Vice President and Principal Analyst

Constellation Research

Holger Mueller is VP and Principal Analyst for Constellation Research for the fundamental enablers of the cloud, IaaS, PaaS and next generation Applications, with forays up the tech stack into BigData and Analytics, HR Tech, and sometimes SaaS. Holger provides strategy and counsel to key clients, including Chief Information Officers, Chief Technology Officers, Chief Product Officers, Chief HR Officers, investment analysts, venture capitalists, sell-side firms, and technology buyers.

Coverage Areas:

Future of Work

Tech Optimization & Innovation

Background:

Before joining Constellation Research, Mueller was VP of Products for NorthgateArinso, a KKR company. There, he led the transformation of products to the cloud and laid the foundation for new Business Process as a…...

The following video is an interview between Holger Mueller, Constellation VP & Principal Analyst, and Gerald Venzl, Distinguished Product Manager at Oracle, on the new API for MongoDB.

On

CR Conversations

<iframe src="https://player.vimeo.com/video/675424745?h=79390c4f2a&badge=0&autopause=0&player_id=0&app_id=75194" width="1280" height="720" frameborder="0" allow="autoplay; fullscreen; picture-in-picture" allowfullscreen title="CR Interviews Gerald Venzl, Oracle on the new API for MongoDBInterview"></iframe>

Former Vice President and Principal Analyst

Constellation Research

Doug Henschen is former Vice President and Principal Analyst where he focused on data-driven decision making. Henschen’s Data-to-Decisions research examines how organizations employ data analysis to reimagine their business models and gain a deeper understanding of their customers. Henschen's research acknowledges the fact that innovative applications of data analysis requires a multi-disciplinary approach starting with information and orchestration technologies, continuing through business intelligence, data-visualization, and analytics, and moving into NoSQL and big-data analysis, third-party data enrichment, and decision-management technologies.

Insight-driven business models are of interest to the entire C-suite, but most particularly chief executive officers, chief digital officers,…...

Sanjeev Mohan, Principal @ SanjMo; Tony Baer, Principal @ dbinsight; Carl Olofson, Research VP @ IDC; Dave Menninger, SVP & Research Director @ Ventana Research; Brad Shimmin, Chief Analyst, AI platforms, Analytics and Data Management @ Omdia; Doug Henschen, VP & Principal Analyst @ Constellation Research, all sit down with Siliconangle Media's Dave Vellante for a CUBE Conversation around Analyst Predictions 2022: The Future of Data Management.

Vice President and Principal Analyst

Constellation Research

About Andy Thurai

Andy Thurai is an accomplished IT executive, strategist, advisor, enterprise architect and evangelist with more than 25 years of experience in executive, technical, and architectural leadership positions at companies such as IBM, Intel, BMC, Nortel, and Oracle. Andy has written more than 100 articles on emerging technology topics for publications such as Forbes, The New Stack, AI World, VentureBeat, DevOps.com, GigaOm and Wired.

Andy’s fields of interest and expertise include AIOps, ITOps, Observability, Artificial Intelligence, Machine Learning, Cloud, Edge, and other enterprise software. His strength is selling technology to the CxO audience with a value proposition rather than the usual technology sales pitch.

Find more details and samples of Andy’s work on his…...

SoftBank-backed Automation Anywhere, an RPA company, (currently valued over $7B+) recently acquired FortressIQ, a process mining company, for an undisclosed sum. FortressIQ, founded in 2017 by an ex-GenPact (a BPO outsourcing firm) executive, has technology partnerships with Automation Anywhere’s direct competitors – Blue Prism and Microsoft Power Automate.

Why does it matter?

To understand why this is important, you need to understand the Robotic Process Automation (RPA) concept and what is involved in making RPA successful as well. RPA is generally about automating manual work processes by analyzing the inefficiencies, cost, and wastage and improving them by automating them. For any RPA project to be successful, identifying inefficient processes is key. Unearthing the processes to automate, analyzing it, and justifying automation costs to senior management to get approval is a lengthy and expensive process – especially if you bring in outside consulting firms to execute on it. This is where process mining tools come into play. AI-based process mining tools can analyze the data, workflow, and model workflow processes as close to real-life as possible with very little effort.

With the pandemic and work from home (WFH) in full swing, a lot of IT processes have also moved online – whether it is rolling out digital applications or applying for a mortgage loan application, etc. Many enterprises were not ready for this forced digital maturity. Many of them hired as many warm bodies (aka IT consultants) as they can, to solve this problem in the back office by having many humans in the loop to create a “semi-automated” solution. Many enterprises are tired of paying exorbitant rates to those consultants and are now trying to optimize the loop by automating wherever they can. I wrote a couple of reports about emerging trends in SRE and Incident Management recently on how enterprises are trying to cope with this situation (see the further reading section below).

Business process identification and process mining are about learning the unknowns in the process of mapping known business processes.

Where do legacy tools fail

Legacy process mining tools mine data logs from ERP, CRM, BPM (Business Process Management), Invoicing systems, etc. to model a business process workflow. The problem with those tools is that they just identify the processes, and the automation tools can automate it, without removing the inefficiencies in the process flow first. These process mining tools read the logs that are generated by the transactions in a specific process. By combining the logs, over many transactions, these tools can map out the process as it is done today. It can get difficult if the logs are dispersed across many systems for a single process. Unless all of the data is fed properly, the tool might land up creating a partial process map which can result in failure. In addition, the tools also assume all of the processes are done in real-time, and in chronological order. If portions of the process are executed in batch mode, those timestamps can create an improper process map as well.

How Fortress IQ is different

Image Source: FortressIQ.

Fortress IQ takes a slightly different approach to process mining. They deploy a Virtual Process Analyst (VPA) which is a sensor embedded in user desktops to visually record all activities. Later the recordings are analyzed using AI technology. A combination of computer vision, natural language processing (NLP), and Machine Learning (ML) technologies try to understand the process flow and map out the processes. When deployed across multiple desktops, by capturing various analysts doing the same work, the analysis can reveal the differences and potentially unearth the inefficiencies in the process. After filtering out the noise, and side activities, AI can come out with a clear view of the current process and make recommendations for the most optimized process that can be automated using RPA. One of the major issues is redacting sensitive information from the screenshots/processes captured – AI can help in that front as well while making recommendations. Fortress IQ’s DevOps accelerator packs for industry verticals are a good addition for process mining in old-school industries with a closed mindset.

Understanding the current processes and identifying inefficiencies is key to figuring out the optimal process to automate, hence FortressIQ’s motto “understand today, plan for a better tomorrow with process intelligence” makes a lot of sense. Most of the RPA projects fail because they fail to identify the unknowns properly during the process identification which is a very complex work including interviews with process workers, stakeholders, business analysts, and creating process diagrams that may not reflect the true picture with the true hidden nuances.

Current Landscape

The field is getting competitive with many smaller players popping in the market - Celonis, Kryon, MiniT, SmartSense, ProDiscovery, ABBYY, Kofax, PuzzleData to name a few. Though some of these players with unicorn valuations are not that small anymore.

This space has been acquisition galore for the last few years:

In Aug 2019, ABBYY acquired TimelinePI

In Oct 2019, RPA company UIPath acquired Stepshot and ProcessGold

In May 2020, Microsoft acquired Softomotive to be part of Microsoft Power Automate.

In Jul 2020, IBM acquired RPA company WDG Automation

In Jan 2021, SAP acquired gemmal process automation company Signavio

In March 2021, ServiceNow acquired an Indian RPA company Intellibot.io.

In April 2021, IBM acquired process mining software company MyInvenio

In Aug 2021, Salesforce/MuleSoft acquired RPA company Servicetrace

In Aug 2021, Appian acquired process mining software company Lana Labs

In Oct 2021, Microsoft acquired Clear Software

In Oct 2021, process mining software company Celonis acquired Lense.io

Constellation POV

We at constellation think this is a good acquisition by Automation Anywhere to justify businesses’ money spent in RPA by showing the inefficiencies in current processes without spending a lot of money upfront. We also expect M&A to continue and will consolidate the smaller players to join hands with the bigger backer for business expansion and survivability. There is a lot of VC money is flowing into this space in the last few years, obviously, they will expect to get returns sooner than later.

Many RPA projects fail because of poor process identification. In addition, many of the inefficient front and back-office business processes still remain undiscovered as no one thought of it. This is where AI-driven process mining tools such as Fortress IQ can help to identify many processes to automate in a very short period. If you don’t know what is broken, it is hard to fix it.

