Editor in Chief of Constellation Insights

Constellation Research

Larry Dignan is Editor in Chief of Constellation Insights at Constellation Research, where he leads editorial coverage focused on enterprise technology, digital transformation, and emerging trends shaping the future of business. He oversees research-driven news, analysis, interviews, and event coverage designed to help technology buyers and vendors navigate complex markets with clarity and context. ...

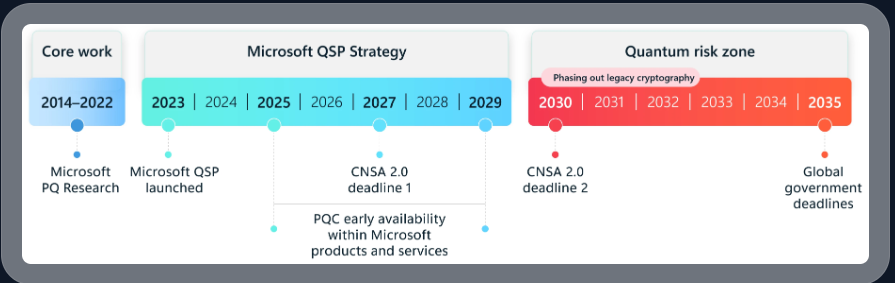

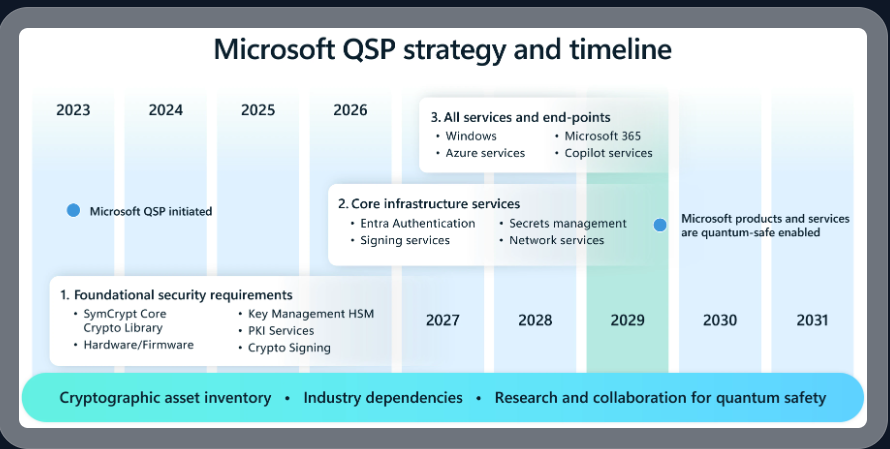

Microsoft laid out its plans to roll out post-quantum cryptography across its products and platform in a multi-year effort.

In a blog post, Microsoft introduced its Quantum Safe Program (QSP), which is a broad transformation to secure its infrastructure, customers and ecosystem against future quantum threats.

Holger Mueller, analyst at Constellation Research, said:

"The real quantum use case in 2025 is to make data centers quantum safe, which is a top priority for CxOs who need to fear that state actors will be spying on them. Microsoft is now making a key move by making all of Azure quantum safe. This move will make deployments for enterprises easier and get every Azure customer to the top level of safety. It also simplifies things for Microsoft as it can manage all its datacenters consistently."

Microsoft's QSP components include the following:

Integrating post-quantum cryptography into foundational components.

Updating products and services to prevent future quantum risks. Microsoft said it will integrate post-quantum cryptography across Azure, Entra Authentication, Microsoft 365 and more.

Align QSP with US government requirements and timelines for quantum safety.

Complete the transition to post-quantum cryptography by 2033, two years ahead of the deadline set by most governments.

In the blog post, Microsoft noted:

"Migration to post quantum cryptography (PQC) is not a flip-the-switch moment, it’s a multiyear transformation that requires immediate planning and coordinated execution to avoid a last-minute scramble.

It is also an opportunity for every organization to address legacy technology and practices and implement improved cryptographic standards. By acting now, organizations can upgrade to modern cryptographical architectures that are inherently quantum safe, upgrade existing systems with the latest standards in cryptography, and embrace crypto-agility (the ability to easily change algorithms) to modernize their cryptographic standards and practices and prepare for scalable quantum computing."

Here's a look at where Microsoft sits today and the roadmap ahead.

Editor in Chief of Constellation Insights

Constellation Research

Larry Dignan is Editor in Chief of Constellation Insights at Constellation Research, where he leads editorial coverage focused on enterprise technology, digital transformation, and emerging trends shaping the future of business. He oversees research-driven news, analysis, interviews, and event coverage designed to help technology buyers and vendors navigate complex markets with clarity and context. ...

Human capital management software provider Dayforce is going private in a deal with Thoma Bravo valued at $12.3 billion.

The news, which had leaked out earlier this week, comes as Dayforce plays in a crowded HCM space. Thoma Bravo has a broad portfolio of enterprise software vendors including Coupa, Flexera, Conga, Darktrace and others.

Under the terms of the deal, Dayforce shareholders will get $70 per share in cash, good for a 32% premium over the August 15 closing price. The Thoma Bravo purchase includes a minority investment from the Abu Dhabi Investment Authority.

David Ossip, CEO of Dayforce, said the move to grow private will "accelerate our business - with our focus, resources, and product innovation all laser-pointed on leaping forward as the HCM leader for a world of work shaped by AI."

The deal is expected to close in early 2026.

Dayforce was formerly known as Ceridian. In 2012, Ceridian acquired Dayforce, a cloud HCM player. In 2018, Ceridian went public with a focus on Dayforce. The company took on the Dayforce brand in 2024.

The company reported second quarter net income of $21.3 million on revenue on $464.7 million, up 10% from a year ago. Dayforce has 6,984 customers on its platform.

Dayforce projected 2025 revenue between $1.935 billion and $1.955 billion.

Constellation Research's take

Holger Mueller, an analyst at Constellation Research, said:

"The investment from Thomas Bravo comes somewhat as a surprise - as Dayforce is on a roll. With its interational expansion Dayforce has quickly become an alternative to the larger SAP, Oracle and Workday - three giants that all do not offer as in depth workforce managment. On the other side, Dayforce is on a massive investment jouney, adding compliance, workforce management and payroll for 40 countries. The additional funding from Thomas Bravo may be be able to accelerate the R&D effort and possibly go beyond. Building sales and marketing presence is not a small investment either. The bottom line is - if the strategy remains largefly unchained, we will see a turbocharged Dayforce soon."

Editor in Chief of Constellation Insights

Constellation Research

Larry Dignan is Editor in Chief of Constellation Insights at Constellation Research, where he leads editorial coverage focused on enterprise technology, digital transformation, and emerging trends shaping the future of business. He oversees research-driven news, analysis, interviews, and event coverage designed to help technology buyers and vendors navigate complex markets with clarity and context. ...

Wipro said it will acquire Harman's Digital Transformation Solutions (DTS) unit for $375 million in a move that will give the services firm more engineering and research and development reach.

Harman is a unit of Samsung. Samsung bought Harman in 2016 for $8 billion in a move that would expand its audio technology as well its reach into auto infotainment, telematics and connected safety systems.

By selling Harman DTS to Wipro, Samsung gets to focus on the technology with Wipro focusing on services for key industries. Wipro will get 5,600 DTS employees in the deal as well as the leadership team. Harman DTS serves telecom, industrial, life sciences, hospitality and retail verticals.

