Capgemini continues the journey to becoming the innovation company

Capgemini continues the journey to becoming the innovation company

Guy Courtin was formerly Vice President and Principal Analyst at Constellation Research covering Matrix Commerce and how the Internet of Things drives the evolution of commerce. Guy has over 15 years experience in the technology space and specifically in the supply chain space. Most recently he was the Vice President of Research at SCM World. Where he focused on the service providers that empowered supply chains. Prior to SCM World, Guy held numerous senior positions. He was responsible for product marketing at RSi, a retail supply chain solution provider. There managed RSi’s go to market strategy around their leading cloud based supply chain solutions. He also spear headed Progress Software’s supply chain group. Where he was responsible for driving revenue and market share as well…...

Read moreTwo weeks ago I was on the road again…I know I know…. what a surprise! I can’t complain since I was home, Paris France, where Capgemini was hosting their summer analyst day at their fabulous training center (see picture). While the setting at Les Fontaine captured the tradition and history of France, the discussions with Capgemini were dominated by the theme around innovation and how Capgemini is working with leading firms across a variety of industries to infuse innovation into their every day DNA.

Not a bad place for a 2 day meeting.

Capgemini is correct in focusing on how the digital revolution we are undergoing, will have a wide and deep impact on industries. While there were a number of examples from all the businesses they work with, the ones that caught my attention were, no surprise, around supply chain.

- Capgemini and large European retailer discussed their thinking around an important customer centric project. At the base of this project is the need to implement a large and comprehensive CRM system. Speaking with an executive from the retailer, it was evident that they recognize the importance to create a 360-degree view of their customers. The goal being to nurture the customer experience, constantly and continually. The notion of a sequential relationship – customer has a need, customer seeks solution, customer buys product and transaction is consummated – is no longer how the retail/consumer relationship works. The retailer has identified the need to be much savvier when it comes to their consumers’ data. As they work through the technological needs, it was clear in my discussions that they are exploring new and powerful ways of leveraging the information they expect to extract from their CRM solution to better service their customers, which is really about providing an enhanced retailing experience.

- Speaking with some of the Capgemini executives it was clear that they regard supply chain improvements as holding great opportunity. The thinking focuses on how digital is disrupting the entire supply chain, and the opportunity to target the parts that are “hidden” from the general public. Of course this is music to my ears. A wonderful example of this in action is the work Capgemini is doing with Nokia and their world class supply chain. The Finnish telecom giant has looked to Capgemini to overhaul their production and sourcing processes – to harmonize the supply chain. The work is not simply about buying a new software solution, but rather about identifying the business processes that must change and some that need to be adopted. Not a small task. But the work Capgemini is accomplishing at this level with Nokia could and should lead to more transformative projects within their supply chain – leveraging the digital transformation for future business cases.

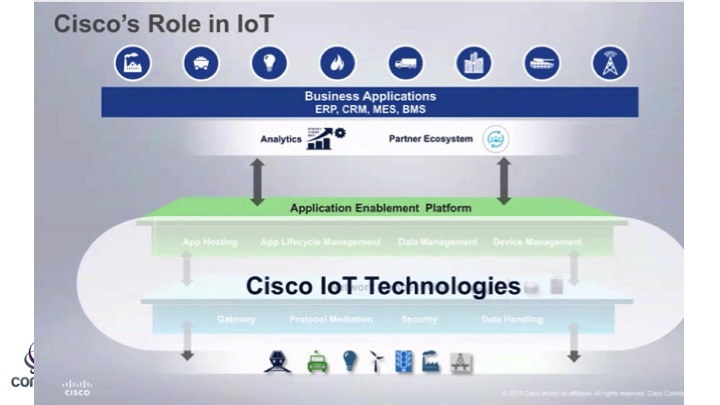

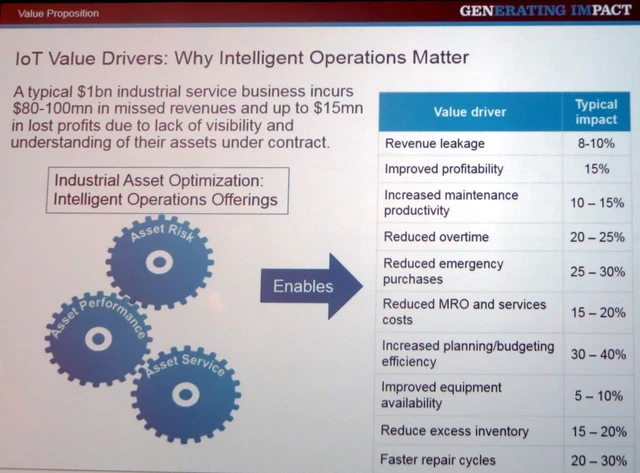

- The Internet of Things (IoT) and the impact it has with manufacturing. Digital manufacturing within such areas as the automotive industry was highlighted as well. Speaking with the Capgemini heads of the automotive sector, the discussion revolved around the base line use cases many companies are using IoT for: asset management, predictive maintenance and field enablement. However in my discussions around this topic we began to explore the possibility of new use cases emerging from IoT. Around greater customer experience, enhanced store utilization and new business models between manufacturer and customer. Some of which may never see the light or day, but Capgemini is clearly thinking about disruptive this technology will truly become. More importantly, Capgemini is partnering with their customer base about how to take advantage of IoT.

Following up from my meetings with Capgemini this March in Chicago, the digital disruptive theme continues to be a vital theme to what Capgemini is executing on with their customers. Their ability to continue to help their customers innovate around digital, will determine how successful Capgemini is in becoming a leading services firm in this space. Companies, from all industries, will need these types of partners as their industries become transformed and disrupted by digital changes.

We are all witness to the transformation every day – for example while in Paris with Capgemini we were subject to a strike by an traditional business, taxi drivers, against a digital disruptor Uber. We are all seeing and thinking about how each industry will be impacted by this change, companies like Capgemini are working on a valuable services partner to help navigate the journey. ![]()