Recommendation

Given that the announcement just came out, and the fact that Automation Anywhere and Fortress IQ are not fully integrated one needs to exercise caution before going full onboard. It is also worth exploring other tools in the market to figure out how to identify inefficient processes faster, and with all hidden nuances, before engaging in full-blown RPA projects. This will increase the success rate of such projects.

Vice President & Principal Analyst

Constellation Research

About Liz Miller:

Liz Miller is Vice President and Principal Analyst at Constellation, focused on the org-wide team sport known as customer experience. While covering CX as an enterprise strategy, Miller spends time zeroing in on the functional demands of Marketing and Service and the evolving role of the Chief Marketing Officer, the rise of the Chief Experience Officer, the evolution of customer engagement, and the rising requirement for a new security posture that accounts for the threat to brand trust in this age of AI. With over 30 years of marketing experience, Miller offers strategic guidance on the leadership, business transformation, and technology requirements to deliver on today’s CX strategies. She has worked with global marketing organizations to transform everything from…...

Numerous use cases and business imperatives have been outlined for those willing to be the early disruptors shaping the metaverse economy. The truth is many will not have the willpower to be part of this advance party. Much like the early trailblazers in the Age of Digital Innocence or the Age of Digital Giants, those willing to take the leaps and chances will serve as aspirational landmarks on the road into the metaverse.

There are two conversations that today’s Customer Experience (CX) leaders, from marketing to sales to service, need to have: first, what is the metaverse and second, what is our place in the metaverse economy?

In one line, what is the metaverse?It is an infinite domain of shared immersive experiences in which commerce, community and currency co-exist and are co-created. By nature, and by design, the metaverse transcends defined boundaries of “physical” and “digital”. In terms of an experience, the metaverse is where a ride on a stationary bike is a fully immersed and connected experience where riders don’t watch a screen but don goggles to be IN the room with a community. Currency, mined by the power generated by a bike in the physical world, allows riders to tip their instructor and pay for virtual waters for friends.

It could be argued that capacity exists today. But, in the fully realized metaverse, before class starts, riders can stop off at the virtual grocery store, pick up some essentials and before the cooldown of their workout is over, real groceries are delivered to a real front door.

If the metaverse is an ecosystem of shared immersive experiences, what is the role of CX leaders in the metaverse?

“Entry into the metaverse should take a purpose driven and brand led approach. Identify areas where the brand has market permission to introduce, participate, and lead.”

In a world in which a brand needs to be willing to bring 50% of a shared experience to the table, what will the purpose, tone and tenor of that approach be? Will brands let down their guard and co-create in the moment? Or will we wrap the same push-centric communications of web 2.0, delivered through VR goggles?

The difference is the metaverse economy won’t just be about the technologies and platforms required to exist within it. The difference will be the participant’s expectations about experiences within an economy where each individual is shaping and creating economies of value and experience around (and about) themselves. Brands won’t “get a break” when the one-way street of push communications is passed off as an experience. The mere presence of digital content won’t pass as an experience. Just calling something the metaverse won't make it so.

So CX leaders beware. You won’t be able to “campaign your way” through the metaverse. If you want to participate in the metaverse economy, start by asking what purpose your brand has and what value your brand can provide. What will your 50% of any shared experience be?

Vice President & Principal Analyst

Constellation Research

About Liz Miller:

Liz Miller is Vice President and Principal Analyst at Constellation, focused on the org-wide team sport known as customer experience. While covering CX as an enterprise strategy, Miller spends time zeroing in on the functional demands of Marketing and Service and the evolving role of the Chief Marketing Officer, the rise of the Chief Experience Officer, the evolution of customer engagement, and the rising requirement for a new security posture that accounts for the threat to brand trust in this age of AI. With over 30 years of marketing experience, Miller offers strategic guidance on the leadership, business transformation, and technology requirements to deliver on today’s CX strategies. She has worked with global marketing organizations to transform everything from…...

Principal Analyst and Founder

Constellation Research

R “Ray” Wang is the CEO of Silicon Valley-based Constellation Research Inc. He co-hosts DisrupTV, a weekly enterprise tech and leadership webcast that averages 50,000 views per episode and blogs at www.raywang.org. His ground-breaking best-selling book on digital transformation, Disrupting Digital Business, was published by Harvard Business Review Press in 2015. Ray's new book about Digital Giants and the future of business, titled, Everybody Wants to Rule The World was released in July 2021. Wang is well-quoted and frequently interviewed by media outlets such as the Wall Street Journal, Fox Business, CNBC, Yahoo Finance, Cheddar, and Bloomberg.

Short Bio

R “Ray” Wang (pronounced WAHNG) is the Founder, Chairman, and Principal Analyst of Silicon Valley-based Constellation Research Inc. He…...

Is this what a battle line looks like in the metaverse?

Is this a play to dominate and reshape the gaming industry? Is this a play for cloud dominance? Did Microsoft and its CEO known for empathy actually smell blood in the water after headline making employee misconduct charges chased other takers from the table?

No matter how you slice it, the $68.7 billion deal just made the whole metaverse conversation a WHOLE lot more interesting.

First, let’s break down what we know about the deal. Microsoft is set to acquire Activision Blizzard, including mega gaming titles such as Call of Duty, World of Warcraft, Overwatch, Diablo along with mobile and social gaming titles like Candy Crush (before you laugh, it had $1.19 in revenues in 2020 alone) in an all cash deal. Plans are already underway to include many of these blockbuster titles to Microsoft's XBox Game Pass and PC Game Pass. It is worth noting that Activision Blizzard isn’t just a gaming company: it still has a movie production company, eSports league and eSports content network in its portfolio. It also has a TON of workloads in the cloud that gives Azure some new bragging rights against the likes of Google Cloud (who inked a 2020 deal with Activision Blizzard to be the preferred cloud provider and YouTube the exclusive streaming destination).

Let’s just say the rough stuff out loud first: Microsoft struck when the time was right and got one heck of a deal. The rumors, charges and negative press about Activision Blizzard have been swirling for a while. The lawsuit and subsequent investigations have just been the tipping point. Rumor has it there were NO other takers when Activision Blizzard first made the acquisition rounds.

The truth is that Activision Blizzard has been losing loyal long-time players disillusioned with the lack of player-first decision making that Blizzard, specifically, had been known for with the rise of massively multiplayer online games like World of Warcraft. You know you have a problem when your employees (2,000 of them) stage a walk out that prompts thousands of players online to stage a virtual walkout with many of the games top influencers and streamers leaving the game and taking their legions of viewers with them.

The bottom line is that Activision Blizzard’s content portfolio is worth the massive bags-o-billion being rolled into Santa Monica. And most don’t anticipate embattled Activision founder and Activision Blizzard CEO Bobby Kotick getting comfy in a corner suite on a Microsoft campus any time soon.

But let’s dive into this question: What’s worth more than the content? Arguably…the ownership and control of one of the broadest graphs of consumer data imaginable. Sure, Meta may have access to the data across Facebook, WhatsApp and Instagram…but now, Microsoft suddenly has console, PC, mobile and social gaming profiles and data access. With the acquisition they become the 3rd largest gaming player. But more than posture, Microsoft now has a WHOLE new set of building blocks too with the gaming, subscription, and now that whole massive multiplayer immersive universe creation thing going on. It’s a different multiverse ballgame.

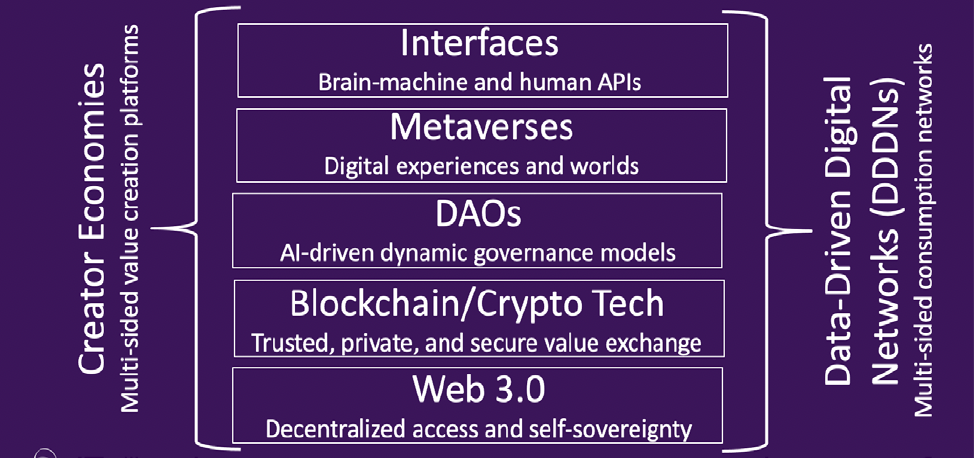

The metaverse economy (which Ray has JUST published an epic report on) will stack five key components that provide the very platform on which creator economies and consumption models will exist within fully immersive digital networks (see below). There are few entities better prepared than gaming and movie studios to build these platforms.

