So here are my Top3 takeaways (the press release can be found here):

Simplification – in the past Oracle pegged its products to IaaS / PaaS etc. – now we have the Oracle Cloud Platform (for PaaS) and the Oracle Cloud Infrastructure Services (for IaaS). A good top level naming convention, but then the same, massive offering lies underneath. But it is good to see that the official Strategy for Oracle Cloud Platform is to bring Oracle’s Database and Middleware offerings together for the ‘customers and partners anywhere in the world through the Internet’. Note the internet – more below. It is somewhat simpler for the Oracle Infrastructure Services portfolio – that offers infrastructure services for workloads is an ‘enterprise grade cloud managed, hosted and supported by Oracle’. And these are the 3 basic computing services, compute, storage and networking. As mentioned in the progress report of the cloud analyst summit in spring (see here) that is the area where Oracle is relatively most behind, compared to PaaS and SaaS.

Simplification – in the past Oracle pegged its products to IaaS / PaaS etc. – now we have the Oracle Cloud Platform (for PaaS) and the Oracle Cloud Infrastructure Services (for IaaS). A good top level naming convention, but then the same, massive offering lies underneath. But it is good to see that the official Strategy for Oracle Cloud Platform is to bring Oracle’s Database and Middleware offerings together for the ‘customers and partners anywhere in the world through the Internet’. Note the internet – more below. It is somewhat simpler for the Oracle Infrastructure Services portfolio – that offers infrastructure services for workloads is an ‘enterprise grade cloud managed, hosted and supported by Oracle’. And these are the 3 basic computing services, compute, storage and networking. As mentioned in the progress report of the cloud analyst summit in spring (see here) that is the area where Oracle is relatively most behind, compared to PaaS and SaaS.

|

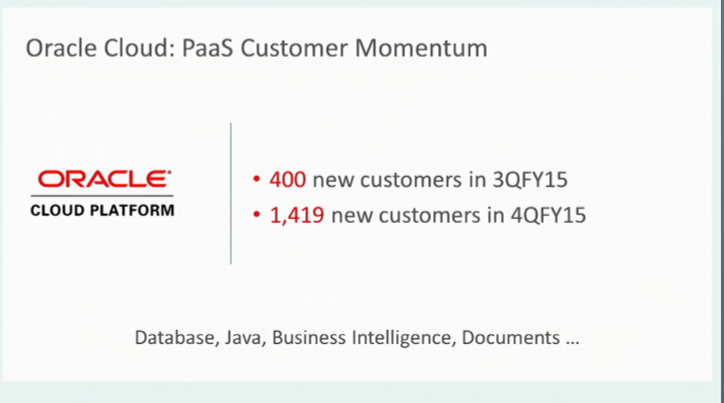

| Oracle PaaS Customers |

The interesting aspect on Oracle Cloud Platform is the ‘through the internet’ addition in the strategy charter above. Oracle delivers one of the few offerings that can be deployed both in Oracle’s cloud infrastructure as well as on premises. In the latter the support, upgrades and maintenance is delivered through the internet. Oracle keeps stressing that the same code runs on both sides, workloads can be moved transparently as customers wish. This remains a key differentiator of Oracle towards most cloud offerings in the market. It will be good to see some proof points of customers taking advantage of this capability, especially for the hybrid usage of the offering. What we see right now that it is more of a binary (on premises vs cloud) decision in sales conversations and deployment decisions.

|

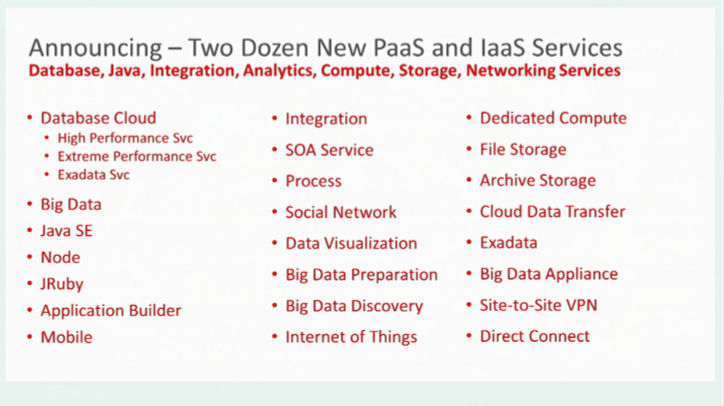

| Oracle PaaS Momentum |

GA of 6 cloud Services – The main message from product side was that 6 Oracle cloud services are now available. These are Oracle Database Cloud – Exadata Service, Oracle Archive Storage Cloud Service, Oracle Big Data Cloud Service and Big Data SQL Cloud Service, Oracle Integration Cloud Service, Oracle Mobile Cloud Service and Oracle Process Cloud Service. All six are major achievements for Oracle, with making the Oracle database available on Exadata machines in the Oracle cloud being a potential cannibalization of Exadata hardware sales, so quite remarkable. And Oracle introduced its competitor to Amazon AWS Glacier with Oracle Archive Storage Cloud Service, not surprisingly at a lower price point, but it wasn’t clear if services were 100% identical. The two BigData Services are interesting as they move BigData usage closer to business users, which overall is the right strategy direction for all enterprise services. The same is valid for Oracle Mobile Cloud Services that allows business users to build (simple) cross platform mobile applications, a product that once fully working and adopted, will change the way how mobile applications are built. And Oracle Integration Cloud Service is interesting for the same approach, bringing the tools of enterprise software integration to business end users. An ambitious goal, but Oracle has made steps close to achieve that goal.