Srini Pallia, CEO of Wipro, said DTS will give the company "specialized engineering expertise" that can be combined with the company's AI and consulting business. DTS will give Wipro heft in domain-led design, connected products, accelerators and autonomous agents.

As part of the purchase, Wipro entered a multi-year pact with Harman and Samsung. DTS will be integrated into Wipro's engineering global business unit. The deal is expected to close before the end of 2025.

Constellation Research's take

Constellation Research analyst Chirag Mehta said:

“Engineering R&D (ER&D) fueled by AI is now a primary battleground for global enterprises seeking to accelerate innovation and stay competitive in a fast-evolving market. Wipro’s acquisition of Harman’s DTS business—bringing over 5,600 engineers across the Americas, Europe, and Asia—significantly enhances their digital engineering capabilities with deep domain-led design, connected-product expertise, AI-native platforms, and proprietary accelerators .

The broader industry context underscores why GSIs are doubling down here: Cognizant’s recent acquisition of Belcan, an established aerospace and defense engineering leader, reflects the same urgency to capture high-value ER&D opportunities where domain depth and scale matter. By merging specialist strength with global reach, GSIs are positioning themselves to deliver end-to-end engineering services that combine consulting, design, and AI-native execution.

In this light, Wipro’s move is not just about capacity—it’s about competing in a new wave of engineering services where clients demand agility, IP-rich platforms, and the assurance of global scale. The ER&D market is evolving into the next frontier of growth for services firms, and this acquisition marks a critical step in redefining how engineering innovation is delivered worldwide.”

Editor in Chief of Constellation Insights

Constellation Research

Larry Dignan is Editor in Chief of Constellation Insights at Constellation Research, where he leads editorial coverage focused on enterprise technology, digital transformation, and emerging trends shaping the future of business. He oversees research-driven news, analysis, interviews, and event coverage designed to help technology buyers and vendors navigate complex markets with clarity and context. ...

Target's incoming CEO Michael Fiddelke is betting that AI, technology and process optimization will return the company to growth while navigating economic uncertainty.

Fiddelke's earnings call debut coincided with a disappointing second quarter. Fiddelke is currently chief operating officer and has been in various roles at Target for 20 years. Wall Street wasn't pleased an insider got the job and current CEO Brian Cornell will stay through the end of the year. Fiddelke takes over at the start of Target's fiscal 2026 in January.

To be sure, Target faces more than a few challenges. Target reported second quarter earnings of $2.05 a share on revenue of $25.2 billion, down 0.9% from a year ago, but slightly ahead of Wall Street estimates. Same store sales in the second quarter were down 1.9%, but digital comparable sales were up 4.3% due to same-day delivery via Target Circle 360.

As for the fiscal 2025 outlook, Target said it expects a low-single digit decline in sales and earnings of $8 a share to $10 a share. Adjusted earnings will be $7 a share to $9 a share due to litigation settlements.

Target plans to spend about $4 billion in capital expenditures to open new stories, remodel existing ones and invest in supply chain and technology.

Fiddelke, who has led Target's Enterprise Acceleration Office, said he's stepping in as CEO with "a clear and urgent commitment to build new momentum in the business and get back to profitable growth."

The topline plan for Target includes the following:

Reestablish merchandising authority to improve product selection.

Create an "elevated experience" to give guests "a sense of joy from every trip to Target."

Use technology to improve speed, guest experience and efficiency.

Technology, with a heavy dose of AI, will span everything from sourcing to supply chain and customer experience. "While technology is at the core of all our operations today, it will need to play an even stronger role going forward," said Fiddelke. "As we continue investing in our future growth, we'll be making key technology investments throughout our stores, supply chain, headquarters and digital operations to power our team and our business."

Details were sparse, but the big picture is that Fiddelke wants to move faster, reevaluate strategies continuously and be nimble enough to react to the tariff and consumer landscape. Target's enterprise acceleration office is designed to scale best practices and technologies.

"We've identified the biggest challenges that slow us down, legacy technology that doesn't meet today's needs, manual work that can be automated, unclear accountabilities, slow decision-making, siloed goals and a lack of access to quality data. For example, it's clear that at our headquarters, team structures and processes have significant opportunities to improve," said Fiddelke. "We started redesigning large cross-functional processes like how our teams build our merchandising and inventory plans to clarify roles and access the right data to make more effective decisions."

Fiddelke said Target is doing the following:

Embedding more technology and data to evaluate initiatives with the highest returns.

Leverage AI and other tools for better forecasting.

The company has deployed more than 10,000 new AI licenses across its employee base.

"Solving these challenges will require changes, both big and small, across technology and data, process and structures and organizational behaviors," said Fiddelke.

Fiddelke moved to address the perception that he isn't an agent of change. He said, "there's real power in drawing on 20 years of knowing what makes Target, Target."

"Having seen us at our very best in different chapters gives me a clear focus on who we are in retail and what our unique path is that's going to lead to growth. And it centers on style and design," said Fiddelke.

Now all Fiddelke has to do is leverage technology to revamp Target's store fulfillment "in a capital light way" and offset tariffs by becoming more efficient.

Editor in Chief of Constellation Insights

Constellation Research

Larry Dignan is Editor in Chief of Constellation Insights at Constellation Research, where he leads editorial coverage focused on enterprise technology, digital transformation, and emerging trends shaping the future of business. He oversees research-driven news, analysis, interviews, and event coverage designed to help technology buyers and vendors navigate complex markets with clarity and context. ...