Microsoft’s building materials to establish a metaverse platform has suddenly become FAR more interesting. They have the hardware and cloud aspect of the metaverse stack, and thanks to hardware innovations made on the Xbox hardware itself, have security chips and technologies to establish new security measures for the metaverse stack and network. Add to this the content, expertise in managing, building and engaging MMO players and influencers, the subscription network and player infrastructure to not just create a community but co-create an economy for that community online…this puts Microsoft in instant rival posture to Meta, Apple, Tencent, Epic and Unity.

But let’s extend this just a step down the road…in a fully established metaverse thru which a robust metaverse economy can thrive…gaming and entertainment can’t be the only experiences available. Instead, in this next decentralized and data-driven co-created economy, work and life will also be a collaborative connected effort. So all of a sudden, the lines of business across Microsoft (office, azure and gaming) start to reemerge as key paths and critical infrastructure to a fully formed and fully immersive metaverse.

The metaverse economy will demand that networks and economies transcend the traditional norms of place and space. Who better than Microsoft to draw the first significant battle line in who will build a platform instead of just painting a doorway into the metaverse blue?

While the metaverse may not be “really real” today…these newly painted battle lines sure are. Don’t expect this to be the last salvo.

Principal Analyst and Founder

Constellation Research

R “Ray” Wang is the CEO of Silicon Valley-based Constellation Research Inc. He co-hosts DisrupTV, a weekly enterprise tech and leadership webcast that averages 50,000 views per episode and blogs at www.raywang.org. His ground-breaking best-selling book on digital transformation, Disrupting Digital Business, was published by Harvard Business Review Press in 2015. Ray's new book about Digital Giants and the future of business, titled, Everybody Wants to Rule The World was released in July 2021. Wang is well-quoted and frequently interviewed by media outlets such as the Wall Street Journal, Fox Business, CNBC, Yahoo Finance, Cheddar, and Bloomberg.

Short Bio

R “Ray” Wang (pronounced WAHNG) is the Founder, Chairman, and Principal Analyst of Silicon Valley-based Constellation Research Inc. He…...

Vice President & Principal Analyst

Constellation Research

About Liz Miller:

Liz Miller is Vice President and Principal Analyst at Constellation, focused on the org-wide team sport known as customer experience. While covering CX as an enterprise strategy, Miller spends time zeroing in on the functional demands of Marketing and Service and the evolving role of the Chief Marketing Officer, the rise of the Chief Experience Officer, the evolution of customer engagement, and the rising requirement for a new security posture that accounts for the threat to brand trust in this age of AI. With over 30 years of marketing experience, Miller offers strategic guidance on the leadership, business transformation, and technology requirements to deliver on today’s CX strategies. She has worked with global marketing organizations to transform everything from…...

Microsoft's Biggest Acquisition Is All About Moving To Metaverse

On January 18th, 2022, MIcrosoft announced its intent to acquire Activision Blizzard for $68.7 billion in an all cash offer. As the metaverse economy heats up, this move gives MIcrosoft several advantages including:

Beefed up market presence in the gaming industry and a base in the creation of metaverse worlds. Constellation estimates that the combined deal will give MIcrosoft more than 10% of the gaming market. Activision titles such as Warcraft, Diablo, Overwatch, Call of Duty, and Candy Crush join Microsoft's Xbox game pass and PC Game pass. The massive collection of titles and digital assets can be leveraged to grow the 25 million subscribers on XBox Game Pass.

POV: Gaming software companies along with movie studios are a great place to build a platform for future worlds. The acquisition is a bet on building a metaverse platform to rival Apple, Epic, Meta, Niantic, Roblox, and Unity. In 2021, MIcrosoft added to its gaming library with its acquisition of Bethesda for $7.5 billion. While this may seem aggressive, MIcrosoft has had to compete with Tencent and Sony's buying sprees.

Pressure to improve Hololens hardware and retain metaverse talent. Microsoft has had the hardware aspects of the metaverse stack and a significant gaming library.While Hololens was innovative when launched in 2015, the pace of development has been slow and competitors such as Meta's Ocuclus, Sony, HTC, and Valve have run rings around Microsoft's Hololens 2 in quality, battery life, speed, and price.

POV: The doubling down on gaming and metaverse should give Microsoft's gaming chief, Phil Spencer, new ammo to make the improvements in Hololens 3 that will take the hardware to the next level and drive cross-sell. Hopefully these actions will stem the defections of metaverse talent from Microsoft as the Wall Street Journal has reported a brain drain to Meta. Recruiters have confirmed key talent headed to Apple, Epic, Nviidia, Unity and others.

Win over Google Cloud for gaming workloads and loss to YouTube Ad revenue. Blizzard's origiinal footprint included 10 AT&T data centers for hosting World of Warcraft. At some point, AWS played a role in the hosting but over time Jacques Erasmus, CIO of Activision Blizzard, consolidated the sprawling network of data centers and colocation contracts. Candy Crush was an origiinal Google Cloud customer. Eventually, Google won the Activision Blizzard account in 2020 amidst much fan fare. Google even paid Activision Blizzard $160 million over three years for exclusive streaming rights for events and eSports leagues on Google's YouTube properties.

POV: The win puts MIcrosoft Azure in a great position for hosting the significant gaming workloads. With a handover expected in 2023, Google Cloud will lose a key tenant and ad driver for YouTube. Microsoft will gain valuable experience in hosting metaverse worlds and attempt to bring more users onto Microsoft platforms.

The Bottom Line: Expect More Partnerships And Mergers As Vendors Rush Into The Metaverse

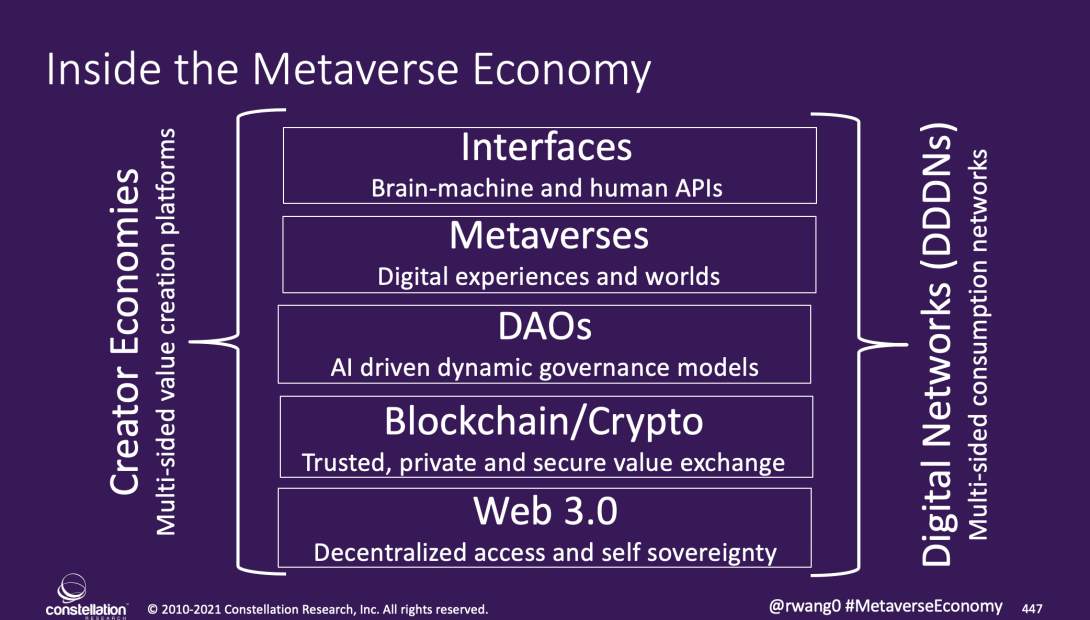

Constellation predicts that advances in the metaverse economy will provide a critical element of the “Great Refactoring” ahead and a $21.7 trillion market by 2030. Massive consolidation ahead will come as metaverse players seek to gain proficiency across the five layers of the Metaverse Economy (see Figure 1). There will be an arms race for all aspects of the metaverse economy which includes the interfaces (hardware), the metaverse worlds, the DAOs, the value exchanges in crypto, tokens and coins, and the Web 30 infrastructure.

