Constellation Research Presents the 2024 Enterprise Awards

Constellation Research Presents the 2024 Enterprise Awards

About Liz Miller: Liz Miller is Vice President and Principal Analyst at Constellation, focused on the org-wide team sport known as customer experience. While covering CX as an enterprise strategy, Miller spends time zeroing in on the functional demands of Marketing and Service and the evolving role of the Chief Marketing Officer, the rise of the Chief Experience Officer, the evolution of customer engagement, and the rising requirement for a new security posture that accounts for the threat to brand trust in this age of AI. With over 30 years of marketing experience, Miller offers strategic guidance on the leadership, business transformation, and technology requirements to deliver on today’s CX strategies. She has worked with global marketing organizations to transform everything from…...

Read more

About Andy Thurai Andy Thurai is an accomplished IT executive, strategist, advisor, enterprise architect and evangelist with more than 25 years of experience in executive, technical, and architectural leadership positions at companies such as IBM, Intel, BMC, Nortel, and Oracle. Andy has written more than 100 articles on emerging technology topics for publications such as Forbes, The New Stack, AI World, VentureBeat, DevOps.com, GigaOm and Wired. Andy’s fields of interest and expertise include AIOps, ITOps, Observability, Artificial Intelligence, Machine Learning, Cloud, Edge, and other enterprise software. His strength is selling technology to the CxO audience with a value proposition rather than the usual technology sales pitch. Find more details and samples of Andy’s work on his…...

Read more

Doug Henschen is former Vice President and Principal Analyst where he focused on data-driven decision making. Henschen’s Data-to-Decisions research examines how organizations employ data analysis to reimagine their business models and gain a deeper understanding of their customers. Henschen's research acknowledges the fact that innovative applications of data analysis requires a multi-disciplinary approach starting with information and orchestration technologies, continuing through business intelligence, data-visualization, and analytics, and moving into NoSQL and big-data analysis, third-party data enrichment, and decision-management technologies. Insight-driven business models are of interest to the entire C-suite, but most particularly chief executive officers, chief digital officers,…...

Read more

Larry Dignan is Editor in Chief of Constellation Insights at Constellation Research, where he leads editorial coverage focused on enterprise technology, digital transformation, and emerging trends shaping the future of business. He oversees research-driven news, analysis, interviews, and event coverage designed to help technology buyers and vendors navigate complex markets with clarity and context. ...

Read more

R “Ray” Wang is the CEO of Silicon Valley-based Constellation Research Inc. He co-hosts DisrupTV, a weekly enterprise tech and leadership webcast that averages 50,000 views per episode and blogs at www.raywang.org. His ground-breaking best-selling book on digital transformation, Disrupting Digital Business, was published by Harvard Business Review Press in 2015. Ray's new book about Digital Giants and the future of business, titled, Everybody Wants to Rule The World was released in July 2021. Wang is well-quoted and frequently interviewed by media outlets such as the Wall Street Journal, Fox Business, CNBC, Yahoo Finance, Cheddar, and Bloomberg. Short Bio R “Ray” Wang (pronounced WAHNG) is the Founder, Chairman, and Principal Analyst of Silicon Valley-based Constellation Research Inc. He…...

Read more

Holger Mueller is VP and Principal Analyst for Constellation Research for the fundamental enablers of the cloud, IaaS, PaaS and next generation Applications, with forays up the tech stack into BigData and Analytics, HR Tech, and sometimes SaaS. Holger provides strategy and counsel to key clients, including Chief Information Officers, Chief Technology Officers, Chief Product Officers, Chief HR Officers, investment analysts, venture capitalists, sell-side firms, and technology buyers. Coverage Areas: Future of Work Tech Optimization & Innovation Background: Before joining Constellation Research, Mueller was VP of Products for NorthgateArinso, a KKR company. There, he led the transformation of products to the cloud and laid the foundation for new Business Process as a…...

Read more

Steve Wilson is former VP and Principal Analyst at Constellation Research, leading the business theme Digital Safety and Privacy. His coverage includes digital identity, data protection, data privacy, cryptography, and trust. His advisory services to CIOs, CISOs, CPOs and IT architects include identity product strategy, security practice benchmarking, Privacy by Design (PbD), privacy engineering and Privacy [or Data Protection] Impact Assessments (PIA, DPIA). Coverage Areas: - Identity management, frameworks & governance- Digital identity technologies- Privacy by Design - Big Data; “Big Privacy”- Identity & privacy innovation Previous experience: Wilson has worked in ICT innovation, research, development and analysis for over 25 years. With double…...

Read more

Chirag Mehta is Vice President and Principal Analyst focusing on cybersecurity, next-gen application development, and product-led growth. With over 25 years of experience, he has built, shipped, marketed, and sold successful enterprise SaaS products and solutions across startups, mid-size, and large companies. As a product leader overseeing engineering, product management, and design, he has consistently driven revenue growth and product innovation. He also held key leadership roles in product marketing, corporate strategy, ecosystem partnerships, and business development, leveraging his expertise to make a significant impact on various aspects of product success. His holistic research approach on cybersecurity is grounded in the reality that as sophisticated AI-led attacks become…...