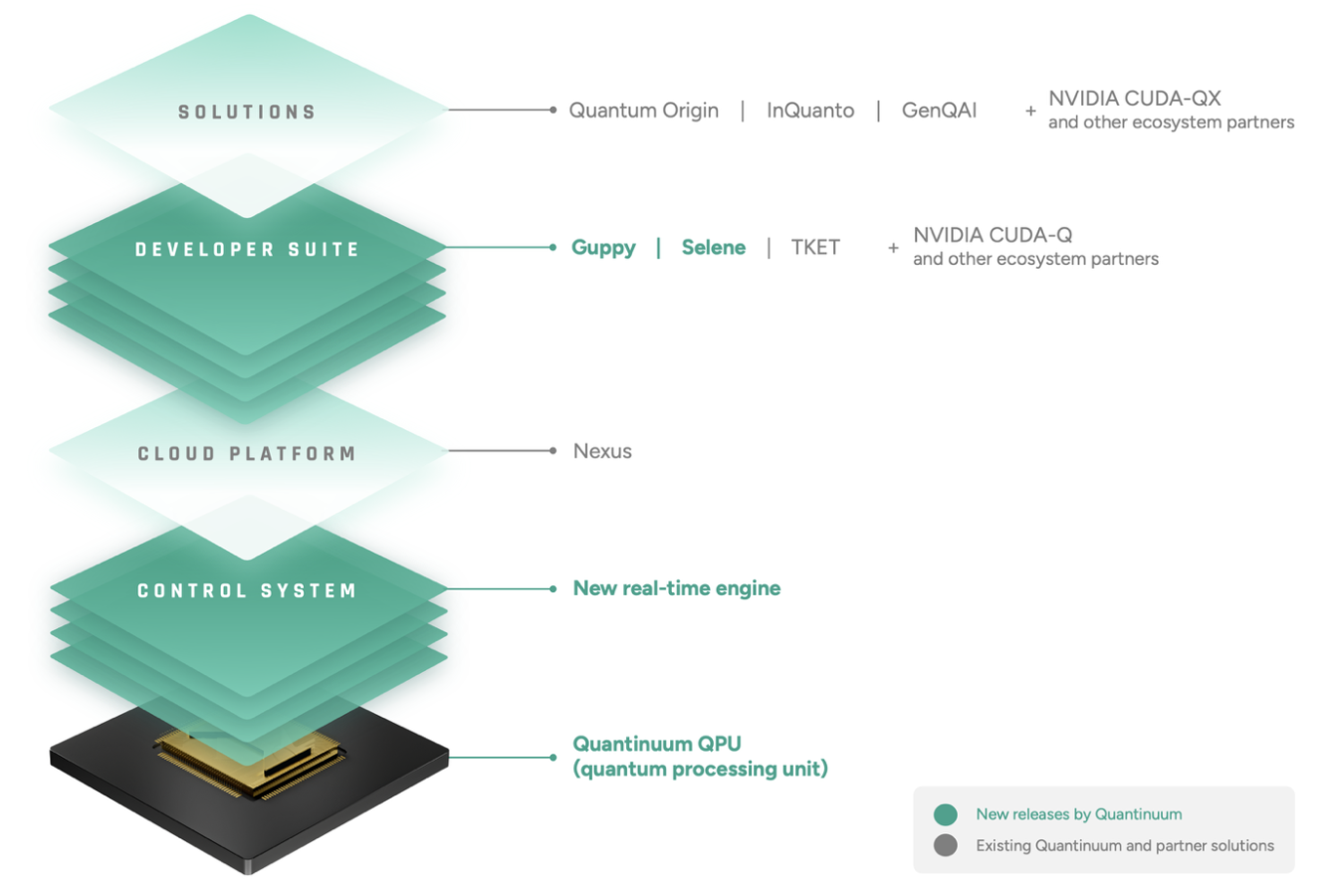

Guppy, an open-source language hosted inside Python. Guppy enables quantum computing programming above the gate level using conditional logic and the ability to incorporate any quantum error correction code.

Selene, which is an emulator that models realistic, entangled quantum behavior. The goal is to make quantum software research and development easier.

Quantinuum is prepping its software stack for the launch of Helios, the company's next-gen quantum computer. Helios will require a new software stack that can speed up quantum computing use cases.

Guppy and Selene will join TKET, an open-source tool kit for developers and Nexus, a platform to access quantum computing systems. Going forward, Guppy will run software applications on new systems. TKET will be used to optimize Guppy programs. Nexus will be the primary vehicle to accessing Quantinuum hardware, support Guppy and provide access to Selene.

Editor in Chief of Constellation Insights

Constellation Research

Larry Dignan is Editor in Chief of Constellation Insights at Constellation Research, where he leads editorial coverage focused on enterprise technology, digital transformation, and emerging trends shaping the future of business. He oversees research-driven news, analysis, interviews, and event coverage designed to help technology buyers and vendors navigate complex markets with clarity and context. ...

Certinia, which provides management software for professional services organizations, delivered its first installment of AI agents built on Salesforce's Agentform platform as part of its summer release. Learn more in the interview with Certinia's Chief Product and Digital Officer, Raju Malhotra, and Constellation's Editor in Chief, Larry Dignan.

Editor in Chief of Constellation Insights

Constellation Research

Larry Dignan is Editor in Chief of Constellation Insights at Constellation Research, where he leads editorial coverage focused on enterprise technology, digital transformation, and emerging trends shaping the future of business. He oversees research-driven news, analysis, interviews, and event coverage designed to help technology buyers and vendors navigate complex markets with clarity and context. ...

Databricks said it raised more funding in a Series K round with a valuation topping $100 billion.

The company said the funding was from existing investors. In a release, Databricks, which has more than 15,000 customers, didn't disclose how much it raised or its annual revenue run rate, which was put at $3 billion late last year.

According to Databricks, the new capital will accelerate its AI strategy via expanding Agent Bricks and investing in its Lakebase database. CEO Ali Ghodsi said the company is "seeing tremendous investor interest.

Databricks launched Agent Bricks in June and Lakebase, which is optimized for AI agents. The company said that the new funding will also be used for future AI acquisitions and AI research.

Databricks has been busy expanding partnerships with the likes of Microsoft, Google Cloud, Anthropic, SAP and Palantir.

Constellation Research analyst Holger Mueller said:

"Data is the foundation for AI and Databricks' strong data story is driving its valuation. Beyond the data Datbricks will now have to demonstrate it is not only about analytics, but can also be the platform for AppDev and Agent building. Another aspect will be whether Databricks can be successful with its SAP partnership - and repeat similar partnerships with other key data sources - starting with the ERP vendors."

Editor in Chief of Constellation Insights

Constellation Research

Larry Dignan is Editor in Chief of Constellation Insights at Constellation Research, where he leads editorial coverage focused on enterprise technology, digital transformation, and emerging trends shaping the future of business. He oversees research-driven news, analysis, interviews, and event coverage designed to help technology buyers and vendors navigate complex markets with clarity and context. ...