Figure 1. The Five Layers Of The Metaverse Economy

Enterprises interested in the metaverse economy can start by applying the 43 enterprise use cases that focus on engagement and experiences to support the future of work, employee experience, customer experience, and commerce.

Principal Analyst and Founder

Constellation Research

R “Ray” Wang is the CEO of Silicon Valley-based Constellation Research Inc. He co-hosts DisrupTV, a weekly enterprise tech and leadership webcast that averages 50,000 views per episode and blogs at www.raywang.org. His ground-breaking best-selling book on digital transformation, Disrupting Digital Business, was published by Harvard Business Review Press in 2015. Ray's new book about Digital Giants and the future of business, titled, Everybody Wants to Rule The World was released in July 2021. Wang is well-quoted and frequently interviewed by media outlets such as the Wall Street Journal, Fox Business, CNBC, Yahoo Finance, Cheddar, and Bloomberg.

Short Bio

R “Ray” Wang (pronounced WAHNG) is the Founder, Chairman, and Principal Analyst of Silicon Valley-based Constellation Research Inc. He…...

Vice President and Principal Analyst

Constellation Research

About Andy Thurai

Andy Thurai is an accomplished IT executive, strategist, advisor, enterprise architect and evangelist with more than 25 years of experience in executive, technical, and architectural leadership positions at companies such as IBM, Intel, BMC, Nortel, and Oracle. Andy has written more than 100 articles on emerging technology topics for publications such as Forbes, The New Stack, AI World, VentureBeat, DevOps.com, GigaOm and Wired.

Andy’s fields of interest and expertise include AIOps, ITOps, Observability, Artificial Intelligence, Machine Learning, Cloud, Edge, and other enterprise software. His strength is selling technology to the CxO audience with a value proposition rather than the usual technology sales pitch.

Find more details and samples of Andy’s work on his…...

Vice President and Principal Analyst

Constellation Research

Title: About Dion Hinchcliffe

Dion Hinchcliffe is an internationally recognized business strategist, bestselling author, enterprise architect, industry analyst, and noted keynote speaker. He is widely regarded as one of the most influential figures in digital strategy, the future of work, and enterprise IT. He works with the leadership teams of large enterprises as well as software vendors to raise the bar for the art-of-the-possible in their digital capabilities.

He is currently Vice President and Principal Analyst at Constellation Research. Dion is also currently an executive fellow at the Tuck School of Business Center for Digital Strategies. He is a globally recognized industry expert on the topics of digital transformation, digital workplace, enterprise collaboration, API…...

Former Vice President and Principal Analyst

Constellation Research

Doug Henschen is former Vice President and Principal Analyst where he focused on data-driven decision making. Henschen’s Data-to-Decisions research examines how organizations employ data analysis to reimagine their business models and gain a deeper understanding of their customers. Henschen's research acknowledges the fact that innovative applications of data analysis requires a multi-disciplinary approach starting with information and orchestration technologies, continuing through business intelligence, data-visualization, and analytics, and moving into NoSQL and big-data analysis, third-party data enrichment, and decision-management technologies.

Insight-driven business models are of interest to the entire C-suite, but most particularly chief executive officers, chief digital officers,…...

Vice President and Principal Analyst

Constellation Research

Holger Mueller is VP and Principal Analyst for Constellation Research for the fundamental enablers of the cloud, IaaS, PaaS and next generation Applications, with forays up the tech stack into BigData and Analytics, HR Tech, and sometimes SaaS. Holger provides strategy and counsel to key clients, including Chief Information Officers, Chief Technology Officers, Chief Product Officers, Chief HR Officers, investment analysts, venture capitalists, sell-side firms, and technology buyers.

Coverage Areas:

Future of Work

Tech Optimization & Innovation

Background:

Before joining Constellation Research, Mueller was VP of Products for NorthgateArinso, a KKR company. There, he led the transformation of products to the cloud and laid the foundation for new Business Process as a…...

Vice President & Principal Analyst

Constellation Research

About Liz Miller:

Liz Miller is Vice President and Principal Analyst at Constellation, focused on the org-wide team sport known as customer experience. While covering CX as an enterprise strategy, Miller spends time zeroing in on the functional demands of Marketing and Service and the evolving role of the Chief Marketing Officer, the rise of the Chief Experience Officer, the evolution of customer engagement, and the rising requirement for a new security posture that accounts for the threat to brand trust in this age of AI. With over 30 years of marketing experience, Miller offers strategic guidance on the leadership, business transformation, and technology requirements to deliver on today’s CX strategies. She has worked with global marketing organizations to transform everything from…...

Former Vice President and Principal Analyst

Constellation Research

Steve Wilson is former VP and Principal Analyst at Constellation Research, leading the business theme Digital Safety and Privacy. His coverage includes digital identity, data protection, data privacy, cryptography, and trust. His advisory services to CIOs, CISOs, CPOs and IT architects include identity product strategy, security practice benchmarking, Privacy by Design (PbD), privacy engineering and Privacy [or Data Protection] Impact Assessments (PIA, DPIA).

Coverage Areas:

- Identity management, frameworks & governance- Digital identity technologies- Privacy by Design

- Big Data; “Big Privacy”- Identity & privacy innovation

Previous experience:

Wilson has worked in ICT innovation, research, development and analysis for over 25 years. With double…...

Despite the chaotic pandemic environment, 2021 was an amazing year for enterprise tech IPO's, product launches, and new technologies. CXO's were given the budgets to refactor their business models, add additional talent, and invest towards a digital future. Amidst this backdrop, enterprises changed how they worked, what they sold, how they monetized, why they existed, and who they worked with. The underpinnings of what is known as the "Great Refactoring" began in 2021 and will fully emerge into 2022 and beyond..

The technology vendors named into this year's Enterprise Awards have show how they can partner with clients to be successful, show resiliency despite the harshest selling environments, and innovate despite the constraints placed on their businesses. It's with pleasure to announce the 2021 Constellation Enterprise Award winners.

BEST ENTERPRISE SOFTWARE STARTUP

This category recognizes when an enterprise software startup achieves escape velocity in mind share and relevance.

WINNER: Starburst Data

Why did they win? Starburst Data is advancing the Trino project as an open source platform for lakehouses and data mesh architectures. The well-funded 2017 startup brings together multiple Presto co-creators with enterprise tech veterans to pursue cloud-native companies operating at massive scale as well as enterprise giants with data strewn across cloud and on-premise sources invariably including multiple lakes and warehouses. The company's mission is to be enable access to data wherever it lives, and more than 150 large, data-driven organizations already rely on Starburst Data to do just that, including Comcast, Conde Nast, Finra, Verizon and VMWare. [Doug Henschen]

RUNNERS UP: Auditoria.AI

Why were they recognized? The field of cognitive automation continues to grow. Auditoria.AI applies intelligent SmartBots to automate manual, error prone, and time-consuming finance processes for accounts payables and accounts receivables. Using AI, Auditoria works with ERP systems, accounting platforms, and other financial systems of record. Partnerships with Bill.com, Oracle ERP Cloud, Oracle NetSuite, Sage Intacct, Workday, and collaboration tools such as Microsoft 365 and Google Workspace have put Auditoria on the map for back office cognitive automation. In addition, Auditoria was a winner of Constellation's 2021 The Pitch awards. [R Wang]

RUNNERS UP: Horizon3.AI

Why were they recognized?

Horizon3.ai is one of the winners of Constellation's 2021 The Pitch awards. The startup provides Red Teaming services that simulate a cyber security attack. Their penetration testing platform, NodeZero, constantly assess an organization's attack surface. From harvested credentials, misconfigurations, dangerous product defaults, and exploitable vulnerabilities to compromise your systems and data, Horizion3.ai's use of knowledge graph analycis and adaptive attack algorithms work to identify vulnerabilites . . Our core innovation is the use of knowledge graph analytics combined with adaptive attack algorithms. From a fresh round of investment to growing awareness in the market place among CISO's, this Autonomous Security Platform is gaining mindshare among the security elite. [R Wang]

RUNNERS UP: Varada

Why were they recognized?

Mastering data is the foundation of digital transformation. Varada provides customers with a dynamic and adaptive big data indexing solution. The proliferation of data requires the ability to run any query including ad hoc, experimental analytics and vast discovery projects. Varada has emerged as a critical solution for organizations building digital proficiency and competing on decision velocity. As one of the 2021 The Pitch award winners for data to decisions, Varada is a stand out solution. [R Wang]

BEST ENTERPRISE SOFTWARE VENDOR This category recognizes the enterprise software vendor who improved their customer relevance, market share, customer satisfaction, and brand standing.

