Zscaler Q3 strong, outlook hit by component costs, sales turnover

Zscaler reported a better-than-expected third quarter, but the outlook was mixed due to higher memory, storage and processor costs and turnover in sales.

The company reported a third quarter net loss of $13.9 million, or 9 cents a share, on revenue of $850.5 million, up 25% from a year ago. Growth was fueled by the acquisition of Red Canary. Annual recurring revenue in the quarter was up 25% with Red Canary and 21% without. Non-GAAP earnings were $1.08 a share.

Jay Chaudhry, CEO of Zscaler, said the company’s Zero Trust architecture is resonating amid AI workloads, frontier models and compromised AI agents. “Our results demonstrate that our approach is resonating as we attract new customers and expand with our existing customers,” he said.

Zscaler’s results are setting the table for Palo Alto Networks and CrowdStrike earnings next week.

Zscaler’s third quarter non-GAAP earnings beat estimates by 7 cents per share.

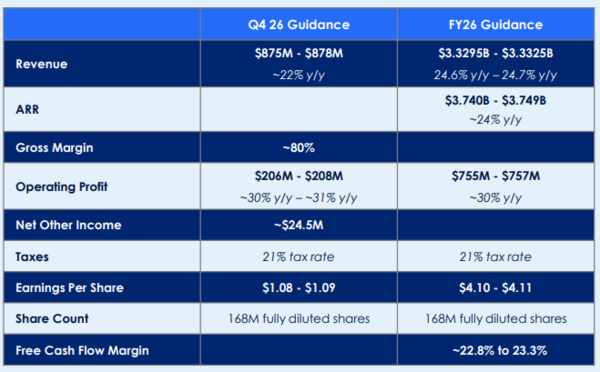

As for the outlook, the company projected fourth quarter revenue of $875 million to $878 million, up 22% from a year ago. Non-GAAP earnings will be $1.08 a share to $1.09 a share. For fiscal 2026, Zscaler projected revenue of $3.3295 billion to $3.3325 billion with non-GAAP earnings of $4.10 a share to $4.11 a share.

Wall Street was looking for fourth quarter non-GAAP earnings of $1.03 a share on revenue of $878.66 million. The fiscal 2026 outlook was better than expected.

In a shareholder letter, Zscaler outlined the mixed outlook and how increasing memory, storage and processor prices hit the company.

“We purchase equipment for our data center and Zero Trust Branch appliances. To mitigate costs, we put through a price increase on our branch appliance early this calendar year, which we expect to flow through in the next several months. We are also being opportunistic and taking advantage of delivery of data center equipment where we can get it, to lock in today’s prices ahead of potential increases in the future. This is pulling forward some of the investments we expected to make in fiscal 2027 into Q4. As a result, we expect higher capex in Q4, taking fiscal 2026 capex to the high single-digits as a percent of revenue, up from our prior expectation of mid-single-digits. Looking ahead to fiscal 2027, based on higher prices we see in the market today, we expect capex as a percentage of revenue to increase up to 200 basis points compared to fiscal 2026 levels.”

Zscaler is also dealing with sales turnover. The company said:

“At the end of the third quarter, two sales leaders departed the company. We have already appointed a replacement for one of these leaders, and we are in the late stages of hiring a leader for the other role. However, we are taking a prudent approach to our guidance during the transition.”

Not surprisingly, the first questions on an analyst call with analysts revolved around pricing and the sales executives. The component costs were surfaced since the reality is that hardware costs are going up due to AI data centers.

On the sales issues, Chaudhury said the two leaders who left were part of Chief Revenue Officer Mike Rich's team. He said the sales bench is strong, but could be disruptive. Zscaler took a "prudent approach" to guidance, said CFO Kevin Rubin.

The big theme from Zscaler is that its Zero Trust access approach resonates with Mythos and frontier models finding vulnerabilities.

"Today, users are the weakest link in cybersecurity. But soon, AI agents will be the weakest link because they operate at far greater speed and have far less oversight. Even a single compromised agent can move from discovery to data theft in minutes, inflicting catastrophic damage on enterprises. Making it even more challenging, new powerful frontier AI models like Mythos are finding security vulnerabilities in software at machine speed, significantly diminishing the effort, skill and time needed to breach enterprises. All enterprises already have thousands of known vulnerabilities that they haven't been able to patch. Frontier models are multiplying these unremediated vulnerabilities by as much as 10x and even more powerful models that are currently being developed will undoubtedly make it worse. Enterprises don't have the capacity to patch and update existing vulnerabilities, so backlogs are piling up faster than organizations can address them."

He added that Zscaler has "never seen so many inbound calls come in so quickly." Chaudhry said CIOs are concerned and Zero Trust is one of those things that need to be done. "We also know that this is an area where we need to help our customers and not do ambulance chasing, okay? So we're not rushing to create opportunities. We are actually engaging with our customers in a consultative fashion to help them get out of the tough situations so they can really keep the Board and CEOs apprised of what's going on," he said.

Here's what else Chaudhry had to say on the earnings call.

- "We announced our intent to acquire Symmetry Systems, a company that solved this difficult problem. Symmetry provides an access graph that maps how identities, applications and other data sources connect across the enterprise. We are integrating its Access Graph technology with our Zero Trust Exchange."

- "We continue to deepen our partnership with global system integrators or GSIs, who play a meaningful role in expanding the reach of the Zscaler platform. we are seeing strong growth in bookings through our GSI partners."

- "Our AI Protect solution is resonating with customers with bookings crossing $100 million over the past 12 months. We are seeing inbound requests from across our customer base, and our pipeline is robust and growing."

Larry Dignan is Editor in Chief of Constellation Insights at Constellation Research, where he leads editorial coverage focused on enterprise technology, digital transformation, and emerging trends shaping the future of business. He oversees research-driven news, analysis, interviews, and event coverage designed to help technology buyers and vendors navigate complex markets with clarity and context. ...

Read morePublished

Author