CoreWeave tops $5 billion in revenue for 2025, projects more hypergrowth 2026, 2027

CoreWeave topped $5 billion in annual revenue as the company said, "demand continues to intensify."

The company's fourth quarter highlighted how CoreWeave is racking up revenue and net losses as it scales out.

CoreWeave reported a fourth quarter net loss of $452 million, or 89 cents a share, on revenue of $1.57 billion, up from $747 million a year ago. For 2025, CoreWeave reported a net loss of $1.17 billion, or $2.81 a share, on revenue of $5.13 billion.

According to CoreWeave, the company had a revenue backlog of $66.8 billion as of Dec. 31. Current debt was $6.71 billion and non-current debt was $14.66 billion as of Dec. 31.

Michael Intrator, CEO of CoreWeave, said the AI cloud provider is seeing a "broader set of customers adopt CoreWeave Cloud."

Aside from building out AI data centers, CoreWeave has been expanding via acquisitions. It purchased Monolith and Marimo in the quarter.

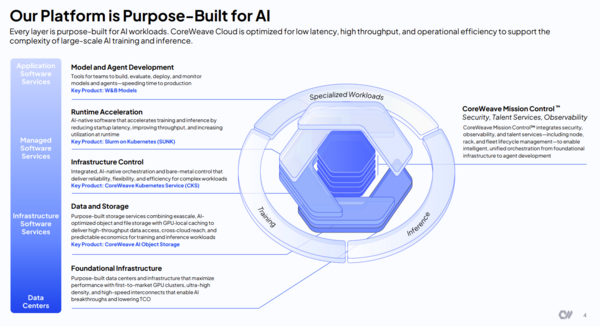

CoreWeave has also been building out its offerings and launched AI Object Storage for AI workloads, expanded CoreWeave Mission Control with new features and debuted Serviceless RL, a managed reinforcement learning service. The company also stood up CoreWeave Federal and partnered with CrowdStrike.

Intrator said CoreWeave "added approximately twice as many new reserved instance customers in Q4 versus any quarter in our history" with demand from hyperscale cloud providers, AI natives and enterprises. The enterprise demand is notable since CoreWeave saw "deepening engineering relationships with our largest customers and material progress on diversification," said Intrator.

He said:

"We grew the number of customers committed to spending at least $1 million on CoreWeave Cloud by nearly 150% these are not one-time infrastructure deployments. They represent sophisticated multiproduct opportunities, the early chapters of enduring platform relationships, and a growth engine that compounds as AI becomes more deeply embedded in how these companies operate. We are also seeing a significant increase in demand for prior generations of GPU architectures, where supply also remains constrained."

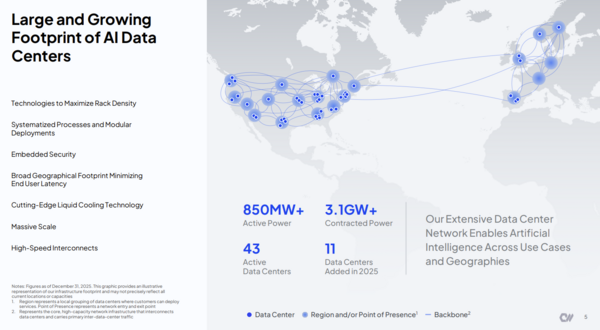

As for the outlook, CoreWeave projected more hypergrowth ahead. CoreWeave said 2026 revenue will be between $12 billion to $13 billion with operating income of $900 million to $1.1 billion. Capital expenditures will be between $30 billion to $35 billion to fund plans to double active power capacity to 1.7 gigawatts by the end of the year.

CFO Nitin Agrawal said:

"We expect adjusted operating income of $900 million to $1.1 billion. We anticipate margins will ramp sequentially from low single digits in Q1, expanding in each of Q2 and Q3 and returning to low double-digit levels by Q4 as deployed capacity matures and revenue scales against the existing cost base."

For the first quarter, CoreWeave will deliver revenue between $1.9 billion to $2 billion with adjusted operating income between break even and $40 million.

The plan according to Agrawal is to exit 2026 with an annual revenue run rate of $17 billion to $19 billion by the end of 2026 and more than $30 billion by the end of 2027.

That guidance excludes revenue or margin improvements from monetizing CoreWeave's cloud stack to third parties.

Intrator said CoreWeave's platform is evolving to "unlock margin-accretive avenues for growth through new products and services as well as offering our proprietary cloud stack outside of our data centers to the broader Nvidia ecosystem."

"Approximately 80% of CoreWeave Cloud customers paying at least $1 million per year have adopted one or more of our storage products. Additionally, we are seeing strong cross-selling momentum with Weights & Biases as we added hundreds of millions of CoreWeave Cloud TCV from Weights & Biases customers in the second half of the year," said Intrator.

Key takeaways:

- Sentiment on CoreWeave's earnings call was mixed. Wall Street analysts questioned the timing of capacity deployment and why revenue guidance wasn't higher. Agrawal said the new capacity came online at the end of the fourth quarter and will monetize in 2026.

- Enterprise deals. Intrator said enterprise contracts are similar to hyperscale deals in length (four to five years) but are structured for corporate needs. Enterprise deals are critical to diversification.

- Nvidia. Nvidia has partnered with CoreWeave on financing and that should "have a positive impact on the costs associated with our data center footprint." Intrator was asked about using custom chips compared to Nvidia reference architecture and he said the company is following overwhelming demand.

- Blackwell performance. Intrator said CoreWeave is seeing better performance but is "just getting going" and you will see "step functions in performance."

- Older Nvidia GPUs still sell well. CoreWeave is also selling older generations of Nvidia and prices are holding. Average H100 pricing in the fourth quarter was within 10% of where it was at the start of the year and A100 pricing increased.

Larry Dignan is Editor in Chief of Constellation Insights at Constellation Research, where he leads editorial coverage focused on enterprise technology, digital transformation, and emerging trends shaping the future of business. He oversees research-driven news, analysis, interviews, and event coverage designed to help technology buyers and vendors navigate complex markets with clarity and context. ...

Read morePublished

Author