still rules - read here

- Market Move - Oracle buys Datalogix - moves more into DaaS - read here

- Event Report - Oracle Openworld - Oracle's vision and remaining work become clear - they are both big - read here

- Constellation Research Video Takeaways of Oracle Openworld 2014 - watch here

- Is it all coming together for Oracle in 2014? Read here.

- From the fences - Oracle AR Meeting takeaways - read here (this was the last analyst meeting in spring 2013)

- Takeaways from Oracle CloudWorld LA - read here (this was one of the first cloud world events overall, in January 2013)

- Progress Report - Good cloud progress at Oracle and a two step program - read here.

- Oracle integrates products to create its Foundation for Cloud Applications - read here.

- Java grows up to the enterprise - read here.

- 1st take - Oracle in memory option for its database - very organic - read here.

- Oracle 12c makes the database elastic - read here.

- How the cloud can make the unlikeliest bedfellows - read here.

- Act I - Oracle and Microsoft partner for the cloud - read here.

- Act II - The cloud changes everything - Oracle and Salesforce.com - read here.

- Act III - The cloud changes everything - Oracle and Netsuite with a touch of Deloitte - read here.

---------------------

And here are my notes in tweets from the event:

Holger Mueller is VP and Principal Analyst for Constellation Research for the fundamental enablers of the cloud, IaaS, PaaS and next generation Applications, with forays up the tech stack into BigData and Analytics, HR Tech, and sometimes SaaS. Holger provides strategy and counsel to key clients, including Chief Information Officers, Chief Technology Officers, Chief Product Officers, Chief HR Officers, investment analysts, venture capitalists, sell-side firms, and technology buyers. Coverage Areas: Future of Work Tech Optimization & Innovation Background: Before joining Constellation Research, Mueller was VP of Products for NorthgateArinso, a KKR company. There, he led the transformation of products to the cloud and laid the foundation for new Business Process as a…...

Read morePublished

Author