WINNER: Adobe

Why did they win? Adobe has been making some interesting moves to bring the Experience and Creative clouds closer together. Customre feedback from system integrators like Accenture, Deloitte and even IBM Services, confirms that 2021 was the year Adobe has gotten serious about extending experiences beyond marketing tools for marketing people. Previously when it came to "transformational projects", most system integrators did not truly take Adobe seriously for anything outside of Marketing until they dug into the open source Experience Data Model (XDM), These integrators have been impressed with the XDM when it finally was delivered in a usable format late 2020. In addition, the Workfront and Frame.io acquisitions focus on how the actual work of Experience is conducted and new tools around commerce, content and assets bring some significant evolution to where, how and why experiences are delivered. Closing out the year, Adobe answered the evolving marketplace with their strategy that can only be described as being the Canva-killer, clearly taking aim at digital upstarts that had threatened to upend their dominance in the graphics, creative and video space. When it comes to numbers, 2021 was good to Adobe with $15.79 billion in revenues, representing a 23 percent year over year growth. They have strengthened their partnerships with Microsoft and ServiceNow which has also helped raise their profile and their reputation with IT buyers. [Liz Miller]

RUNNERS UP: Snowflake

Why were they recognized? Snowflake kept the momentum from its 2020 IPO going quite nicely in 2021, racking up triple-digit year-over-year gains in revenue as customers continued to flock to the major public clouds. Whether those customers are moving existing data warehouses or launching new data collections in the cloud, Snowflake's one-platform, multi-cloud message seemed to resonate with customers wanting choice as well as service consistency across AWS, Microsoft Azure and Google Cloud. Snowflake also took multiple steps in 2021 to support unstructured data and data science, building its Snowpark partner community and opening up options to work in Python, Java and Scala. The icing on the cake is the Snowflake Data Marketplace, which provides a governed platform for partners to share data and a commerce-enabled store where data owners can monetize their assets. [Doug Henschen]

RUNNERS UP: Oracle Why were they recognized? Traditional IT vendors have often failed and few have excelled in the cloud era. Oracle is one remarkable exception and with solid execution in 2021. This success spans the spectrum of SaaS, PaaS and IaaS, Oracle even managed to change their cloud rankings at a reputable analyst firm. This type of improvement has not happened in over a decade. Across the major cloud vendors, Oracle has the most enterprise IT friendly cloud, and plans to match market leader AWS in 2022 in terms of locations and regions offered. Locations matter for cloud due to data residency and performance requirements. On the PaaS side Oracle has advanced its autonomous vision, which surprisingly remains un-answered but almost the entirety of the competition. Larry Ellison's vision of the "chip to click" stack materlalizes in no place better than Oracle Exadata and its various offerings. Interestingly, Oracle is gaining a second revenue stream for databases, with a number of smart, code based innovations around its mySQL offering with HeatWave. Finally Oracle has been in a strong position on the SaaS side for years, but has managed to improve breadth and depth of its enterprise suite offerings, once again. At the moment there is no more complete and functional rich enterprise automation suite than Oracle Fusion. Customers hope Oracle does not rest on in its laurels. With the largest planned acquisition in its history - Cerner, this would cements its offerings in the largest vertical of the US economy and guarantee future revenue streams while locking out competitors from this key vertical. [Holger Mueller]

RUNNERS UP: Servicenow

Why were they recognized?

CEO Bill McDermott and team continue to add great talent to the team, expand offerings, and make key AI acquisitions required for future growth. This has led to strong quarter to quarter revenue growth and a $115 billion market cap with admission to the Fortune 50 club. Acquisitions this year include tuck-ins with DotWalk, Intellibot, Lightstep, Gekkobrain, Mapwize, and Swarm64. Significant partnerships with 3Clogic, Celonis and Microsoft highlight a more alliance friendly approach. System integrators are clamoring to poach and hire Servicenow talent. [R Wang]

BEST ENTERPRISE SERVICES VENDOR This category recognizes the enterprise services vendor that transforms delivery models and crafts new client–centric market approaches. WINNER: Accenture

Why did they win?

Accenture and CEO Julie Sweet pulled out all the stops to lead the market with significant revenue growth and strategic partnerships. The Q1 2022 numbers showed a $3.21 billion increase YoY from Q1 2021 or 27% increase. These numbers reflected both growth in outsourcing revenues and consulting revenues. The firm's 360° value approach paid off with 20% or more growth in all regions and service lines. Key cloud partnerships and strong hires led to a 58% increase in stock price for 2021. As clients continue to deploy digital transformation projects, Accenture has kept ahead with hiring of scarce skills and preparation for new business models in the Great Refactoring. [R Wang]

RUNNERS UP: Wipro

Why were they recognized?

Wipro is in the midst of a major turnaround. CEO,Thierry Delaporte has made significant hires to the management team including a new CRO, a new CEO of European Operations, and head of business development. The company has not been shy about entering new markets with acquisitions. In fact, 2021 was a busy year for acquisitions including Capco, Ampion, Edgile, and Leanswift. The investment of $1 billion into cloud transformation with the Fullstride offering has been well received. Most importantly in 2021, Constellation witnessed Wipro undergoing a massive cultural shift and making the right moves for the future. [R Wang]

BEST TECH ACQUISITION This category recognizes the enterprise tech acquisition that has the most impact for customers, market landscape, and the overall industry direction.

WINNER: Oracle + Cerner

Why did they win?

Oracle's $28.3 billion acquisition of Cerner will allow Oracle to enter the healthcare space and at the heart of heatlhcare transactions, the electronic medical record. Cerner's focus on software for hospitals and doctors provides great workloads for Oracle's cloud and an opportunity to cross-sell Oracle's applications into a highly specialized industry vertical. Healthcare consumes 20% of the US gross domestic product and will make Oracle the second largest vendor after Epic Systems Corp. Cerner has a strong presences in the federal and state markets but has been losing to Epic in the for-profit market. With this acquisition, Oracle will breathe new life into Cerner. Customers hope Oracle puts Epic on alert for its abuse of market position and priciing and inject much needed competition in this market. [R Wang]

Why were they recognized? Salesforce/Tableau acquires Narrative Science. This late-in-the-year, under-the-radar acquisition brought Narrative Science, the best-of-breed natural language analysis and insight-generation company, into the portfolio of the CX and analytics leader. Natural language query is increasingly the interface for analytics exploration, and using its Lexio data storytelling tech, Narrative Science was already helping companies explore and gain insight well beyond the confines of static reports and dashboards. Look for the combination of NLQ and Lexio to enhance Tableau's embedding capabilities and delivery of actionable insights. There's also little doubt that Narrative Science tech will soon raise the IQ of the "Ask Einstein" feature wherever it's exposed throughout the Salesforce portfolio. [Doug Henschen]

RUNNERS UP: Adobe + Frame.io

Why were they recognized? Adobe / Frame.io acquisition is one of my favorites of 2021. If one could count the Workfront acquisition, Adobe shelled out almost $2.8 BILLION for collaboration in less than 12 months. The Frame.io pickup changes the game for HOW organizations reshape collaboration across video creation from the creator to creatives and campaigns. While Workfront has gotten a lions share of attention, Frame.io is a technical powerhouse in video and will retain a LARGE portion of their film creator, editor and director customers that can remain platform agnostic and still use Frame.io as their primary conduit to collaboration and even content submission and storage. For Adobe, the collaboration and AI engines that come under the hood are especially exciting when the Frame.io and Workfront pictures come together. Both pickups are about how content, creators and marketers actually WORK...and how businesses can finally start to WORK with these artsy creators with a LOT less pain and grousing (one hopes). [Liz Miller] RUNNERS UP: Intuit + Mailchimp

Why were they recognized? Intuit, touted as a platform for DIYers whether it is for personal use or for small business, acquired MailChimp last year for $12 billion. Given that the majority of small business owners try to do things on their own and keep their costs low, this acquisition gives Intuit an opportunity to market and cross-sell their platforms in accounting, tax, credit, etc. with an eye on helping these small business owners with marketing in that process. Given that MailChimp owns about three-fourth (yup, close to 75%) of the email campaign market the deal logic makes sense.

Intuit wanted to disrupt the small business mid-market. MailChimp rose from the ashes of a failed online greeting card company to amass 13 million users with a revenue of US $800m in 2021 and unlike the Intuit business model, MailChimp has a recurring revenue model. The 13 million user base addition to their existing 100 million user base for Intuit is a big deal hence they paid a whopping $12B.