Read more

Martin Schneider has had a unique career that has spanned both analyst and marketing practitioner roles, focused on high technology and related industries. The unifying factor has always been both a keen analysis of go-to-market trends, while also having achieved success as a marketing leader. Schneider started his career as a journalist covering B2B technologies, and quickly transitioned into a leading analyst covering application software for the 451 Group in NYC, where he specialized in CRM, marketing automation, and business intelligence/analytics technologies. After analyzing various go-to-market strategies of dozens of technology vendors, Schneider made the move to the vendor side, where he led successful go-to-market teams for several startups and established tech providers,…...

Read more

In many ways, the themes that dominated 2024 were a continuation of the generative AI revolution started in 2023. And then the switch flipped from generative AI to agentic AI and CxOs started to focus on returns and production deployments.

So long proofs of concept and hello returns on investment. This more practical AI spin featured familiar players--Nvidia, Microsoft, Amazon Web Services and Google Cloud--with rejuvenated giants such as Salesforce and emerging vendors including Anthropic, Rubrik and Kong.

The technology vendors in this year's Enterprise Awards have shown the ability to navigate an enterprise technology landscape that changes every few months. The Constellation Research team debated, horse traded and bickered to pick this year's 2024 Constellation Enterprise Award Winners. Enjoy.

BEST ENTERPRISE SOFTWARE VENDOR

This category recognizes the enterprise software vendor who improved their customer relevance, market share, customer satisfaction, and brand standing.

co-Winner: Google

Why did they win?

A few days ago, it was not clear if Google would be a contender here, but the launch of Gemini 2.0 (and more) makes it a winner. Here’s why.

- Google had a lead in custom algorithms on custom silicon (TensorFlow on TPUs) and started in 2014. Now with Trillium, Google has maintained its lead over its fellow cloud competitors. Google is on its 6th iteration of custom AI silicon and the competition is on its second.

- Multimodal lead. Humans are inherently multimodal and for AI to have a shot to be general AI it needs to be multimodal. Google was the first with Gemini at Google Cloud Next, now it is pushing further with native Gemini Flash 2.0, which uses Trillium as its platform. It is the first multimodal model that doesn’t have to call on other models to be multimodal. All modalities are trained together.

- Just when we got comfortable with agentic AI, Google has pushed on into autonomous AI. Its coding AI agent Jules identifies what code to write, bug to fix (in JavaScript and Python) and can put it on GitHub. Google is making software development autonomous and moving into the era of Autonomous Software Operations (where software writes itself, delivers and operates itself - more here.)

- Google shows a broader leverage of its models which creates 2+2=5 synergies: Project Astra uses Gemini 2.0, has a 10-minute memory window and can use Google Search. Project Mariner also uses Gemini 2.0 in the Chrome browser. Collab provides automatic insights from data in notebooks with language discovery with Gemini 2.0. Finally, Google is going vertical (already) with research and gaming offerings.

CO-WINNER: SALESFORCE

![]()

For the longest time Salesforce seemed to be stuck on its 20+ year old architecture. In 2022 at Dreamforce, Salesforce departed from that architecture with the launch of Genie (now Data.com). That innovation has put Salesforce on a new, innovative platform trajectory.

Fast forward to Dreamforce 2024 and Salesforce has achieved four unique feats that make them the winner of the 2024 best enterprise software vendor award:

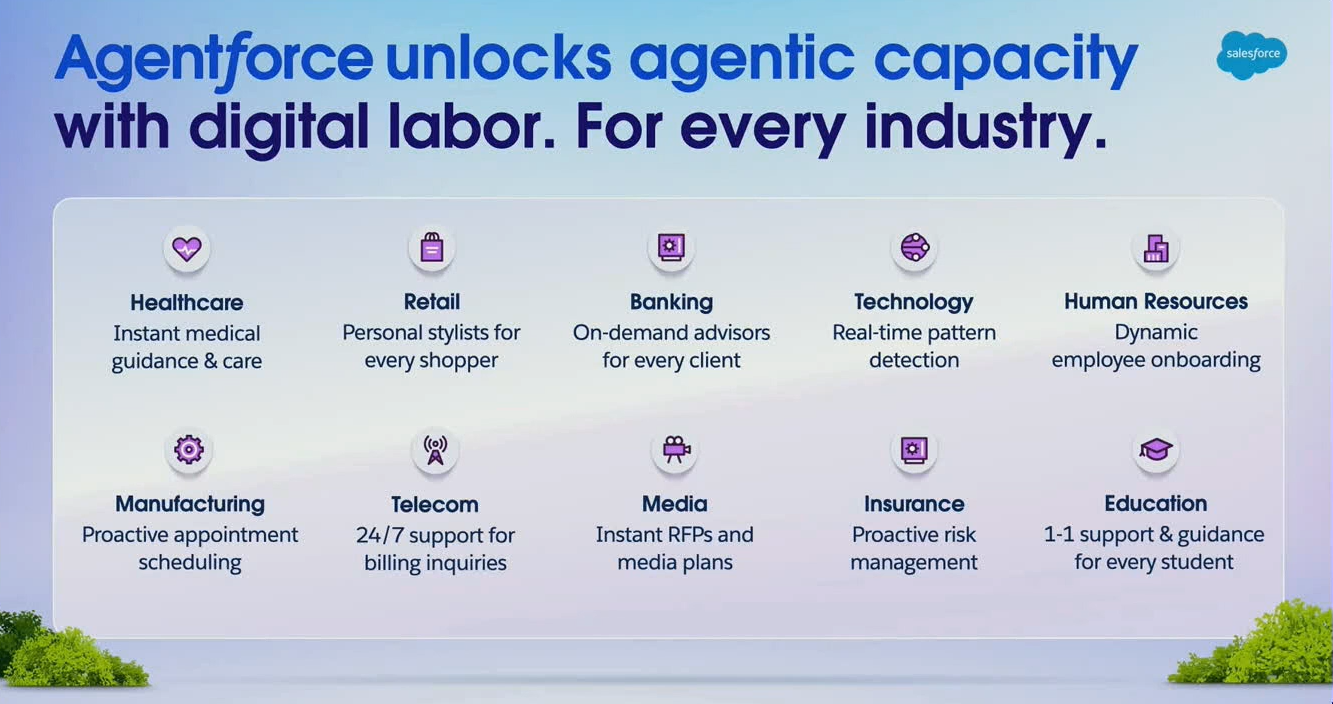

- Salesforce was among the first vendors to unleash an agent-based offering with Agentforce, thus ushering the era of agentic AI, not in PowerPoint, but in actual available (and paid for) enterprise software.

- Salesforce showed continuous and systematic platform building from the launch of Genie to Einstein to Einstein Copilot and now Agentforce. No other software vendor has a 2+ year platform evolution strategy to serve the enterprise like Salesforce.

- Salesforce was the first enterprise vendor to access the data that matters for enterprises--transactional data--via its Atlas Reasoning Engine. Until Atlas, generative AI was limited to the transformer algorithm-based document centric ingestion and generation. That approach is of course transformative, but enterprises run on data and transactions and Salesforce is the first enterprise vendor to unleash GenAI to both data sets.

- Enterprise vendors typically announce their plans at their user conferences and deliver capabilities months later. But Salesforce at Dreamforce 2024 pre-equipped 1,000 customers with Agentforce and had company attendees build agents during Dreamforce. The expectation was one agent per customer, but attendees were so inspired they ended up building 10 agents per customer on average. That proof point highlights how easy Salesforce has enabled the creation and operation of agents.

Congrats to Salesforce, which has shown that we are in the PaaS age and not the DIY era of AI in the enterprise.

RUNNERS UP: ServiceNow

Why were they recognized?

Call ServiceNow an AI platform, an automation and workflow platform or call them a platform of platforms. ServiceNow spent 2024 working to corner the market of putting AI to action and work. From its Workflow Data Fabric to over 150 GenAI applications across its Now Platform, ServiceNow got specific with upgrades to processes with a healthy dose of GenAI governance. On the functional front, ServiceNow focused on partnerships with key functional solutions to bring data and workflows out of functional silos, announcing major initiatives with contact center solutions like Genesys and Five9. ServiceNow CEO Bill McDermott has also issued a promise for business: ServiceNow is here to make business fun again. After years of pushing data, workflow and AI rocks up chaotic hills, businesses are ready for some of that fun.

RUNNERS UP: ANTHROPIC

Why were they recognized?

Anthropic had a strong 2024 where it landed $8 billion in funding from Amazon Web Services, put its Claude family of models in the enterprise winner's circle. But more importantly, Anthropic put collaboration features around its Claude large language models that may point to a future application suite. Anthropic CEO Dario Amodei is putting Anthropic in the middle of enterprise AI conversations in 2025.

BEST CEO

This category recognizes the best enterprise CEO. Enough said.

WINNER: JENSEN HUANG, NVIDIA

Why did they win?

If there is one CEO in enterprise tech who has managed a growth curve well, it is Nvidia’s Jensen Huang. Never has a tech vendor managed growth from single digit billions of triple digit billions in such a short time, so successfully. Yes, timing is everything, but if Huang had not seeded Nvidia machines to OpenAI in 2016 it wouldn’t be where it is today.

But credit does not only go to Huang for betting on its own platform, but also for surrounding himself with great talent. Chips can only scale when abundant talent is around: Nvidia’s four company officers have been around since 2003 (longest) to 2017 (shortest). Simply put, Huang hired talent that can scale for the AI era boom.

Working with the same team allowed Huang also to do something that the chip industry has struggled with - growing the supply chain. While Nvidia has recently run into some supply challenges, it has not hurt its growth path. And finally, the semiconductor industry that is accustomed to release major platforms on a two-year cycle, was pushed single handedly into a one-year cycle by Huang. He knows Nvidia will need to more beyond chips and has successfully moved up the technology stack with CUDA and NIMs. An added bonus is Huang is always an insightful, incredibly humble and interesting CEO to see on dozens of tech keynotes.

