ServiceNow's Q1: The strategy, AI, rule of 55 yet a lot of likely misplaced worries

ServiceNow's first quarter was in line with expectations and the company projected second quarter subscription growth of 22.5%. Separately, ServiceNow said it has expanded its partnership with Google Cloud and launched industry specific agentic AI offerings. Now if only Wall Street could understand the rule of 55 company and its strategy.

The company reported first quarter earnings of $469 million, or 45 cents a share, on revenue of $3.77 billion, up 22% from a year ago. Non-GAAP earnings were 97 cents a share. Wall Street was expecting ServiceNow to report first quarter non-GAAP earnings of 97 cents a share on revenue of $3.75 billion.

ServiceNow recently announced that it had closed the acquisition of Armis to expand into cybersecurity and risk. The company also said it will change its pricing strategy.

- ServiceNow ends the AI add-on, adds Context Engine, aims to scale Now Platform usage

- ServiceNow makes its cybersecurity move, acquires Armis for $7.75 billion

- ServiceNow integrates Moveworks, launches Autonomous Workforce, EmployeeWorks

CEO Bill McDermott said, "our AI growth is far exceeding even our own expectations." He added that ServiceNow's platform is seen as a way to deploy AI across clouds, models, data layers, interfaces and systems.

ServiceNow CFO Gina Mastantuono said the early close of the Armis purchase closed early and will accelerate the company's subscription revenue growth.

As for the outlook, ServiceNow said the first quarter saw a 75-basis point headwind it saw "delayed closings of several large on-premise deals in the Middle East, due to the ongoing conflict in the region." That reality colored the second quarter’s outlook given geopolitical headwinds and war in the Middle East.

The moving parts include:

- Second quarter subscription revenue will see a 125-basis point boost from Armis, which will also hit fiscal year 2026 subscription gross margin as well as a 75-basis point hit to operating margins.

- ServiceNow said that AI efficiencies internally will normalize integration costs and the margin hit to the Armis integration.

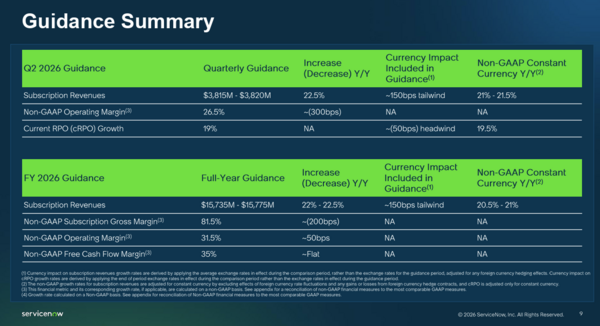

- Subscription revenue in the second quarter will be $3.81 billion to $3.82 billion, up 22.55.

- For fiscal 2026, ServiceNow projected subscription revenue of $15.73 billion to $15.77 billion, up 22% to 22.5%.

At Google Cloud Next, ServiceNow said it and Google Cloud are teaming up on joint offerings for AI agents in 5G networking, retail and IT systems. The companies will integrate Google Cloud's Gemini Enterprise platform and ServiceNow's AI Platform in a move that will couple ServiceNow AI Control Tower, Workflow Data Fabric and Google Cloud BigQuery. The companies will also run on a shared interoperability framework built on AI agent standards.

The fog of LLMs and ServiceNow's role

Regarding the Middle East, ServiceNow said the lumpiness is because those deals are all sovereign clouds and treated like on-premise revenue. It happens all at once and has a bigger impact on revenue. But those deals will be completed. Mastantuono added that the guidance wasn't reduced for any potential conflicts.

Speaking on a conference call with analysts, McDermott said net new annual contract value (NNACV) was strong in CRM and the company had 16 deals with NNACV worth more than $5 million and five deals worth more than $10 million. McDermott said the goal was to have $1 billion in committed AI revenue this year but it's already $1.5 billion.

As for ServiceNow's decision to include AI as part of the platform and end add-ons, he said that 50% of the company's net new business comes from a non-seat-based pricing models. That means ServiceNow's pricing includes tokens and other assets such as infrastructure, hardware and connectors. However, the pricing with AI included will be higher and incremental Assist revenue will be counted as AI revenue.

McDermott also said the acquisition of Armis and Veza will be transformative and both CEOs of those companies will continue to run the company. Both of those acquisitions as well as MoveWorks are showing traction and the ability to scale revenue, he said.

McDermott said the following on the call:

- "With the surface area so broad, our goals for ServiceNow are clear. Here they are: fast time to value for our customers, revenue growth acceleration, margin expansion, reduced stock-based compensation and outperforming our own rule of 55-plus standard. To say we're excited for Knowledge and Financial Analyst Day on May 4 in Las Vegas would be an understatement."

- "When an enterprise fully deploys ServiceNow, it's not just software, it's an end-to-end operating system. And today, an average Fortune 500 company has 100 million lines of custom code to manage their business. And this excludes the code in other systems of record where there are billions and billions of lines of code. As code volume increases 20x by 2030, the complexity of managing this explosion of code will increase exponentially. The volume of tickets generated by this complexity will also explode. In this scenario, the number of tickets hitting an ITSM system will increase by 50x compared to today."

- "With Mythos as one example, security activity is skyrocketing. The actions run through this platform, alerts, tickets, actions, resolutions, they're all revenue drivers for ServiceNow. Enterprises can't afford experiments in today's risk environment. They need ServiceNow as the strategic defense shield for the enterprise."

- "Armis is going to be our Instagram, and I'll tell you why. The #3 economy in the world is cybercrime. It's $1 trillion a month. We now have a situation where on the IT and the OT landscape of every major corporation, we are managing the agents and the humans, and we are managing the landscape of the threat actors. And if you think about a single intrusion from an AI agent will cost a commercial customer $5 million and a public sector customer $10 million, you have to look to ServiceNow quickly, and you'll need that core to illuminate the power of Armis. So those are issues that have not even happened yet. We just got Armis on Monday. So you're looking at a tailwind here that has -- I've never seen it. So get ready for major revenue acceleration."

- "When people ask, what's the difference between ServiceNow AI and the foundation models, you can boil it down to one word, context. I read that one of our customers referred to ServiceNow this way. The control tower is the quarterback. It figures out which agent or LLM to use. Merge that with a quote from the Hall of Fame Coach, Bill Walsh. Chaos is the quarterback's natural environment. There's plenty of chaos in today's enterprises. You have hyperscalers, systems of record, foundation models, data lakes, homegrown tools and agents coming at you from everywhere. That's why our platform is totally open. We integrate with all of them."

The big question from analysts is when will Wall Street understand ServiceNow and accelerating growth. McDermott was asked about why ServiceNow wasn't putting up AI lab type numbers. "I think the bigger argument for the shareholders is something like what's the terminal value of the software company? Is the seat-based pricing going to last? Well, when you have many more seats because the surface area you cover is 80% greater than what you used to cover, you're going to do fine on seats, but nobody cares about seats. We had a CIO from one of the biggest companies in the world tell us yesterday, she never bought a pricing plan one way or the other. She buys the return on the investment," said McDermott. "We're also mindful that customers are spending a lot on AI, but that is incremental. It is not replacing what they're spending on us."

Larry Dignan is Editor in Chief of Constellation Insights at Constellation Research, where he leads editorial coverage focused on enterprise technology, digital transformation, and emerging trends shaping the future of business. He oversees research-driven news, analysis, interviews, and event coverage designed to help technology buyers and vendors navigate complex markets with clarity and context. ...

Read morePublished

Author