MailChimp's boot strapped business model is unique in the tech world. For instance, the foudners never received VC or outside funding. This is the largest payout for a company that never took funding from outside. From the Intuit side, this is the second biggest acquisition within a year after acquiring Credit Karma for $8.1B just nine months earlier. Intuit's shareholders are hoping this will help them grow in the $300B target market.[Andy Thurai]

RUNNERS UP: Citrix + Wrike

Why were they recognized? Cloud computing firms are waking up to the reality that low level IT services don't directly provide the high business impact of services that enable specific business functionality. This has led many cloud services firms to look to the sustainable growth of a Salesforce or Workday, even as they offer more fundamental capabilities as their core business. Enter Citrix, a stalwart cloud and virtualization tech firm that provides server, application and desktop virtualization, networking, software-as a service, and other lower-level cloud computing technologies.

In a demonstrated desire to better position the company higher in the digital workplace stack, in early 2021 Citrix acquired Wrike, a well-known developer of work coordination and collaborative workspace softwarefor $2.25 billion in cash. Clearly aiming at the white hot "Future of Work" category made even more popular by the pandemic, Citrix has been able to use its Wrike acquisition to position itself has a richer set of offerings for the fundamentals of the modern digital workplace. Digitization and the adoption of flexible and hybrid work models continue to have high importance to customers and so the Write acquistion cements Citrix's growth vector up into a broader world of digital workplace services.

The work coordination industry itself, which Wrike is a leader in, is one of the growth stories of the business software industry. This means Citrix will also be able to use the Write acquisition to grow revenue and not just play in a higher-order category of tools. Citrix needs this evolution if it hopes to successfuly compete in services to help today's workers collaborate more efficiently and effectively across work channels, devices and locations. In the end, Wrike's broad horizontal applicability to digital workplace activities will help Citrix move into more of a Microsoft-style enterprise software provider with a broader appeal to buyers looking for strategic partners that can help them build the employee experiences of the future. [Dion Hinchcliffe]

WORST TECH ACQUISITION This category recognizes the enterprise tech acquisition that had the least impact for customers, market landscape, and the overall industry direction.

WINNER: Panasonic + Blue Yonder

Why did they win? Panasonic buys Blue Yonder: What the...? Panasonic acquired Blue Yonder for $7.1 billion in April, adding the Arizona-based AI, IoT, and edge computing technology company to its Autonomous Supply Chain offering. Who knew Panasonic was in business of helping customers better track their supply chains and predict future demand? It may not be the worst acquisition, but maybe Panasonic (like Hitachi) needs to spin out a new brand that isn't so associated with consumer electronics. Constellation believes a team of 100 developers could build the needed funcitonlaity in less than 3 years for less than $500M, but what the heck? [Doug Henschen and R Wang]

RUNNERS UP: Block (Square) + Tidal

Why were they recognized? A few weeks ago one would have said Square buying Tidal...hands down, the biggest dog of an acquisition. But now we are in a world where Tidal is actually changing digital payment models in music with direct to artist payments and now with Jack becoming the king of blockchain and crypto, one won't expect to see Tidal slowing their roll and Constellation can see them becoming the source for artist-driven NFTs. Hey...if Elon's ex Grimes can sell $6m in NFTs, imagine what JayZ and Beyonce will do. [Liz Miller]

RUNNERS UP: Zoom + Five9

Why were they recognized?

Is it fair to have this appear (sorta) 2x on this...but is a non-acquisition considered the worst...Zoom / Five9? I mean, it isn't as bad as TikTok and neither org had their stock price get nailed as a result of the call-off...but wow. What a bummer. [Liz Miller]

RUNNERS UP: Okta + AUTH0

Why were they recognized?

The financials of the deal are almost certainly good for Okta, whose revenues in their last few years from their customer identity product has grown to 25% of total revenues from almost nothing. However, many have asked why would Okta pay $6.5 billion in stock for a company that basically provides some authentication APIs, esssentially not that much more than the sign-up forms with social networking support that you see on popular Web sites. Most likely Auth0's $200 million in annual recurring revenue had something to do with it. However, the reason this deal isn't a good one is because of Okta's poor reputation for being developer friendly. Auth0 has real credibilitiy in the tech industry, while Okta is much more oriented around enterprise IT and response by developers to this acquisition has been notably poor. It's likely going to leave a lot of existing customers unhappy and ready to defect to the next upcoming provider, while bolstering Okta's bottom line less than they hope. [Dion Hinchcliffe]

BEST PARTNERSHIP This category recognizes the enterprise partnership that delivered the most impact for customers and the market.

WINNER: Kyndryl + Microsoft

Why did they win? Kyndryl plus Microsoft (and more Kyndryl partnerships to come). When IBM spun out its $19 billion infrastructure services business as Kyndryl in November, a world of new partnerships became possible. The deals led off with an exclusive Premier Global Alliance Partnership with Microsoft centered on that vendor's cloud platform. This deal was quickly followed by a deeper app-modernization and multicloud-services partnership with VMware. It's still early days for digital transformation and cloud migrations for the world's largest companies, and there are signs that stand-alone Kyndryl will be in a better position to be an agile competitor and proactive partner in pursuit of the $500 billion managed services market. [Doug Henschen]

RUNNERS UP: Google + Ford

Why were they recognized?

The Ford Motor Company and Google announced a six-year extensive business and technology partnership. Ford's VP of Strategy, David McClelland clarified that Ford chose Google for leadership in AI and ML, robustness of the Android operating system, strength of Google Assistant for voice technology, and mapping and navigation technology. Thomas Kurian, CEO of Google Cloud noted that Google and Ford will build a co-creation digital transformation team focused on manufacturing, purchasing, and factory floor modernization. Other potential opportunities include new retail experiences, new ownership offers based on connected vehicle data, and other product development modernization efforts involving AI and data. Ford was clear that Google was the preferred cloud vendor and other partnerships with Amazon for Alexa and Apple for Car Play would remain as choices for customers. This partnership with Google benefits Ford by allowing our employees to harness the power of data in smarter and innovative ways. Customers will get better and smarter in-vehicle experiences. Given what's been publicly discussed by Google and Ford, this is the beginning of many such Data Driven Digital Network partnerships by Google in each strategic industry. One can expect to see more of these as industries collapsed around value chains and tech partnerships around data and AI improve the competitive landscape. While every cloud vendor will be a strategic partner, the real question is which industry leaders will build, partner, or be punished in a world of digital giants. [R Wang]

RUNNERS UP: Servicenow + 3CLogic

Why were they recognized? Might be a small one, but Constellation still thinks this is a cool partnership: ServiceNow plus 3CLogic. ServiceNow has been actively pushing its experience-focused workflow capabilities, notably with investments into service and field service management solutions and use cases. What the partnership with 3CLogic provides is adding voice services to their field service, HR Service and IT service solutions. With FSM, 3CLogic steps up ServiceNow's capabilities to include self-service voice-based experiences, automated actions from voice engagements, live and virtual agent interactions and advanced AI-powered conversational analytics without leaving their existing ServiceNow environment -- use case example: ServiceNow administrators can build workflows for IVR journey based on 3CLogic's drag-and-drop designer...IN ServiceNow. It gives ServiceNow telephony without having the BUILD telephony. This release dropped yesterday...Nissan connected 3CLogic to their ServiceNow application to bring voice and SMS to the party for their HR service application. https://www.businesswire.com/news/home/20211207005002/en/3CLogic-Selected-to-Provide-Voice-and-SMS-Services-for-Nissan’s-HR-Service-Center [Liz Miller]

BEST CEO This category recognizes the best enterprise CEO. Enough said.