- Nvidia CEO Jensen Huang has a dream...

- Nvidia's uncanny knack for staying ahead

- Nvidia highlights algorithmic research as it moves to FP4

- Nvidia launches NIM Agent Blueprints aims for more turnkey genAI use cases

- Nvidia shows H200 systems generally available, highlights Blackwell MLPerf results

- Nvidia outlines roadmap including Rubin GPU platform, new Arm-based CPU Vera

RUNNERS UP: MATT GARMAN, AWS

Why were they recognized?

If you attended or watched Amazon Web Services re:Invent 2024 event, you had to come away impressed by the company’s new CEO, Matt Garman. Had this unflappable straight shooter taken the helm of the company earlier in the year, rather than on June 3, 2024, he would have been our hands-down pick for Best CEO of 2024. Good things happened after Garman took charge, starting with the Oracle-AWS partnership, announced on September 9, and culminating in a powerhouse re:Invent that saw AWS solidify its AI roadmap with significant product announcements and introductions. Garman oozes credibility and in-depth knowledge of all things AWS, having joined the company as an MBA intern in 2005 before becoming one of its first product managers in 2006. More importantly, Garman believes in customer choice and makes their wants and needs the top priority, whether best served by AWS or by third-party partners.

RUNNERS UP: BARAK EILAM, NICE

Why were they recognized?

Barak Eilam first joined NICE 25 years ago, taking on the CEO role 10 years ago. In his tenure, total revenue has tripled, and profitability has increased 4x and market value has increased 7x for the now $14 billion dollar contact center company. Through his leadership, NICE is a consistently recognized leader in Contact Center as a Service (CCaaS) and is poised to look beyond the contact center function and into a more expansive service-led customer engagement platform with a solid underpinning of AI. He is also a good person with conviction, humility and a distinct need to help people around him. His upcoming “retirement” will likely see him spearheading both philanthropic and entrepreneurial endeavors.

BEST ENTERPRISE SERVICES VENDOR

This category recognizes the enterprise services vendor that transforms delivery models and crafts new client–centric market approaches.

WINNER: ACCENTURE

Why did they win?

The services market has been brutal with the major players growing in the mid-single digits. Despite no promotions or advancement for employees in this current cycle, Accenture has weathered the AI storm quite well. While other services firms were talking about AI, Accenture took every opportunity to engage clients with live POC’s and demos to help clients quickly adopt to the changing landscape. Accenture has achieved more than $1 billion in AI associated revenue, and that 10X growth from $100 million just last year is quite impressive. The loss of Global CTO Paul Daugherty in September to retirement will be felt by clients for years to come, but the shift to AI will forever change the services landscape. Accenture has taken a first mover advantage and competitors and customers have taken note.

RUNNERS UP: PERSISTENT SYSTEMS

Why were they recognized?

Prior to Sandeep Kalra’s arrival, Persistent had been stagnant in growth at $500 million in revenue, but under Kalra’s leadership, the company grew and crossed the $1 billion mark in 2023. Over the past four years, Persistent has transformed from a specialized technology provider into a trusted digital transformation partner and global brand competing against the Tier 1 global system integrators. In October 2024, the company achieved a $345.5 million quarter, showing an 18.4% YoY growth. Persistent is making a name for itself in BFSI, healthcare, and high tech and emerging industries.

BEST ENTERPRISE SOFTWARE STARTUP

This category recognizes when an enterprise software startup achieves escape velocity in mind share and relevance.

WINNER: WIZ

Why did they win?

Wiz has demonstrated exceptional growth, achieving $500 million in ARR and is aiming for $1 billion ARR by 2025. This trajectory underscores its significant impact in the cloud security sector. In July 2024, Wiz declined a $23 billion acquisition offer from Google, opting to pursue its own path toward an IPO. This decision reflects Wiz’s confidence in its long-term potential, strategy, and commitment to innovation. Wiz has also expanded its capabilities through acquisitions, such as the recent purchase of Gem Security. Wiz is not just executing as the best start-up; it’s executing as one of the best enterprise software companies of any size.

RUNNERS UP: KONG

Why were they recognized?

Kong, a startup focused on cloud API technologies, raised $175 million Series E financing at a valuation of $2 billion. It remains to be seen if Kong can thrive in the cloud API ecosystem. Certainly, demand is there. Kong is looking to capitalize on a surge in API call demand largely due to cloud connections to large language models.

BEST AI LAUNCH

Adobe launched significant upgrades, updates and new models and integrations across its applications and platform in 2024. Simply put: Adobe didn’t have an AI launch, but rather multiple AI solution launches coupled with highly usable and creative and productivity enhancing AI tools. These tools were then launched directly into existing interfaces and applications used by creative, business and marketing users. While the most notable and visible were introductions of upgrades to the Adobe Firefly Family of Models—specifically Image, Vector, Design and Video—Adobe also launched AI services across its Digital Experience (AI Assistant in Adobe Experience Platform, personalization in Journey Optimizer, content analytics and behavior analytics in Adobe Analytics, GenAI enhancements to create personalized content across Adobe Experience Manager) and Document Cloud (Acrobat AI Assistant includes multiple AI and GenAI driven services).