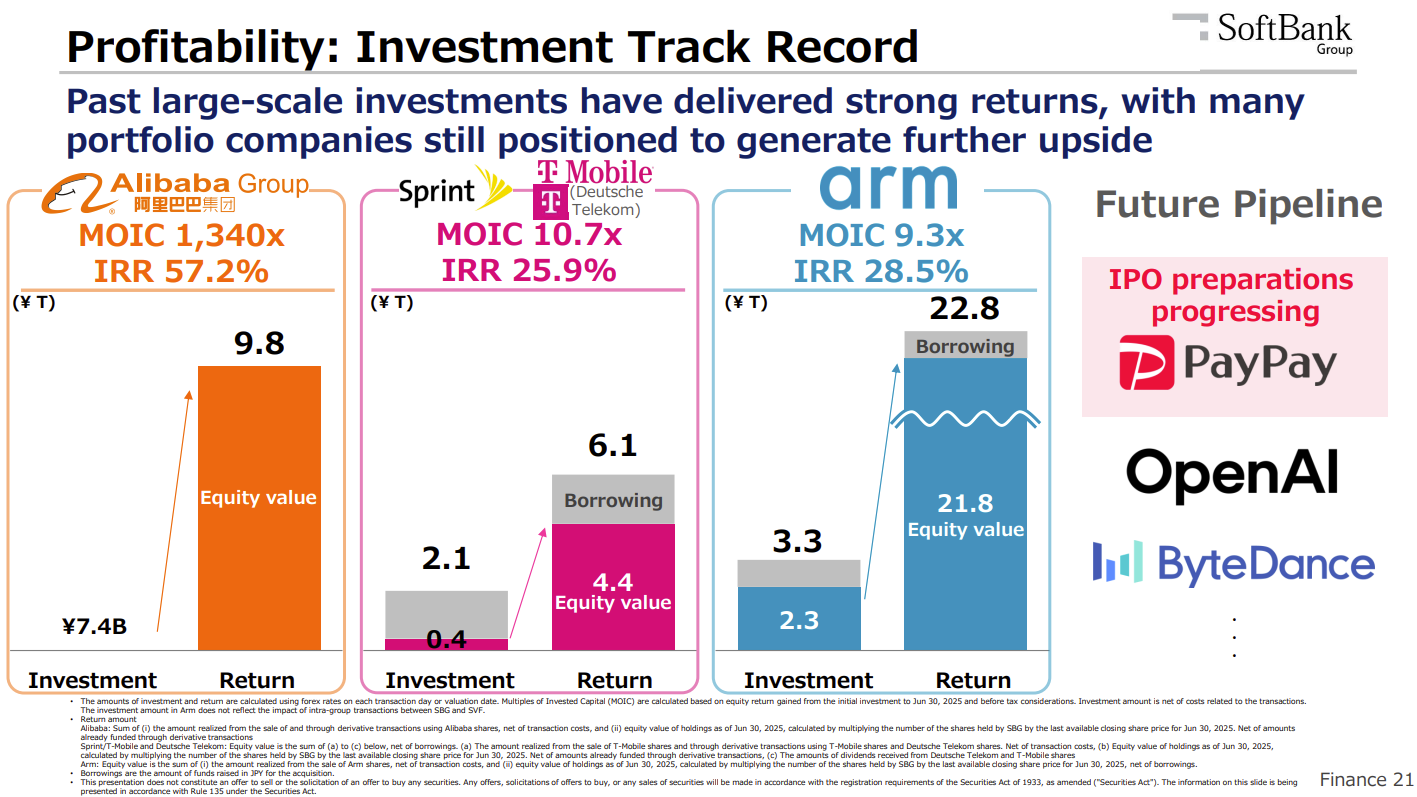

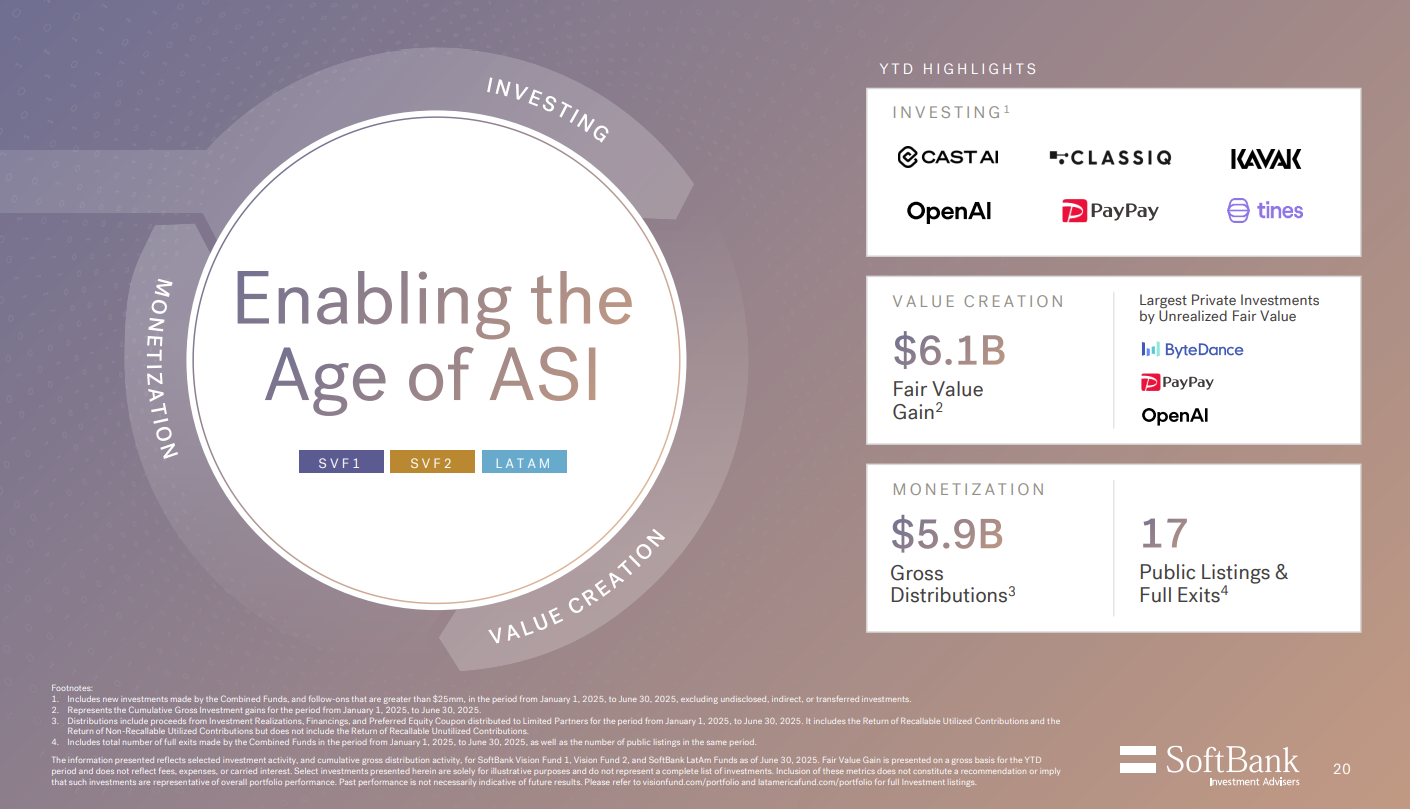

Softbank will invest $2 billion into Intel at $23 a share in a deal may be a value-oriented investment as well as a head scratcher. Perhaps the biggest question for Softbank is this: Why?

After all, Softbank already has skated to where the puck is going. Softbank has bet big on AI, owns Arm and a big chunk of OpenAI. Arm is the architecture beating Intel into a pulp in recent years. Nvidia and AMD have been running circles around Intel on servers, PCs and GPUs too. By the way, Softbank has an investment in Nvidia too and is closing a $6.5 billion purchase of Ampere.

Unless Softbank just wants to collect chipmaker stocks there has to be a reason right?

Softbank CEO Masayoshi Son said: "For more than 50 years, Intel has been a trusted leader in innovation. This strategic investment reflects our belief that advanced semiconductor manufacturing and supply will further expand in the United States, with Intel playing a critical role."

Son would be believable if it didn't already bet on the winning semiconductor horses.

Softbank Group CFO Yoshimitsu Goto, who is also CISO, Head of legal, Admin & Finance Unit and Group Compliance Officer & Director, spent a lot of time talking about Arm on its second quarter earnings call. Arm plans to pour money into R&D and design its own processors.

Goto said:

"We actually encourage Arm to spend the money for future growth. From business perspective, compute subsystem, or CSS, is a key driver, and CSS is an integrated IP package that includes multiple Arm CPUs. And CSS helps customers shorten development time and reduce cost."

Goto noted that about half of the server chips launched by major hyperscalers will be Arm based this year. Enterprises are also gravitating to Arm. "Arm is quickly becoming the core platform for the AI era, cloud infrastructure," said Goto.

Why buy Intel then? Maybe it's just $2 billion among friends.

Lip-Bu Tan, CEO of Intel, said: "SoftBank, a company that’s at the forefront of so many areas of emerging technology and innovation and shares our commitment to advancing U.S. technology and manufacturing leadership. Masa and I have worked closely together for decades, and I appreciate the confidence he has placed in Intel with this investment."

There's probably some truth to Softbank helping out Intel for the good of the ecosystem and Tan. But there are some other reasons worth pondering. Here are a few thoughts.