WINNER: Frank Slootman, Snowflake

Why did he win? Frank Slootman took over as CEO at Snowflake in April 2019 with the goal of guiding the company to a successful IPO. It's a task he had successfully handled twice before, at Data Domain and ServiceNow, but Snowflake's $3.9 billion IPO haul in 2020 stood out as the software industry's largest ever and the fifth largest among U.S.-based tech listings (after Facebook, Uber, Agere Systems and Snap). Slootman has since kept Snowflake focused, ashewing calls for an on-premises offering and concentrating on growing it's single-platform, multi-cloud service that offers consistency and choice across AWS, Microsoft Azure and Google Cloud. That focus has been rewarding, with Snowflake racking up triple-digit year-over-year revnue gains in 2021. "CEOs are only there for one reason, and that is they need to win," Slootman told Forbes in a 2021 interview. "When you win, nobody can hurt you. And when you lose, nobody can help you.” [Doug Henschen]

RUNNERS UP: Rowan Trollope, Five9

Why was he recognized? Gotta give a nod to Rowan Trollope, CEO @ Five9. In the CCasS/UCaaS space, Five9 is a player...but the minute that Zoom deal was announced, a red hot spotlight hit that company. Under different leadership, when the deal was called off, things could have gotten ugly. Instead, Q3 saw revenue growth of 38%. Five9 is riding a wave of increased subscriptions as well as seeing some payoffs from their 2020 investments into cloud-native solutions and a big push into AI-driven service, routing and operations for call center. Beyond what the company has been able to do Trollope has been out there openly daring the call center industry specifically, and business as a whole, to transform voice and communications...something that has been slow to happen and that many in the market aren't really ready to have happen. But Trollope's bet that being the big voice on voice is paying off as other competitors are still trying to find their thought leadership legs. [Liz Miller]

RUNNERS UP: Safra Catz, Oracle

Why were they recognized? After the unfortunate and early passing of Mark Hurd, Saffra Catz was given the sole CEO role and has delivered. Amongst the few IT vendors being the trusted partners of CIOs and CTOs, Oracle is the strongest and most relevant provider of technology. The combination of Ellison and Catz forms one of the very few 20+year partnerships at the highest executive level and they understand each - blindly. The division of labor is clear - Ellison does technology and Catz the 'rest'. But for the technology to work, the rest needs to work as well, making sure that sales and marketing work, making sure consulting services and partners deliver and that support keeps customers in good shape. That all will growing the cloud business of Oracle, even recently climbing on the #3 stop according to a prominent analyst firm. The Cerner acquisition is Catz's boldest move, and if cleared and successful, will mark as the biggest move that Oracle has done in its history - so Catz has the company in its reins during the most transformative time in IT -having successfully evolved Oracle from 'still relevant' to 'relevant' and into growth mode. [Holger Mueller]

BEST NEW ENTERPRISE CATEGORY This category recognizes the best new enterprise category that made an impact to the market.

WINNER: Environmental, Social, Governance (ESG)

Why did they win? Environmental, Social, and Governance solutions. Like it or not, ESG compliance initiatives are coming. Whether it's carrots -- like access to capital, partnerships and supplier contracts -- or sticks -- in the form of government regulation -- mainstream enterprises are increasingly embracing ESG reporting solutions, software and services. The E in ESG has been leading the way, with oil and gas and other carbon-intensive industries embracing reporting standards and ways to measure progress toward sustainability gools. Asset managers, investors, activist groups and forward-looking companies are turning up the heat on the E, S and G fronts across industries. Tech vendors and businesses will naturally follow the money, leading to a growing ESG market and a growing embrace of reporting solutions, software and services across industries. What's wanting is consolidation of ESG standards and regulations across a confused global patchwork. Only then can technologies including automation, AI and ML help to soften the blow of new ESG compliance costs. [Doug Henschen]

RUNNERS UP: Metaverse Economy

Why were they recognized? Much hype has been made about the Metaverse. However, very few organizations have fully grasped the impact that the metaverse will have on experiences and engagement inside the enterprise. More than just gaming worlds or hardware devices, the metaverse economy brings new opportunities for enterprises to bring their physical presence and 3-D digital presences together in one unified offering to their stakeholders – customers, employees, partners, and suppliers.

Constellation predicts that advances in the metaverse economy will provide a critical element of the “Great Refactoring” ahead and a $15 trillion market by 2030. [R Wang]

BEST NEW IPO This category recognizes the most successful IPO for the year

WINNER: Freshworks

Why did they win? As the story goes, Freshworks started after CEO Girish Mathrubootham struggled through a nightmarish service experience with a broken television. Originally founded in Chennai, India, now based in San Mateo, CA, Freshworks went public with a valuation of $12 billion making it the first Indian SaaS company to be listed on the NASDAQ. Freshworks focuses on the experience side of software, looking to deliver customer and employee experiences with an emphasis on sales and support, IT services management, and call center software on the cloud. Unlike some competitors that have sought to glamorize the allure of experiences, Freshworks has focused on a core belief that delivering experiences should be as simple as actually experiencing them. This has led to simplified pricing models and streamlined product offerings. What makes the Freshworks IPO especially interesting is the emergence of a new, more service-born and customer-focused CRM and engagement player to take on platforms like Salesforce. [Liz Miller / R Wang]

RUNNERS UP: Hashicorp

Why were they recognized?

Cloud technology has been blazing a growth trail in the public markets over the last several years. Whether it’s compelling new software-as-a-service (SaaS) plays, cloud infrastructure firms, or cloud databases -- if it’s in the cloud, it’s hot. One of the most recent stars is HashiCorp, a provider of cloud infrastructure automation services to provision, secure, connect, and run cloud infrastructure. A tech darling in cloud computing circles because their tools can help take the hard work and drudgery out of securing and implementing cloud-based systems, the company raised $1.2 billion on December in an Initial Public Offering (IPO) that gave the company a $15 billion valuation. HashiCorp, now trading under the symbol “HCP” on NASDAQ, proved the new cloud entrants can still make a big splash. The sale exceeded the goals for the stock offering, and made it one of the largest and most successful tech IPOs of the year. [Dion Hinchcliffe]

RUNNERS UP: Walkme

Why were they recognized?

The rapidly growing category of digital adoption platforms (DAPs) -- tools that help companies and workers get more from the IT systems and applications they use -- had a major proof point in the IPO of WalkMe last June. The firm is a leading Israeli-based SaaS company whose stock value has held overall even in the volatile markets, making what is arguably the category leaders a notable winner. WalkMe's code-free platform uses specially tuned algorithms to provide visibility to an organization's Chief Information Officer (CIO) and business leaders so they can then use the platform to better optimize business performance, by improving user experience, productivity and efficiency for employees and customers. While DAPs are still often flying under the radar in parts of the IT industry, WalkMe's debut has solidifying the category in the financial markets while also showing the category has legs in helping organizations strategically achieve higher returns from their IT and talent investments. [Dion Hinchcliffe]

RUNNERS UP: Sprinklr

Why were they recognized?

The social software company headquartered in NYC, went public in June with a $4 billion valuation on $387 million in revenues and a loss of $41 million. The company has developed and acquired a number of tools in social media management, marketing, content, and advertising. Sprinklr is one of the top tech companies in the New York City metropolitan area and its IPO will fund future tuck-in acquisitions and complete their vision to compete head on with Salesforce.com. [R Wang]

RUNNERS UP: Qualtrics

Why were they recognized?

Sliicon slopes launched another IPO on January 28th, with a spin out from SAP and a $27.3 billion valuation. The company has evolved from a survey software tool to an experience platform for companies like Adidas, BMW, Disney, and more looking at customers and employees. Qualtrics has brought a lot of value to shareholders and investors and in its current iteration has added some top talent including a new COO and Chief Revenue Ops leaders, Abhi Ingle from AT&T. [R Wang]

RUNNERS UP: UI Path

Why were they recognized?

Founded in Romania, UI Path pioneered the robotic process automation (RPA) space. The company launched with a valuation of $35.8 billion and has managed to grow revenues to $608 million and narrow its losses from $519.9 million to $92 million. As the market consolidates and moves to infinite ambient orchestrations, expect a rash of consolidation. [R Wang]

BEST NEW ENTERPRISE SOFTWARE MARKETING OF THE YEAR This category showcases the best marketing campaign, ad, or perception transformation in the enterprise.

WINNER: Salesforce

Why did they win? BUT...it is going to be hard to beat the marketing campaign and content juggernaut that is Salesforce this year. Salesforce+ has been chalk full of compelling and exceptionally produced content that speaks to the general market as much as it speaks to their real rabid audience, their trailblazers. The content is geared for all levels of buyers and gives new on-going life to event related content for Dreamforce and Slack Frontiers. They made the investment...but 2022 will be the test to see if it pays off, especially as the expectation to return to live experiences tests the whole "Netflix for Enterprise" concept when the content only comes in one color blue. For Salesforce+ to succeed beyond a really terrific marketing launch in 2021, the partner ecosystem will need to step into the content generation game so more 'channels" give viewers that sticky reason to return. [Liz Miller]

RUNNERS UP: Zendesk

Why were they recognized? Zendesk is consistently good with consistently good marketing. They just don't overcomplicate their message or their content and, best of all, practice what they preach by creating compelling and relevant content in their own Helpdesk content stores. They have been willing to experiment with different content formats from informational technology sessions to webinars with customer stories that are entertaining and compelling because they are unfiltered and honest. Their hero message and theme of "Champions" resonates with organizations that want to be "experience champions" to individual agents working to be "service champions"...it all works within their message of empowerment through chat, AI and all around better service and engagement. [Liz Miller]|

RUNNERS UP: UKG Why were they recognized?