While the individual AI products or services are impressive on their own, it is the totality of AI being infused directly into Adobe’s portfolio of creative and business applications and across their engagement-centric Adobe Experience Platform that matters. The proof of AI’s value to Adobe was revealed in Q4 and 2024 earnings with CEO Shantanu Narayan noting that the company attributes more than $2 billion in Digital Media (which represents the Creative Cloud and Document Cloud business groups) net new ARR. Bottom line: customers are USING AI, not just testing or experimenting. Customers have initiated over 16 billion Firefly powered generations, with new records being set every month.

Specific to a new 2024 AI launch, the Adobe Acrobat AI Assistant saw AI Assistant conversations double quarter-over-quarter. The AI launches in 2024 have kicked off headwinds for all three major business groups moving into 2025, but customers in multiple segments are tapping into the company’s generative AI tools across Adobe’s portfolio.

RUNNERS UP: SALESFORCE AGENTFORCE

Why were they recognized?

Salesforce’s entire Dreamforce event could have just been called Agentforce. The company put on a full court press around its agentic AI play and touted more than 2,000 AI agents created during the event. But more than a no code platform for building agents, Agentforce is including several out of the box AI agents as part of the launch. Highlights were their AI sales development rep, which enabled business development teams to instantly become global, 24-7 lead development engines. Another solid agent was their sales coaching agent, which provides in-line and contextual coaching to sales reps. Salesforce now has several pre-built agents, covering sales, service and marketing campaign building use cases.

RUNNERS UP: MAJOR LLM PROVIDERS

Why were they recognized?

The LLM race used to be more about genAI, which is used to generate things like text, chats, images, video, etc. But they are moving to the next level from seamless multi-modality such as the ability to digest input in NLP, text, image, video, etc., and provide output back in the needed format. Also, expanding the language usage from just English to the most common languages.

Each has its own variation to make this a winner. Meta’s Llama models proved that open source models can compete toe-to-toe against the big boys. OpenAI continues to innovate at a fast pace keeping everyone on their toes. Google is bringing the multi-modality, governance, and trustworthiness to the forefront. Anthropic is making things a lot better and cheaper. So many things that happened so fast.

And LLM vendors can command a premium. OpenAI recently announced the price hike from $20/user/month to $200/user/month.

Overall, generative AI has come a long way in 2024 alone. It is enterprise-ready in many ways. AI is moving from the experimentation state to the production stage.

BEST PARTNERSHIP

This category recognizes the enterprise partnership that delivered the most impact for customers and the market.

WINNER: AWS & ORACLE

Why did they win?

Moving past years of competitive sniping, Oracle and Amazon Web Services forged a pragmatic partnership that’s an overdue acknowledgement of customer requirements. The deal made the leading enterprise-grade database services (Oracle Autonomous Database and the Oracle Exadata Database Service) and the leading open-source database (MySQL/MySQL Heatwave) available with the blessings of both companies (as well as clear licensing terms and support arrangements) on the most popular public cloud. It’s unclear whether the CEO change at AWS or whether the influence of one or more mega customers finally made this partnership possible, but it’s good for all customers, as they are now able to leverage their substantial investments in Oracle tech while still running everything else on their preferred cloud platform.

- Oracle Database@AWS hits limited preview

- Oracle CTO Ellison talks about AWS partnership with Garman, the need for autonomous security

- Oracle's cloud, AI plans are a master class in co-opetition

RUNNERS UP: Servicenow & five9

Why were they recognized?

While still in early days, ServiceNow’s partnership with Five9 is about a massive future opportunity for customers looking to connect more dots between platforms, data, experiences and people. Announced in November and expected to be available in early 2025, this partnership drives well beyond APIs or marketplaces with a turnkey AI-powered solution for unified end-to-end employee and customer experiences. The unified offering will pluck the best of both worlds to offer a single, integrated capability living in a user’s platform of choice. Five9’s TranscriptStream will integrate into ServiceNow’s Interaction Management and into the Now platform. ServiceNow has established multiple functional partnerships, and in earnest, the Five9 partnership expansion is just the latest with others, most notably with Genesys, paving the way. Expect to see this functional expansion continue into 2025.

BEST TECH ACQUISITION

This category recognizes the enterprise tech acquisition that has the most impact for customers, market landscape, and the overall industry direction.

WINNER: SAP + WALKME

Why did they win?

Is software valuable if nobody actually uses it? Are AI Agents worth the effort if nobody ever contributes or leverages them? It was clear from the very first words of SAP CEO Christian Klein Sapphire keynote, use and adoption matter more now than ever. That approach is what makes the acquisition of Digital Adoption Platform darling, WalkMe, interesting. As SAP works to guide workflows across applications, the vision here is for WalkMe to become SAP’s window into adoption and the pace and advancement of business transformation goals.