Intel has manufacturing assets in the US and needs a bailout. Softbank is involved with AI heavily and may need future capacity for Stargate. Sure, Intel Foundry is a sinkhole right now, but if the AI boom plays out then that capacity will be useful to Arm or any one of Softbank's investments. Stargate Project sites under due diligence, says SoftBank

The investment buys goodwill so it's politically savvy. Intel, and Tan, has been in the political crossfire of late. Softbank is playing ball and investing in the US. The investment in Intel buys some US credibility.

Downside risk is limited. Softbank plays on a massive boom-bust scale and $2 billion is a paltry sum. Intel may recover and if it does Softbank will do well. If Intel doesn't Softbank has paid $2 billion for intangibles. Either way it doesn't matter much since $2 billion is spare change.

Editor in Chief of Constellation Insights

Constellation Research

Larry Dignan is Editor in Chief of Constellation Insights at Constellation Research, where he leads editorial coverage focused on enterprise technology, digital transformation, and emerging trends shaping the future of business. He oversees research-driven news, analysis, interviews, and event coverage designed to help technology buyers and vendors navigate complex markets with clarity and context. ...

Certinia, which provides management software for professional services organizations, delivered its first installment of AI agents built on Salesforce's Agentforce platform as part of its summer release.

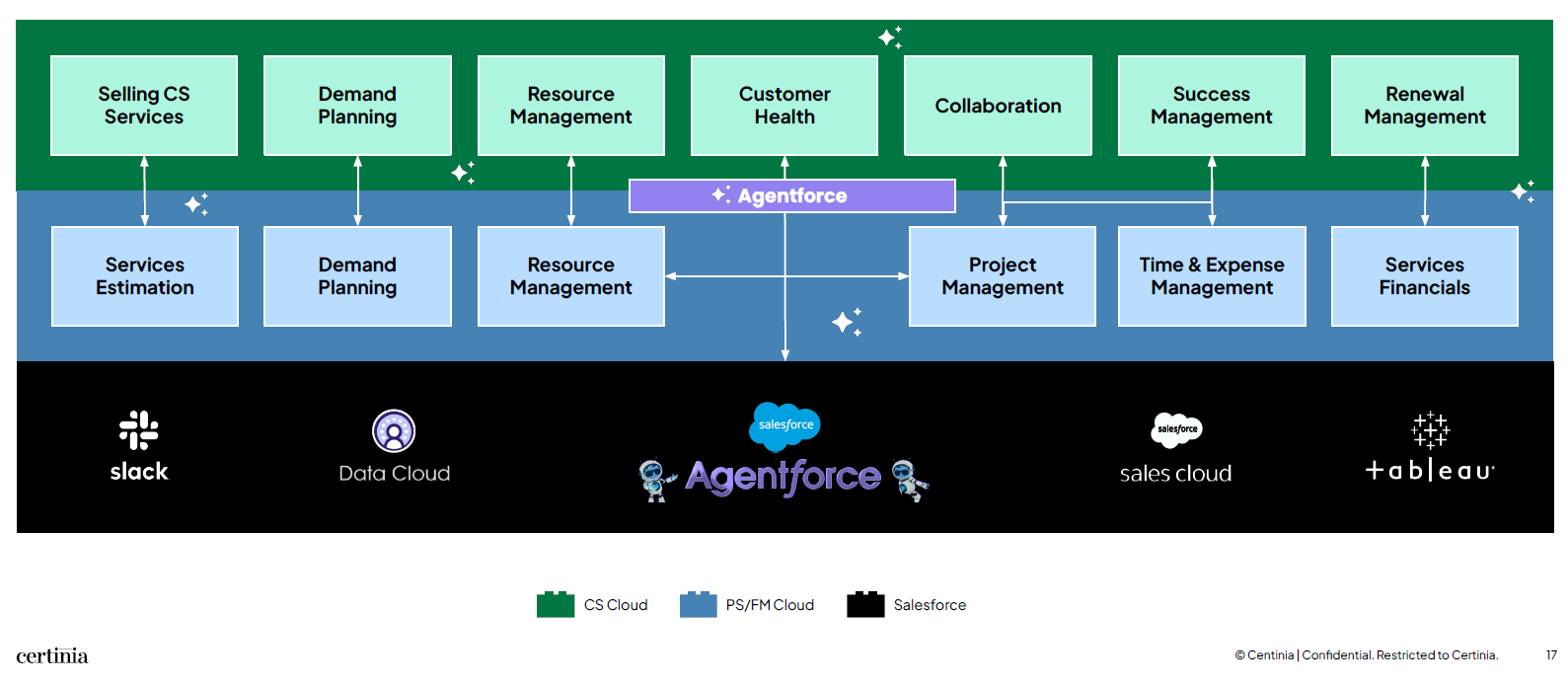

The company has three primary clouds--Professional Services (PS) Cloud, Financial Management Cloud and Customer Success (CS) Cloud--with Certinia AI layered throughout. Certinia, previously known as FinancialForce, is looking to address customers' need for productivity, AI innovation and rising labor costs. Certinia's platform plugs into enterprise ERP and CRM systems.

DJ Paoni, CEO of Certinia, set the backdrop. "Leaders are being asked to do more with fewer resources, and they know they need to hit the targets. They need better alignment across the whole company, sales, services, customer success. And interestingly, while most leaders agree that tight collaboration across these functions would drive higher margins and retention, only about a third are executing on it," said Paoni, speaking on an analyst briefing. "This gap of what you say and what we do is often a result of disconnected systems and processes that can create friction between all the different teams that you have."

According to Paoni, AI is what will be able to close the gap between promises and actual delivery. In the big picture, Certinia is betting that it can turn professional services organizations into profit centers instead of a cost center with a big assist from autonomous systems, said Paoni.

Raju Malhotra, Chief Product and Technology Officer at Certinia, said the company's vision is to "empower technology and services organizations to deliver customer value with certainty." The company has been building out its platform and its CS Cloud became generally available at Salesforce Dreamforce 2024.

Here's a look at the Certinia platform, which is designed to cover the services continuum from services estimating, resource and project management, billing, revenue management, collaboration and planning and analytics.

Certinia kicks off its agent parade

With its 2025 summer release, Certinia launched two AI agents, which were built on Salesforce's Agentforce platform, available for early adopters. Certinia will launch more agents in future releases.