UKG was faced with the challenge to merge two strong brands, Kronos and Ultmate Software. Coming up with the new acronym UKG for Ultimate Kronos Group and combining it with the new smiley logo, was one of the most daring branding moves in tech. But it worked off, not only did it rally customers and employees to the joint company, but through smart sponsoring of events and athletes, the brand has seen more exposure with HCM decision makers and users than much larger competitors in the space. [Holger Mueller]

RUNNERS UP: The Tradedesk

Why were they recognized? With the pandemic forcing every business to operate the majority online, digital advertising companies got an unexpected boom. Especially, with consumer buying patterns moving to buy online, every company wants to optimize their advertisement spending on the digital channels where it matters. This is where companies like Trade Desk have an edge by helping marketers and ad agencies optimize their ad spend across all digital channels to drive the maximum revenue. Programmatic advertising platforms like Trade Desk use software to buy ads automatically, based on criteria, timeframe, and specific data to maximize the reach and revenue potential - all data-driven, in real-time, and very efficient to avoid wastage so they can do more with less. Programmatic ads based on data are the future most digital companies are moving towards.

With the market share competition against Google and Facebook which is very successful in this area, Trade Desk can offer effective marketing programs across different media channels vs brand awareness or limited customers within those platforms' reach. [Andy Thurai]

BEST NEW ENTERPRISE SOFTWARE AD CAMPAIGN This category showcases the best ad campaign in the enterprise.

WINNER: Microsoft

Why did they win? Microsoft has been on POINT with their marketing and advertising campaigns. But REALLY have to give biggest props to the team at Nuance (now owned by Microsoft.) They cranked out one of my FAVORITE ads and overall campaigns around customer experience: We, the customers. https://youtu.be/fAVLKo_-WAA This had me ROLLING from the first time I saw it and was turned into scripts and snippets of customer wishes thru the summer...so I'm just going to count their win to Microsoft...but not really. ;) [Liz Miller]

RUNNERS UP: Adobe

Why were they recognized? -- Also been loving these quick bites from Adobe Experience Cloud (OK yes, perhaps an ad / creative advantage, but these quick spots are hysterical and speak to the stupid things we marketers do to ourselves. Check the Experience Cloud playlist here. [Liz Miller]

BEST LIVE-EVENT This category showcases the team that adapted and succeeded in their high-touch in-person event to a full on virtual event experience

WINNER: AWS Reinvent

Why did they win? Amazon re:Invent. Leave it to Amazon Web Services to bring back tech shows at scale. re:Invent 2021 marked the first return to live events for most attendees and the crowded show exhibit halls and sessions strewn across multiple hotel conference facilities demonstrated that there's a big appetite to return to in-person events. Mask wearing and required evidence of vaccination put most live attendees at ease, but live and on-demand streaming options gave people flexibility to participate at their own comfort level. [Doug Henschen]

RUNNERS UP: Infosys America's Leadership Summit

Why were they recognized?

Infosys had the foresight and fortune of putting together a large executive customer event at Madison Square Garden the week of Novermber 15th. With international travel bans lifted and a respite from needless and ineffective lockdowns, Infosys got kudos for great topics, wonderful programming, and the opportunity to network in-person. Customer panels were insightful, sessions were designed for the right duration, and the level and number of executive attendees far exceeded expectations. Attendees enjoyed the opportunity to network in sky boxes while watching a New York Knicks game well into the night.

RUNNERS UP: Unit4 Experience 4 You (X4U) 2021

Why were they recognized?

Unit4 hosted a US based customer advisory event in Boston, Massachusetts. The event brought together HCM, Finance, IT, and operations professionals. On their first day, CEO, Mike Ettling kicked off the event with an inspiring keynote, featuring Mark Gallagher and Steve Cadigan, looking at the post-COVID future. Customers got a sneak peak into the new People Experience Suite and ERPx, Unit 4 also announced their acquisition news and Industry Mesh announcement along with customer awards.

BIGGEST TECH FLOP OF THE YEAR This category simultaneously recognizes the highest potential and largest failure in enterprise tech.

WINNER: Clubhouse and Andreesen Horowitz

Why did they win? Clubhouse. Is Clubhouse the 2021 equivalent of Pokemon.Go for grownups? It was all the rage, there for 15 minutes in 2020, but is anybody talking about or using it anymore in 2021? Business Insider is reporting "dwindling users and dubious advertizers." [Doug Henschen]

RUNNERS UP: AWS Outage Reporting

Why were they recognized? It is never good when the cloud goes down, especially when it is the largest region. And so it happened to AWS, with the biggest break being it did not happen during its user conference - AWS re:Invent - that hapened a week earlier. In its usual candid fashion, AWS explained in the post mortem on what happened, the biggst takeaway being that the world got to leaern more about the AWS inner workings. As it turns out AWS operated two networks - one for AWS and an internal network. The internal network controls resources, and a defective script overloaded netwrk and resources, resulting in a painful stop of all kinds of services. Knowing AWS they have learnt their lesson, but the big question remains, how does AWS balance its online retail business and its AWS customers. We got one more piece in that puzzle now. [Holger Mueller]

RUNNERS UP: Zillow Why were they recognized?

Zillow flop of iBuying and their belief that their algorithm could sniff out the best flips and establish Zillow as the ultimate real estate intelligence AND real estate holding company. Based on the "Zestimate" algorithm that, if anyone has ever actually tracked it, is questionable AT BEST, the company failed to sell of its holdings in markets where data was intensely flawed. Zillow blames the pandemic for bursting the housing bubble...but real estate watchers blame an algorithms inability to really understand home buying and home flipping. Both of these are examples of the big tech flop: leaving the digital lane for the physical without really understanding EITHER. [Liz Miller]

RUNNERS UP: Casper

Why were they recognized? Might not be a single flop...but it sure was a stinker of a year for digital darlings trying to cross the physical divide. Casper, the darling of social and digital business, went private at a valuation nearly ½ their IPO price just 2 years ago. Despite the promise of upending the mattress market, the digital brand favorites seemed to forget one thing...you don't buy a new mattress every year, no matter HOW much you love the thing. [Liz Miller]

Former Vice President and Principal Analyst

Constellation Research

Steve Wilson is former VP and Principal Analyst at Constellation Research, leading the business theme Digital Safety and Privacy. His coverage includes digital identity, data protection, data privacy, cryptography, and trust. His advisory services to CIOs, CISOs, CPOs and IT architects include identity product strategy, security practice benchmarking, Privacy by Design (PbD), privacy engineering and Privacy [or Data Protection] Impact Assessments (PIA, DPIA).

Coverage Areas:

- Identity management, frameworks & governance- Digital identity technologies- Privacy by Design

- Big Data; “Big Privacy”- Identity & privacy innovation

Previous experience:

Wilson has worked in ICT innovation, research, development and analysis for over 25 years. With double…...

One of the most popular slogans today is also one of the most confusing: Zero Trust. Of course we want to trust business partners and service providers to provide predictable outcomes. But “zero trust” is a technicality, a policy perspective that dispels the traditional class system which grants selected individuals or systems more privileged access than others. That’s the road to security hell, for it is increasingly possible to fake or falsely assume a trusted position, and thence wreak limitless damage.

A zero-trust access control policy means that all agents within an system are dealt with equally, regardless of identity or history. Essentially it equates to the “need to know” principle: all actors must have a demonstrable need for a given level of access.

Sadly “zero trust” has become a catch phrase, much abused in security marketing. All it really means is do not trust people on their word. Equally, we should not accept “zero trust” as a technical description on its word alone. It must go with tangible security controls.

Moore’s Law leads to periodic paradigm shifts in computing focus, from the server to the client and back again. In the 1980s and 90s, mainframe computing gave way to minicomputers, workstations, and microcomputers. Then the sheer volume of data processing required computing to swing back to huge back-end systems and shared resources, which became known as the cloud aka “someone else’s computers”.

The pendulum has swung yet again, driven by cryptography, with mounting preference (nay, mandates) for secure microprocessing units (MCUs) on the client side. Local encryption key generation and storage, and integrated transaction signing are now standard in mobile devices, and IoT device capability is heading the same way. Managing fleets of connected automobiles, smart electricity meters, and medical devices -- to cite some popular examples -- takes a dynamic mix of processing and storage at the edge and in the cloud.

High quality client-side cryptography is the key (pardon the pun) to genuine strong authentication; that is, using personally controlled tangible devices, individually accountable and resistant to phishing.