RUNNERS UP: HPE + JUNIPER

Why were they recognized?

HPE announced the purchase of Juniper Networks for $14 billion in a move that would give it a unified AI stack. That deal is now expected to close in early 2025. HPE CEO Antonio Neri touted the benefits of the deal in December. "Both HPE and Juniper continue to believe the transaction will enable us to provide a complete portfolio of modern, secure networking solutions that offer essential foundations for both Hybrid Cloud and AI," he said. "This transaction will also strengthen U.S. National Security interests by advancing HPE's position as a strong U.S. Innovator among global technology companies."

RUNNERS UP: COHesity + veritas

Why were they recognized?

With the acquisition Veritas closing, Cohesity becomes the fastest company to cross $1.5 billion revenue, "Rule of 40", in just 11 years since their founding - and on a path to $2 billion revenue goal soon. With more than 12,000 customers, the combined company will have more than 85% of the Fortune 100, 70% of the Global 500, the broadest portfolio in the industry and 2x the engineering resources compared to others. Nvidia has also invested in Cohesity.

WORST TECH ACQUISITION

This category recognizes the enterprise tech acquisition that had the least impact for customers, market landscape, and the overall industry direction.

WINNER: ALPHABET AND ANYBODY

Why did they win?

There are only so many times companies can say no to your offers until you wonder, “Was it me?” In the case of Alphabet and their track record of potential mergers and acquisitions in 2024, two power players in two different markets said no at two very different stages of the relationship. Both left egg on the face of a company better known for its business bravado than its acquisition humility.

In fairness to Alphabet and the Google brand, the Hubspot “deal” was more of a rumor. Hubspot could have been another tale of woe in the long history of ‘Google struggles with business applications, but the two parties wisely agreed to part as friends. Wiz similarly declined to push the proposed deal to any substantive stage, publicly choosing to bet on themselves which helped cement their “Best Startup for 2024” status. All in all, Alphabet knocked on a lot of acquisition doors to expand its footing, increase workloads in cloud and secure new lines of revenue to no avail.

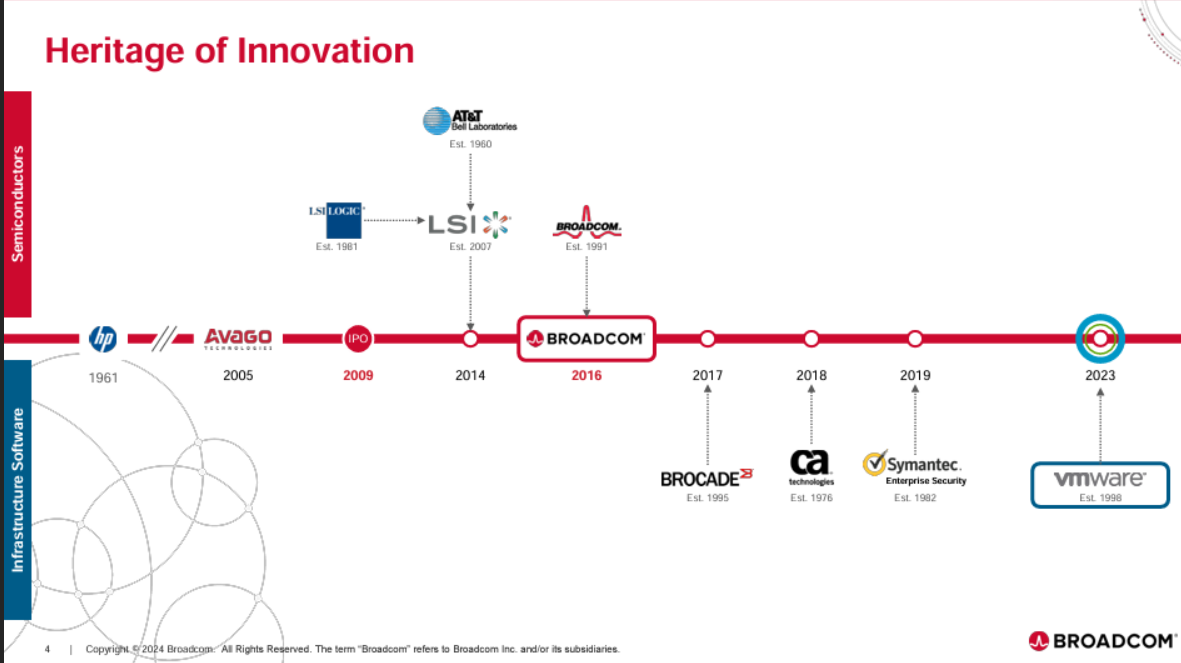

RUNNERS UP: Broadcom + vmware

Why were they recognized?

Broadcom's purchase of VMware looked swell in PowerPoint. Broadcom would broaden its revenue base in software, simplify and raise prices and keep an installed base. Unfortunately, VMware customers were irked and the competition is swirling. Nutanix is likely the biggest beneficiary of VMware angst, but how those workloads get moved will be a trend to watch in 2025. Broadcom has turned the VMware deal into a huge financial success, but what’s in it remains to be seen what’s in it for customers.