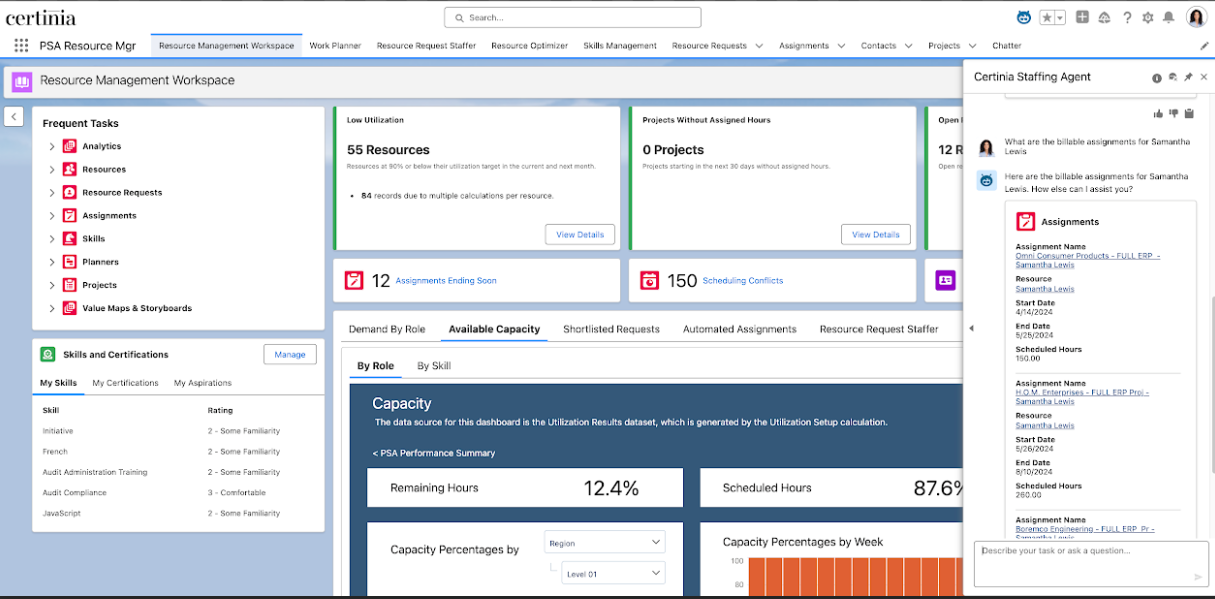

The newly released AI agents include the Certinia Staffing Agent and the Certinia Customer Success Agent.

Malhotra said resource managers need an easier way to reallocate work when someone is out for a period of time to ensure projects remain on track.

Typically, a manual process searches for a resource's assignments and then workflows start to find a qualified replacement.

Certinia's Staffing Agent aims to begin resource allocation with a conversation. The staffing agent is native to Certinia's Professional Services (PS) Cloud. The agent will find billable assignments and provide a shortlist of suitable replacements. Once a manager makes a decision, the agent reallocates the work.

According to Malhotra, Certinia's early adopters have seen the new AI agents "reduce what used to take them hours into a few minutes."

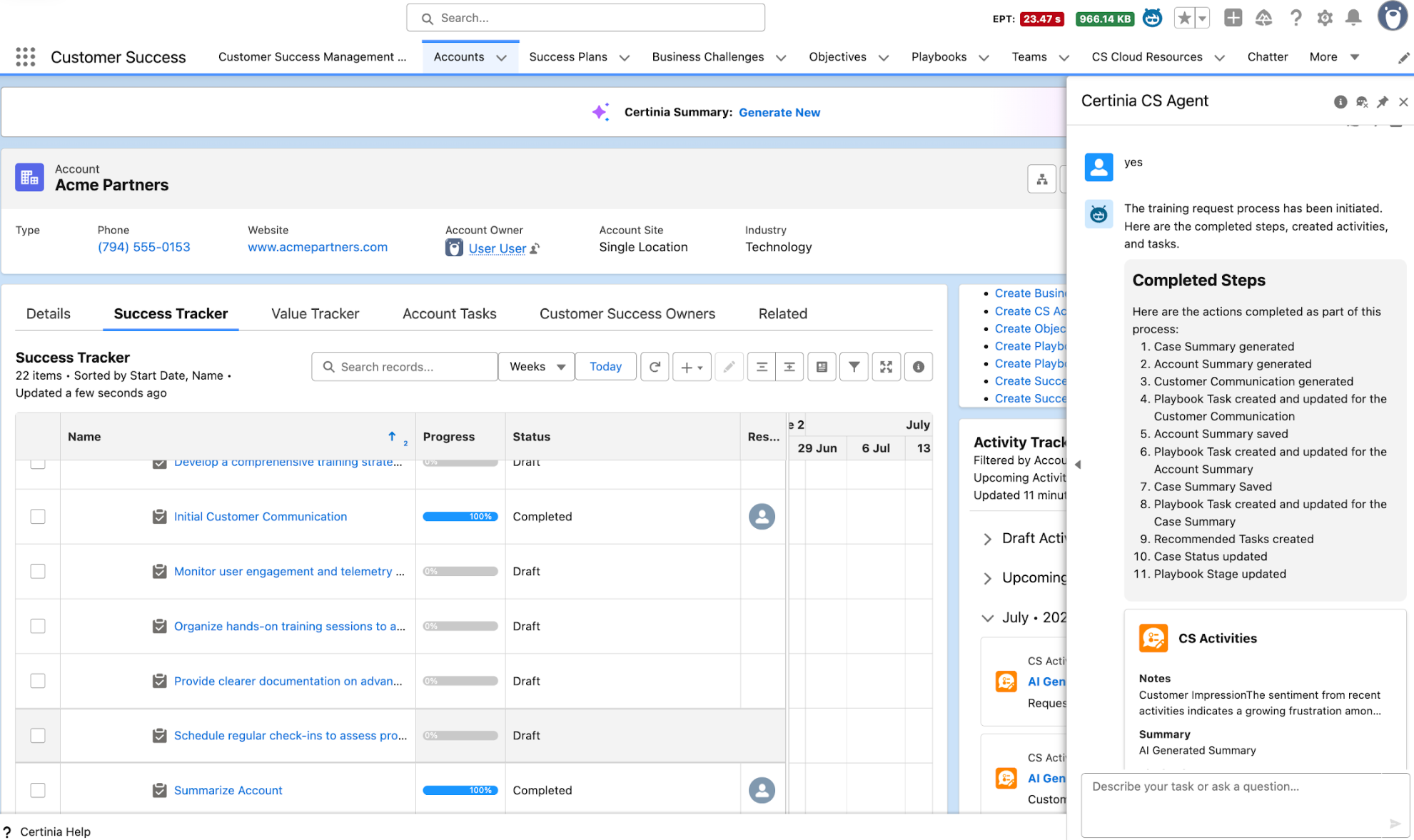

The company's second AI agent is Certinia Customer Success Agent, which aims to automate grunt work for customer success managers.

Certinia's Customer Success Agent is designed to enable success managers to cover more accounts in pooled models. The agent does the prep work for a case and provides a summary, drafts email to customer and creates a task list. When the work is finished, the agent handles closing admin tasks.

Malhotra said the two agents in the 2025 Summer release are just the start. Certinia is experimenting with more than 50 AI agents that will be built into the company's professional services automation software.

Certinia was an inaugural launch partner for the Salesforce Agentforce Partner Network and now is a Salesforce Agentforce Model Context Protocol (MCP) Partner.

Building on Agentforce

Since Certinia is built on the Salesforce platform and an early adopter of Agentforce, Malhotra has a front-row seat to how the AI agent market is developing. Key points:

Certinia's Staffing Agent and Customer Success Agent are built on Agentforce. "Agentforce has evolved from 1.0 to 2.0 and now it's the 3.0 and in terms of capabilities, has really come a long way," said Malhotra.

Building agents requires a strong foundation and focus on data quality, integrity and unification across disparate systems. Certinia leverages the Salesforce platform and Data Cloud but expects to work in third-party data sources on behalf of customers. "We expect that that this is a very heterogeneous environment. So, we expect that heterogeneity of data, system workflows, and we work within that construct, to make sure the personas we are serving have a very unified view of the data that they want to act on," said Malhotra.