|

| All PaaS Announcements |

But there was more – in total Oracle announced 23 PaaS Services, some key networking services to make the Oracle vision a reality (Site to Site VPN, Direct Connect), a lot around polyglot / multi language capabilities of the Oracle cloud (next to Java, Node.js and Ruby), but the most interesting ones to me remain the business end user enablement services, around Application Builder, Data Visualization, Big Data Preparation and Discovery and a ‘make sense of IoT data’ service. While a number of the announced services are basic enablers, some even table stakes and others are bringing Oracle products to the cloud, the real differentiators going forward lie in the business end user enablement services.

|

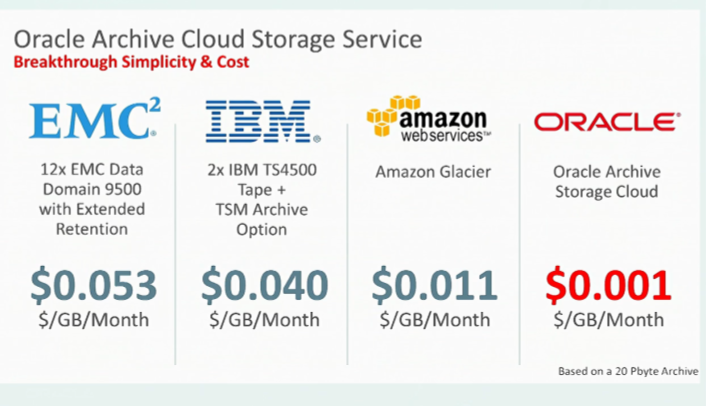

| Oracle comparison on GB / month |

It’s all about TCO – We have written before that at the core of Oracle’s organization DNA is TCO savings, starting with the first product reducing database costs with the relational database. For Oracle in 2015 it means engineering the whole technology stack together, in order to achieve lower cost for performance. And while Oracle did not offer any specific savings beyond storage (Oracle claims to be cheaper than Amazon AWS, EMC and IBM) at the event, the recent announcements of Oracle getting into the two socket server market, shows the power of the approach (we covered it here). What was remarkable there is, that Oracle did not want to be in ‘commodity hardware’ – but changed its strategy (still wondering and speculating why) and then applied the integrated technology stack strategy and approach to the problem. The result is a significantly lower TCO for the Oracle two socket server systems (compared to other market leaders), so the strategy even delivers in areas that were not original targets. A good capability to have for any technology vendor in the fast shifting technology markets.

Overall MyPOV

Another Oracle cloud event with a lot of announcements, but also 6 PaaS cloud services in GA. Oracle did not mention when all of them would be GA (or I missed it in the 5 hours, sorry) , so that is good progress – but can’t hide over the fact that Oracle is ‘still getting there’. What is impressive is to see what kind of revenue Oracle can generate already based on this early offering, the vendor claims to have had the most record ‘cloud’ quarter in the industry with its Q4, with 400+M in new subscription revenue. Which makes clear that the game for Oracle is execution both on the product and on the sales side.On the concern side, Oracle has to build and deliver a lot. One of the largest engineering projects on the planet, if not the largest. And due to the integrated nature of the offering, more bits and pieces have to work flawlessly together. Anyone with experience in enterprise software knows that harmonizing the release of two products is more often a challenge than not. Oracle is releasing multiple 100s that need to work together. And Oracle is building its cloud ‘top down’ – having more mature SaaS than PaaS, more mature PaaS than IaaS products (or replace mature with available). In the ideal world you would go IaaS to PaaS to SaaS. But that’s a place where Oracle finds itself for historic reasons, now it needs to retrofit its SaaS offerings to take advantage of its new PaaS and IaaS capabilities. Take the very promising Oracle Integration Cloud Service, which will have out of the box integrations, built by the SaaS teams. So interfaces are being rebuilt, re-tested etc. Ultimately Oracle has the experience and resources to get all done, and in the long run it is cutting no corners and doing the right thing, but it takes time, investment and stamina. For now it looks Oracle has all of them.

On the differentiation side, Oracle is probably the cloud vendor that focusses the most on business end user enablement, a new era of self-service that is enabled by the cloud. With that it changes the way how enterprise software is created, implemented and supported. Less partners and Sis, more business users that build what they need and want quickly. In a world that is accelerating every day, a key capability for business users, who dread nothing else more than going to IT, paying a partner and increasingly cannot afford to wait for days to go live because some software had to be changed somewhere.

The other differentiator for Oracle is the completely integrated technology stack, where it has a quite unique position in the market. Oracle needs to show the advantages of this to decision makers, who traditionally are concerned about too much tie in, but on the flip side want to avoid too many integration worries. TCO is where decision makers and Oracle can come together on this, and given Oracle’s TCO driven corporate DNA, Oracle is well positioned for that conversation. We saw glimpses of that at the event when it came to storage costs and number of steps it takes to get a product up and running. These stats are interesting but need customer backup sooner than later.

A compelling vision and some good early proof points for Oracle, but it is early, key capabilities need to be made available not only announced, so it is execution and then customer adoption time for Oracle. We will be analyzing.