BEST NEW IPO

This category recognizes the most successful IPO for the year

WINNER: Reddit

Why did they win?

When Reddit went public in 2024, it wasn't hard to find skeptics. In its short life as a public company, Reddit has proved naysayers wrong as the social network has leveraged content provided by real humans for the AI age. In its third quarter, Reddit delivered $29.9 million in profit and revenue of $348.4 million, up 68% from a year ago. Daily active users on Reddit were 97.2 million, up 47% from a year ago. Fourth quarter revenue is projected to be in the range of $385 million to $400 million. Reddit has forged partnerships with OpenAI, Google and is providing training data to models.

Next up: Reddit is aiming to improve its search experience and CEO Steve Huffman said: "We know many users are looking for more than just answers; they are looking for authentic, real-world insights and advice from the communities on Reddit."

RUNNERS UP: rubrik

Why were they recognized?

Rubrik, a data management and cybersecurity company, went public in April at $32 a share and now has more than doubled. However, the company traded below its IPO price after rocky earnings before the big rebound. Rubrik's offerings are resonating with larger enterprises, and the company has surpassed $1 billion in subscription annual recurring revenue, up 38% in the third quarter compared to a year ago. Rubrik's third quarter revenue was $236.2 million, up 43% from a year ago. Yes, Rubrik is still posting losses, but partnerships with AWS, Pure Storage and Okta signal more enterprise traction ahead.

BEST NEW ENTERPRISE CATEGORY

This category recognizes the best new enterprise category that made an impact to the market.

WINNER: agentic ai

Why did it win?

If there was one new technology concept that commandeered both the tech media but also most company roadmaps it would have to be agentic AI. While generative AI owned the cycles in 2023; 2024 quickly became the burgeoning age of autonomous agents. When Salesforce, Oracle, ServiceNow, SAP and Microsoft are stumbling over to scoop each other’s agentic AI announcements, you know it’s a big deal. Nearly every major player in software made some announcement around agentic AI, and those that failed to do so are seen as lagging.

What made agentic AI the hottest new category? Arguably the fact that this is one of the most quickly deployed new technologies both in terms of being embedded in key software portfolios but also being used by enterprise organizations. Also, users have been building both muscle memory and comfort levels with all the generative AI “copilot” announcements and releases over the past two years, so agentic AI was a smooth and natural evolution. These new autonomous agents have been delivered with no code tool sets to speed their uptake, and the results speak for themselves, with companies like Salesforce touting more than 2500 deployed agents to date.

And why is agentic AI a category and not a feature set of AI? Because it changes the game and has implications across every facet of tech. The goal of AI is to aid in decision-making, and optimizing the moments where humans need to make decisions and reducing the number of unnecessary human actions and decisions in any given workflow. That means agentic AI will become prevalent across not just the use of technology, but also the building, testing, configuring, managing and distribution of technology. It will, in short, be an inevitable part of our daily lives across work and personal activities. No other technology has had this large of an impact, this quickly, since the public internet itself.

RUNNERS UP: decision intelligence

Why was it recognized?

Decision Intelligence or Decision Automation is the natural extension of why we have AI. The goal is to achieve decision velocity inside an organization to gain efficiencies and accelerate business. Look for this theme to emerge in 2025 and beyond.

BEST NEW ENTERPRISE SOFTWARE MARKETING OF THE YEAR

This category showcases the best marketing campaign, ad, or perception transformation in the enterprise.

WINNER: atlassian

Why did they win?

Atlassian takes the top spot for bringing a unified marketing message of building better systems of work FOR work. For some time now, Atlassian has struggled to pull some of its acquisitions into a cohesive marketing message for a more cohesive value proposition. 2024 is the year it all clicked, some would say thanks to an advanced AI strategy that pulls functional tools into a more intentional and integrated system of work. Atlassian has brought purposeful marketing language around collaboration and work.

RUNNERS UP: salesforce agentforce

Why were they recognized?

It takes a bold marketing strategy to pivot from a go-to-market live event motion to one that positions another vendor’s copilots as a failure with a new solution where customers can build immediately. It takes a bold strategy…or an even bolder CEO willing to take on the world. When Marc Benioff hit the Dreamforce stage in 2024, the marketing machine had already kicked into high gear with a heavy dose of paid, earned and owned media all screaming the same message: Agentforce had arrived. Salesforce clearly listened to past criticism that noted the scales far more tipped towards long-lead aspirational products as opposed to usable, buildable solutions ready to deploy the moment the keynote concluded. Agents were being built in the campgrounds and customers could get started even before the traditional Hawaiian blessing had been delivered. This excitement and momentum took to the road with a whistle stop tour and a steady drum beat of use case reveals and customer testimonials, allowing Salesforce’s most powerful marketing weapon (aka their Trailblazers) to tell the tale of their own improvements thanks to Agentforce.

BEST NEW ENTERPRISE SOFTWARE AD CAMPAIGN

This category showcases the best ad campaign in the enterprise.