AI agent platforms are developing rapidly and Certinia has a wish list that's often shared with the Salesforce platform team. Wish list items for Agentforce include improved ISV capabilities (packaging, monetization, telemetry), agent orchestration, performance and scalability, and enhanced enterprise security, said Malhotra.

As for Malhotra's wishlist for Agentforce. Here's a look at his punch list.

More data and tools to run Agentforce natively with independent software vendors. Malhotra said Salesforce has been working closely ISVs, but needs to hone the packaging, monetization and telemetry and reporting for Agentforce so partners can make it available natively.

Data quality and integration. Malhotra emphasized the critical importance of having high-quality, unified data from disparate systems. He noted that building effective agents requires a comprehensive view of data from various sources including CRM, financial systems, and other enterprise applications to properly manage services projects.

Orchestration build out. Agent orchestration is going to be critical as Salesforce agents work with Certinia agents and then connect to others. To scale, orchestration via Agent2Agent or Model Context Protocol (MCP) will be critical.

Enterprise readiness, namely security. "Security is a big construct," said Malhotra. "We really need to think about security in a much more specific and significant way so it's baked into the platform." He said that security efforts go beyond Salesforce and Certinia and need to be an ecosystem effort on every level of the stack.

Certinia also launched a set of AI enhancements with the latest platform release. Throughout Certinia's clouds, the company has rolled out features to enhance resource management, optimize budgets and plans and simplify tax planning.

Here's a look:

AI-generated success plans in CS Cloud. The company said generative AI additions can create customer success plans and objectives from sales opportunities and business challenges. The plans connect sales, services and success teams in one place.

AI-generated summaries in PS Cloud. Certinia said genAI additions will provide project overview summaries, and individual summaries for deliverables, financials, risks, assumptions, issues and dependencies.

Automated project staffing. The latest Certinia release now has the ability to automatically hold or assign a resource request to reduce the time to staff.

Enhanced KPI tracking dashboards in CS Cloud with the ability to post a Value Tracker on customer community portals.

Estimate Control in PS Cloud with the ability to accelerate deal closing and modify estimates at once with discounts and billing schedules.

Editor in Chief of Constellation Insights

Constellation Research

Larry Dignan is Editor in Chief of Constellation Insights at Constellation Research, where he leads editorial coverage focused on enterprise technology, digital transformation, and emerging trends shaping the future of business. He oversees research-driven news, analysis, interviews, and event coverage designed to help technology buyers and vendors navigate complex markets with clarity and context. ...

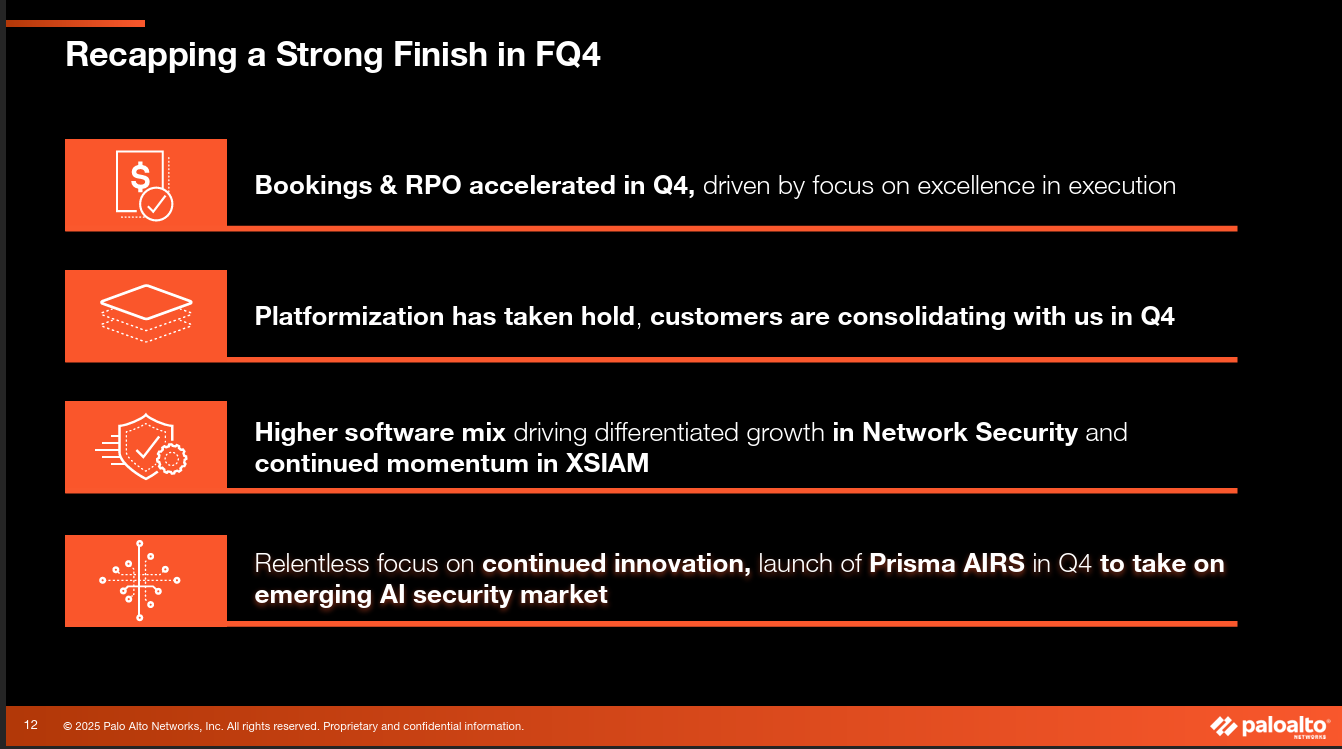

Palo Alto Networks reported better-than-expected fourth quarter earnings and projected revenue growth of about 14% for the fiscal year ahead.

The cybersecurity company reported fourth quarter earnings of $253.8 million, or 36 cents a share, on revenue of $2.5 billion, up 16% from a year ago. Non-GAAP earnings for the quarter were 95 cents a share.

Wall Street was expecting Palo Alto Networks to report fourth quarter non-GAAP earnings of 88 cents a share on revenue of $2.5 billion.

For fiscal 2025, Palo Alto Networks reported earnings of $1.134 billion, or $1.60 a share, on revenue of $9.22 billion.

CEO Nikesh Arora said the company executed well in the fourth quarter and looking for platforms that "are designed to work in concert." Arora said remaining performance obligation (RPO) is accelerating into the new fiscal year and signaling growth.