WINNER: jira

Why did they win?

Jira’s ad campaign featuring Zach Woods, an actor known for roles in The Office and Silicon Valley, hit all the notes a video spot should hit, especially the note of insider joke humor. Woods, looking to collaborate on a contract ideal for his “aspiring to be a rich person” agenda and his goals to be on “a sake only diet” of the rich and famous, Woods perfectly highlights why work and how we collaborate for business has changed for the better thanks to workflows, data and AI.

RUNNERS UP: Stych billboards

Why were they recognized?

Stych went back to the whiteboard to create a campaign that would appeal to developers and create bottoms-up influence. The company chose not to go with a typical enterprisey billboards such as “we understand your security” but rather emotionally appealed to developers by showing a play on code or on a technical term. They picked San Francisco to show their ads including some prominent places such as near Moscone during the RSA Conference.

BEST LIVE-EVENT

This category showcases the team that adapted and succeeded in their high-touch in-person event to a full on virtual event experience.

WINNER: google cloud next

Why did they win?

In eight years, from a few hundred attendees at a nondescript location in San Francisco to 30,000+ attendees in one of the largest convention centers in Las Vegas, the Google Cloud Next conference came a long way. And so did Google Cloud. Google Cloud has increased its revenue 5x in the last five years. Google Cloud Next is the moment for the company to share the progress it has made on AI and other fast-growing categories such as cybersecurity. It was a flawless event that left a mark; Google Cloud appeared as enterprisey as Microsoft or AWS.

RUNNERS UP: aws reinvent

Why were they recognized?

The traditional get together of the IT industry used to be VMworld that would be attended by non-VMWare users because all of the CIOs and IT senior leaders were there. AWS took that baton pre-Covid already with 80,000 attendees. Now AWS re:Invent has come back to that position with 60,000 attendees and attractive new services and offerings.

RUNNERS UP: hpe discover

Why were they recognized?

HPE Discover 2024 marked the first-ever live tech keynote in The Sphere in Las Vegas. Clad in his black jacket, Nvidia CEO Jensen Huang joined HPE CEO Antoni Neri and officially declared “Antoni consumed more liquid than anyone known to mankind.” Of course, he was talking about HPE data centers now being liquid-cooled, which was one of the major announcements of the event. HPE also announced its plan to capture the AI market by offering the simplistic “AI OOB,” an out-of-the-box offering of AI models and other optimized components that come ready to deploy. HPE could kill it in the inferencing arena if this concept takes off. HPE also announced Zerto support for KVM. Given the Broadcom/VMware fiasco, HPE could become a landing place for a lot of dissatisfied customers.

BIGGEST TECH FLOP OF THE YEAR

This category simultaneously recognizes the highest potential and largest failure in enterprise tech.

WINNER: apple vision pro

Why did they win?

This late arrival to the already-failed Metaverse market was not only overweight (at more than 20 ounces), and overpriced (at $3,499), it suffered from a short battery life (of only 2 hours) and a paltry selection of augmented reality and mixed reality content. Reports are that Apple will end production of the device in 2024 because it can’t unload the 500,000 to 600,000 units already produced. The simple truth is that the metaverse has failed to gain mass adoption because the vast majority of people don’t want to cut themselves off from reality and other people — all while looking like a dork with a contraption on their heads. If you really want to escape into the Metaverse, you can buy Meta’s MetaQuest 3S for just $299. The Apple Vision Pro is a repeat performance for Apple, having arrived late to the smart speaker category in 2017 with its overpriced Apple HomePod — although at least that product is still selling to Apple fans.

RUNNERS UP: DOE FAFSA Rollout

Why were they recognized?

The Department of Education’s new financial aid system and FAFSA form will be seen as 2024’s worst IT projects. The FAFSA form was revamped with a Dec. 31 soft launch (typically FAFSA opened in October) that barely delivered. Not only was the FAFSA form a headache for parents and students, but it was also an IT disaster. Studentaid.gov couldn’t serve students well. You mean the Department of Education lacks cloud scalability? Pretty much. Along with the FAFSA form changes, the Department of Education launched its new hybrid cloud platform. A June General Accountability Office report highlighted issues with the new systems. In 2021, the Federal Student Aid (FSA) org aimed to modernize and replace a 30-year-old system to process student aid applications. In March 2023, FSA put a new system in a new cloud environment. In December, that system was fully deployed. The system stabilized but was also late for launch for the 2025-2026 school year.

Data to Decisions Digital Safety, Privacy & Cybersecurity Future of Work Marketing Transformation Matrix Commerce New C-Suite Next-Generation Customer Experience Tech Optimization Chief Analytics Officer Chief Customer Officer Chief Data Officer Chief Digital Officer Chief Executive Officer Chief Financial Officer Chief Information Officer Chief Information Security Officer Chief Marketing Officer Chief People Officer Chief Privacy Officer Chief Procurement Officer Chief Revenue Officer Chief Supply Chain Officer Chief Sustainability Officer Chief Technology Officer