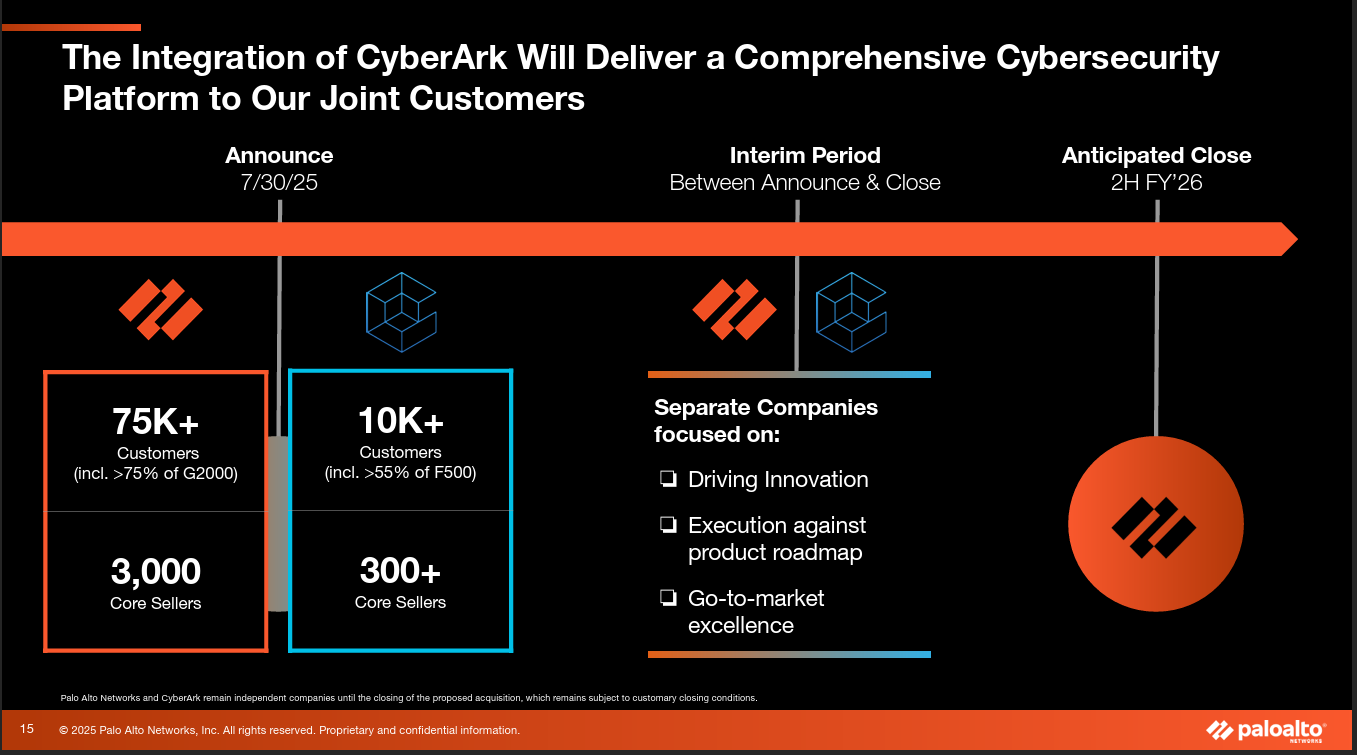

The company has been on a bit of a buying spree with the acquisition of CyberArk for $25 billion.

Separately, Palo Alto Networks said that CTO Nir Zuk will retire. Lee Klarich, Chief Product Officer (CPO), will also take on the CTO role. Zuk founded the company in 2005.

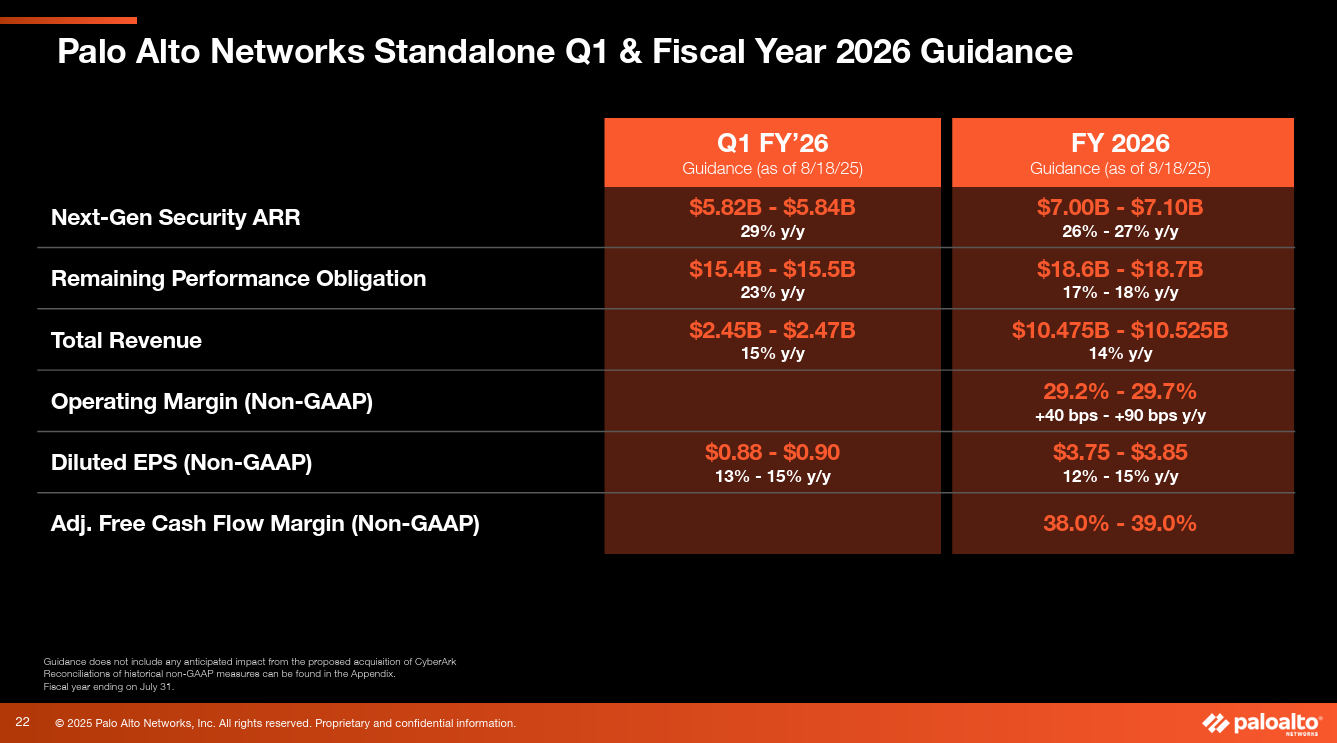

As for the outlook, Palo Alto Networks said first quarter revenue will be between $2.45 billion to $2.47 billion, up 15% with non-GAAP earnings of 88 cents a share to 90 cents a share. Remaining performance obligation is expected to be $15.4 billion to $15.5 billion, up 23% from a year ago.

For fiscal 2026, Palo Alto Networks projected revenue of $10.475 billion to $10.525 billion, up 14% from a year ago. Non-GAAP earnings for the fiscal year are expected to be $3.75 a share to $3.85 a share. Remaining performance obligation will be between $18.6 billion and $18.7 billion, up 17% to 18%.

Key points from Arora on the conference call:

"The only way to get near real time is to have some consistency in your platform where data talks to each other and you're able to run agents on top of it. I can't run agents on top of disparate infrastructure. There's no agent out there that understands three different firewall vendors and infrastructure to SASE vendors, a browser vendor, and seven other vendors on top. Agenting is only going to make this worse, because there are agents that bad actors can deploy to try and reach it."

"We expect our top line seasonality to continue to be second half and four weighted as we continue to compromise with our customers."

"The reason we highlighted a $50 million ARR deal, that's a big number in technology, whether it's cybersecurity, anything else that tells it the art of the possible. If one was able to consolidate the entire security span of a large customer, you can get up to $50 million in ARR."

"AI is going to act as an accelerant towards a desire to consolidate customers are beginning to feel the value of consolidated data, not just in security, in other areas, you can see."